Yet most financial services companies treat compliance as a documentation exercise — write the policy, file it away, and move on. The gap between what's written and what actually happens operationally is where enforcement actions are born.

This article explains what compliance testing is, why it produces measurable business value, and what separates firms that pass examinations from those that don't.

Key Takeaways

- Compliance testing verifies that controls, policies, and procedures work in practice — not just on paper

- For fintech, crypto, and banking firms, it catches regulatory gaps before examiners or sponsor banks do

- Effective testing improves risk visibility, strengthens controls, and builds credibility with regulators and investors

- Without formal testing, gaps surface as enforcement actions or damaged partnerships — not internal findings

- Testing delivers the most value when continuous, risk-based, and tied to remediation workflows

What Is Compliance Testing?

Compliance testing is the systematic review of whether a firm's controls, policies, and procedures are functioning as designed and aligned with applicable regulatory requirements.

The distinction matters: writing a policy is not the same as testing whether that policy is followed. Passing a one-time audit is not the same as ongoing assurance that controls work under real operational conditions.

The FFIEC BSA/AML Examination Manual is explicit on this point — independent testing exists to assess a bank's compliance with BSA regulatory requirements relative to its risk profile, and scope and frequency should be commensurate with that risk profile.

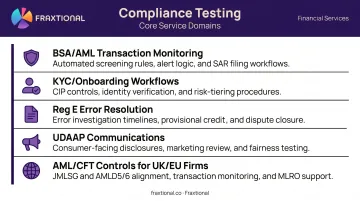

Where Compliance Testing Applies in Financial Services

In practice, compliance testing covers:

- BSA/AML transaction monitoring — validating that thresholds, alert logic, and SAR filing triggers are calibrated correctly and functioning as intended

- KYC/onboarding workflows — sampling customer records to confirm identity verification, documentation, and risk classification are consistent with policy

- Reg E error resolution — reviewing whether dispute handling procedures follow required timelines and documentation standards

- UDAAP-sensitive communications — checking that disclosures, marketing materials, and fee structures don't create unfair, deceptive, or abusive risk

- AML/CFT controls for UK and EU firms — testing against FCA SYSC requirements and EBA AML/CFT guidelines, including at least annual assessment of the compliance function's effectiveness

The goal is continuous assurance that controls work under real conditions — not a milestone that gets cleared once and forgotten.

Key Advantages of Compliance Testing

The advantages below reflect measurable operational and regulatory outcomes. They compound when testing is done consistently and tied to a firm's actual risk profile, not a generic checklist applied uniformly across the business.

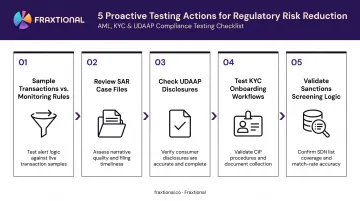

Advantage 1: Proactive Regulatory Risk Reduction

Compliance testing allows firms to identify control failures — gaps in transaction monitoring thresholds, missed SAR filing triggers, incomplete KYC documentation, misapplied consumer protection rules — before regulators, sponsor banks, or auditors find them.

The financial stakes of getting this wrong are significant. TD Bank's 2024 AML resolution totaled approximately $3.09 billion, with DOJ citing AML program and transaction-monitoring failures spanning nearly a decade. Binance faced a $3.4 billion FinCEN civil money penalty, with FinCEN noting that MSBs are required to provide independent review to monitor and maintain adequate AML programs.

Both cases involved slow-moving gaps that internal testing could have surfaced years before regulators acted.

How testing creates this advantage in practice:

- Systematically sampling transactions against defined monitoring rules

- Reviewing SAR case files for documentation completeness and escalation timing

- Checking disclosures and customer communications against UDAAP standards

- Testing onboarding workflows against written KYC procedures

- Validating sanctions screening logic against OFAC and FCA requirements

KPIs impacted: Number of examination findings, time-to-remediation, fine exposure, examination cycle frequency

When this matters most: During rapid product scaling, entry into new markets, or after regulatory updates — situations where existing controls may not yet cover newly introduced risks.

Advantage 2: Operational Transparency and Control Strength

Compliance testing surfaces the gap between what written policies say and what employees and systems actually do. In fast-growing fintechs, documented procedures routinely lag behind operational reality. That gap stays invisible until stress or examination forces it into view.

The FCA's enforcement actions against Starling Bank and CB Payments illustrate this directly. Starling grew from roughly 43,000 customers in 2017 to 3.6 million by 2023, and the FCA found that financial crime controls did not keep pace. Over 54,000 accounts were opened for 49,000 high-risk customers in breach of agreed restrictions. The fine: £28.96 million.

CB Payments' case is equally instructive. The FCA cited inadequate design, testing, implementation, monitoring, and records — with repeated breaches going undiscovered for almost two years. The restriction existed on paper, but no testing was in place to verify it was actually working.

