The stakes are concrete. Non-compliance can trigger civil fines reaching €20 million or 4% of global revenue under GDPR, multi-million dollar AML enforcement actions, and direct pressure from sponsor banks demanding named compliance leadership before granting or maintaining banking relationships. One testimonial from a Fraxtional client sums up what many early-stage teams discover too late: "Our sponsor bank required us to appoint a BSA Officer. Fraxtional came in, cleaned up our AML framework, and helped us pass review faster than we expected."

This article covers what payments compliance actually means, the key regulatory frameworks across the US, UK, Canada, and EU, the five pillars of a compliance program, who owns this function at different company stages, and how to build your program without starting from scratch.

Key Takeaways

- Payments compliance covers AML, data privacy, PCI DSS, and consumer protection — all at once

- AML and sanctions failures carry real costs: fines range from $507K (BitPay) to $4.3B (Binance)

- The UK's APP fraud reimbursement rules took effect October 2024, adding new PSP liability

- Regulators often legally require named compliance leadership: BSA Officer, MLRO, or CAMLO depending on jurisdiction

- Fractional compliance officers give early-stage fintechs director-level expertise without the cost of a full-time hire

What Is Payments Compliance and Why It Matters

Payments compliance is the set of policies, procedures, and controls a business must implement to meet legal and regulatory requirements when processing, transmitting, or storing financial transaction data. It spans anti-money laundering rules, data privacy obligations, payment card security standards, and consumer protection frameworks.

Three core goals drive the entire discipline:

- Preventing financial crime — stopping money laundering, fraud, and sanctions violations before they happen

- Securing payment data — protecting card numbers, account details, and personal financial information

- Protecting consumers — ensuring transparent fees, accessible dispute resolution, and fair treatment

Who Needs to Comply

Almost any entity that touches a financial transaction carries compliance obligations. This includes:

- Merchants accepting card payments

- Payment service providers and processors

- Financial institutions and sponsor banks

- Fintech and embedded finance companies

- Money transmitters

- Crypto exchanges and wallet providers

The Real Cost of Getting It Wrong

Enforcement actions from the past few years make the financial exposure clear:

| Year | Entity | Issue | Penalty |

|---|---|---|---|

| 2024 | CB Payments Ltd (UK) | High-risk customer controls breach | £3,503,546 |

| 2025 | Block / Cash App (US) | Consumer error-resolution failures | Up to $175M |

| 2023 | Binance (US) | AML and sanctions failures | $4.3B |

| 2022 | Bittrex (US) | AML and sanctions violations | $53M+ combined |

| 2021 | BitPay (US) | Sanctions violations | $507,375 |

Beyond fines, GDPR Article 83 allows penalties up to €20M or 4% of worldwide annual turnover, whichever is higher. UK GDPR mirrors this at £17.5M or 4%.

The rules themselves keep changing. New UK APP fraud reimbursement requirements, updated AML frameworks, and successive PCI DSS versions mean a program that passed last year may fall short today. Compliance is ongoing work — not a one-time setup.

Key Regulatory Frameworks Across the US, UK, Canada, and EU

AML and BSA Obligations

Each jurisdiction takes a distinct approach. Here's what applies where:

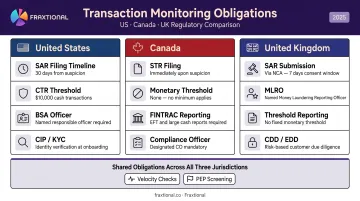

| Jurisdiction | Regulator / Law | Key Obligations |

|---|---|---|

| United States | FinCEN / Bank Secrecy Act | Written AML program; SARs for $2,000+ suspicious activity; CIP checks; MSB registration within 180 days, renewed every 24 months |

| Canada | FINTRAC / PCMLTFA | MSB or foreign MSB registration (required since July 2022 for crowdfunding platforms and certain PSPs); no minimum threshold for STRs — any reasonable grounds triggers reporting |

| United Kingdom | FCA / MLR 2017 | Written AML program; appointed Money Laundering Reporting Officer (MLRO); full compliance required for authorized payment and e-money firms |

Fintechs operating through sponsor banks in the US inherit BSA obligations directly — the bank's program doesn't insulate the fintech partner from its own compliance duties.

PCI DSS and Payment Card Standards

PCI DSS v4.0.1 applies to any business that stores, processes, or transmits payment card data — regardless of where it's headquartered. The standard comprises 12 requirement families covering:

- Network security controls and secure configurations

- Encryption of stored and transmitted card data

- Access controls and user authentication

- Regular penetration testing and security monitoring

- Documented information security policies

Compliance tier depends on transaction volume and is typically determined by your acquiring bank or card brand.

Card compliance sits alongside a separate but equally binding layer of data protection law — one that specifically governs what you do with the personal financial data you collect.

Data Privacy Laws

Payment data — names, card details, account numbers — falls squarely under major privacy regimes:

- EU GDPR / UK GDPR: Requires a lawful basis for processing personal financial data, with consumer rights of access, erasure, and portability. The ICO fined British Airways £20M in 2020 after a breach affecting more than 400,000 customers, including payment card data.

- CCPA (California): Grants California consumers rights to know, delete, correct, and opt out of the sale of their personal information, including financial data.

For EU and UK payment businesses, data privacy obligations run in parallel with authentication requirements baked into the payments directive itself.

PSD2 and Strong Customer Authentication

Under PSD2, businesses offering electronic payment services in the EU or UK must implement Strong Customer Authentication (SCA) — verification using at least two independent factors (knowledge, possession, or inherence) — for account access and payment initiation. UK contactless exemptions currently sit at £100 per transaction and £300 cumulative.

This obligation applies to regulated payment services under EU or UK frameworks — not just firms incorporated there.

UK APP Fraud Reimbursement Rules

The Payment Systems Regulator's mandatory APP fraud reimbursement scheme came into effect on 7 October 2024. Under these rules:

- PSPs must reimburse victims of authorised push payment fraud up to £85,000 per claim

- Liability is shared between the sending and receiving PSP

- In-scope users include consumers, micro-enterprises, and small charities

PSR performance data from early 2024 shows significant variation across firms — Nationwide reimbursed 85% of APP scam value, while some firms had substantially higher fraud rates per million transactions sent. PSPs touching UK Faster Payments need documented fraud controls and a clear reimbursement workflow before the PSR comes knocking, not after.

The Five Core Pillars of a Payments Compliance Program

AML, KYC, and KYB Controls

Effective AML compliance starts with knowing who you're doing business with.

- Verify individual identity at onboarding (KYC) — required under BSA, FCA regulations, and FINTRAC

- Verify the legitimacy of business counterparties (KYB) and identify Ultimate Beneficial Owners (UBOs)

- FinCEN's CDD Final Rule sets the UBO threshold at 25% ownership for covered financial institutions

UBO identification gaps remain among the most common findings in sponsor bank reviews and regulatory examinations — and they're also among the easiest to miss during rapid onboarding.

Transaction Monitoring and Suspicious Activity Reporting

Once customers are onboarded and verified, the compliance focus shifts to what they do. Businesses must monitor transactions for patterns consistent with money laundering, fraud, or sanctions evasion. Key operational requirements include:

- Velocity checks and structuring detection

- High-risk geography and PEP screening

- SAR filing within 30 days of detection (US), with records retained for 5 years

- STR filing with no monetary threshold (Canada)

- SAR filing managed by the named MLRO (UK)

Improperly configured monitoring rules and failure to file are among the most cited deficiencies in AML enforcement actions.

Data Security and PCI DSS Compliance

PCI DSS compliance goes beyond technology. It requires:

- Encryption of card data at rest and in transit

- Tokenization where possible to reduce scope

- Strict access controls and user authentication

- Regular penetration testing and quarterly vulnerability scans (frequency varies by PCI DSS merchant tier)

- Documented policies and annual assessments

Failure to maintain compliance exposes businesses to card network fines and data breach liability.

Consumer Protection and Disclosure Obligations

Across all four target jurisdictions, businesses must clearly disclose payment terms, fees, and error resolution procedures:

- US Reg E: Consumers generally have 60 days to report errors; institutions must investigate within 10 business days (extendable to 45 with provisional credit)

- UK FCA Consumer Duty: Applies to all payment and e-money firms authorized under PSRs 2017, with an outcomes-focused standard that took full effect in 2023

- EU/UK PSD2: Mandates pre-contractual and transaction-level disclosures for payment services

Consumer-facing compliance shapes user experience directly. Disclosure failures are one of the fastest routes to FCA or CFPB supervisory action, regardless of how strong your back-end AML program is.

Sanctions Screening and Regulatory Reporting

Every payments business must screen customers, counterparties, and transactions against:

- OFAC SDN list (US) — on a strict-liability basis, meaning intent is not a defense

- HM Treasury consolidated list (UK)

- Equivalent lists in the EU and Canada

BitPay's $507,375 settlement for 2,102 apparent violations illustrates the exposure even for smaller payment processors. Screening must happen at onboarding and continuously as lists update.

Who Is Responsible for Payments Compliance?

Required Roles and What They Do

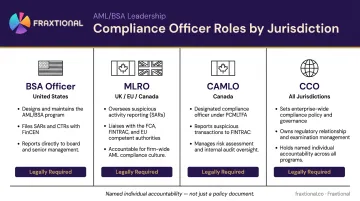

Most regulatory frameworks require a named individual accountable for the AML program — not just a team or a policy document:

| Role | Jurisdiction | Responsibilities |

|---|---|---|

| BSA Officer | US | AML program oversight, SAR filing, FinCEN liaison |

| MLRO | UK / EU / Canada | Suspicious activity reporting, FCA liaison, AML training |

| CAMLO | Canada (primary) | Strategic AML leadership, FINTRAC reporting, risk posture |

| CCO | All | Overall compliance program, regulatory coordination, policy oversight |

These are legally required roles in most cases — not optional hires.

The Cost Challenge for Early-Stage Fintechs

Hiring full-time compliance leadership is expensive. BarkerGilmore's 2025 CCO compensation report puts technology-sector CCO total compensation at $770,000. UK Head of Financial Crime / MLRO roles command £150,000–£300,000 according to Barclay Simpson's 2025 salary guide.

For a seed-stage or Series A fintech, that budget simply doesn't exist — yet sponsor banks and regulators expect credible, named compliance leadership before granting licenses or banking relationships.

The Fractional Compliance Model

Fractional compliance leadership fills this gap directly. Rather than hiring a full-time CCO or BSA Officer, fintechs can engage an experienced director on a part-time or project basis, with the named title, regulatory accountability, and sponsor bank credibility that comes with a senior appointment.

That's the model Fraxtional is built around, covering all four roles (CCO, BSA Officer, MLRO, CAMLO) through three engagement structures:

- On Demand Advisory — flat fee for discrete projects like audits, risk assessments, or sponsor bank introductions

- Subscription Advisory — monthly or weekly retainer for ongoing guidance and staff augmentation

- Fractional Advisory — dedicated director with named title use, most suited for companies needing a permanent-equivalent compliance lead without the permanent cost

One CEO of a Series B fintech described the decision plainly: "After looking at various options, including hiring a full-time BSA Officer, we were convinced that the fractional resource provided the most flexibility and the most expertise at the best price."

Fraxtional's directors are named on regulatory filings, participate in sponsor bank calls, and handle investor due diligence, acting as part of the company rather than outside consultants. The firm has been recognized as a Leader in Compliance through the T100 Finance Award, with founder Ryan Cimo named among the Top 100 Leaders in Finance for 2024.

Best Practices for Building Your Payments Compliance Program

Map Your Jurisdictions First

Identify every market where your business accepts or processes payments. Determine which frameworks apply — BSA/AML in the US, FCA registration in the UK, FINTRAC in Canada, GDPR in the EU — and build controls for the most stringent obligations first. Stronger controls typically satisfy less prescriptive requirements in other markets.

Monitor Continuously, Not Periodically

The UK APP fraud rules, updated PCI DSS versions, and evolving FINTRAC guidance all shifted within the past two years. A point-in-time audit won't catch the next change. Your program needs processes to track regulatory updates, schedule internal audits, and test controls — including transaction monitoring thresholds and sanctions screening coverage — on a rolling basis.

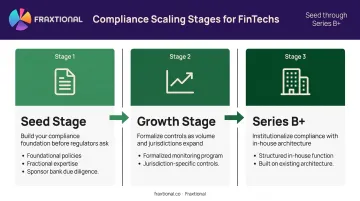

Scale your compliance function strategically:

- At seed stage, document foundational policies and engage fractional expertise to satisfy sponsor bank due diligence

- As volume grows, formalize your monitoring program and add jurisdiction-specific controls

- At Series B and beyond, transition to a structured in-house function built on the program architecture already in place

That transition from fractional to in-house doesn't mean starting over. Well-structured fractional engagements produce documented workflows, threshold logic, escalation paths, and audit-ready policies that incoming permanent leaders can inherit directly. Fraxtional's directors document every workflow with handover explicitly in mind, so incoming compliance leaders step into a functioning program rather than a blank slate.

Frequently Asked Questions

What is payments compliance?

Payments compliance is the combination of regulatory rules, industry standards, and internal controls businesses must follow when processing financial transactions. It covers AML obligations, data privacy requirements, PCI DSS card security standards, and consumer protection rules — with the specific requirements depending on your jurisdiction and business model.

What should a payments compliance notice set out?

A payments compliance notice should clearly state payment terms, applicable fees, the payment service provider's identity, consumer dispute and refund rights, and how personal and financial data will be handled. Requirements vary by framework — PSD2, FCA Consumer Duty, and US Reg E each set their own disclosure standards.

What are the new payment rules in the UK?

The UK PSR's mandatory APP fraud reimbursement scheme took effect on 7 October 2024, requiring payment service providers to reimburse victims of authorised push payment fraud up to £85,000 per claim. Alongside this, FCA Consumer Duty obligations require payment firms to demonstrate positive consumer outcomes across all products and services.

Who is responsible for payments compliance in a fintech company?

Most frameworks require a named individual accountable for the AML program: a BSA Officer in the US, MLRO in the UK, or CAMLO in Canada. The CCO oversees compliance more broadly. Early-stage fintechs often use fractional compliance officers to fill these roles without the overhead of a full-time hire.

What happens if a company fails to meet payment compliance requirements?

Consequences range from civil and criminal fines to loss of payment licenses, card network access, and sponsor bank relationships. Named compliance officers can face personal liability in serious cases. Penalty amounts vary widely — from hundreds of thousands to billions of dollars depending on severity and duration.

What is the difference between PCI DSS and AML compliance?

PCI DSS is a data security standard set by card networks focused on protecting payment card data from breaches through technical and operational controls. AML compliance is a legal obligation focused on preventing money laundering and financial crime through customer verification, transaction monitoring, and suspicious activity reporting. Both are required, but they address different risk categories.