What operational testing catches:

- Staff applying KYC rules inconsistently across customer segments

- Monitoring alerts being cleared without proper documentation or supervisor sign-off

- Complaint handling workflows diverging from written procedures

- Automated system outputs that don't match manual review benchmarks

KPIs impacted: Control effectiveness scores, exception rates, audit finding frequency, staff adherence rates, complaint volumes

When this matters most: After major operational changes — new banking partners, product launches, jurisdiction expansions, or compliance staff turnover.

Advantage 3: Credibility with Regulators, Sponsor Banks, and Investors

A documented, functioning compliance testing program is one of the clearest signals a firm can send that its compliance posture is genuine. Testing results, exception logs, and remediation records aren't just internal housekeeping — they become evidence during regulatory examinations, sponsor bank due diligence, and investor pre-deal reviews.

The 2023 interagency third-party guidance from OCC, FRB, and FDIC makes the bank's position clear: use of third parties does not reduce a bank's legal responsibility to comply with applicable laws and regulations. Banks are accountable for what their fintech partners do — and they know it. The OCC's formal agreement with Blue Ridge Bank required a revised BSA audit program with expanded fintech scope and sufficient transaction testing before approving new fintech partner onboardings.

A firm that can present consistent testing history, exception documentation, and remediation records is materially lower-risk in the eyes of a banking partner than one that produces only a compliance manual.

What sponsor banks and investors want to see:

- Independent testing reports from qualified internal or external reviewers

- Exception and issue inventories with documented escalation

- Remediation evidence showing findings were addressed and closed

- Board or committee-level compliance reporting demonstrating governance

- Third-party monitoring documentation for fintech-bank relationships

KPIs impacted: Time-to-partnership approval, due diligence pass rates, examination cycle outcomes

When this matters most: When seeking a new sponsor bank relationship, during Series A or B fundraising with regulatory due diligence, or when expanding from one regulated jurisdiction into multiple.

What Happens When Compliance Testing Is Ignored

Without compliance testing, policies exist on paper but no one verifies whether controls actually work. Exceptions go undetected. The gap between documented intent and operational reality widens — until it can't be ignored.

When it does surface, the timing is rarely convenient.

The most common real-world consequences:

- Regulatory examinations uncover findings that become public enforcement actions, corrective action plans, or fines — often for issues that internal testing would have caught months or years earlier

- Sponsor banks pause or terminate partnerships when due diligence reveals no evidence of ongoing program effectiveness — a critical exposure for fintech companies whose entire operating model depends on those relationships

- Leadership spends disproportionate time responding to examiner requests and managing audit findings rather than building the business

The reputational cost compounds the financial one. Enforcement actions are public, and they signal weakness to prospective banking partners, investors, and regulators across jurisdictions. For early-stage companies still building regulatory credibility, a single consent order can set back partnership timelines by years.

The Blue Ridge Bank formal agreement is telling from the sponsor-bank side: the OCC required no supervisory objection before onboarding new fintech partners, a written third-party risk management program, and expanded transaction testing as preconditions for resuming normal operations. For any fintech in that bank's pipeline, operations stalled — not because of their own program failures, but because their sponsor had none to show.

How to Get the Most Value from Compliance Testing

Testing works best when it's risk-based, continuous, and tied directly to remediation. A few practical principles:

Prioritize by risk, not alphabetical order. AML transaction monitoring, KYC onboarding, consumer complaint handling, and cross-border payment flows carry more regulatory exposure than many other areas. Test those more frequently and more deeply.

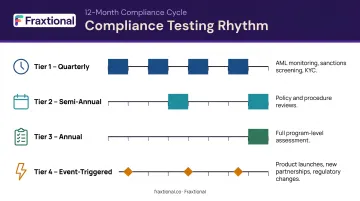

Build a defined testing rhythm:

- Quarterly transactional testing for high-risk areas (AML monitoring, sanctions screening, KYC)

- Semi-annual policy and procedure reviews

- Comprehensive annual program-level assessment

- Event-triggered testing after product launches, new partnerships, regulatory updates, or significant staff changes

Document everything. Every test finding — even minor exceptions — should be documented with the tester, date, scope, result, and remediation step. Regulators and sponsor banks review this documentation, not just the outcomes. A testing program without documentation is almost as weak as no testing program at all.

Match the tester to the standard. The FFIEC requires independent testing — conducted by internal audit, outside auditors, consultants, or other qualified independent parties. Self-certification by the team that runs the control being tested doesn't satisfy this standard.

That independence requirement creates a real challenge for fintech startups, crypto firms, and embedded finance companies that don't yet have a full-time Chief Compliance Officer. Working with fractional compliance leadership fills that gap — providing the director-level expertise to design, run, and interpret testing programs without the cost of a full-time executive hire.

Fraxtional's fractional CCO and BSA Officer model, for example, places named compliance executives directly into client teams. They own daily monitoring, SAR workflows, case governance, and testing oversight in a way that satisfies both regulatory expectations and sponsor bank requirements.

Conclusion

The value of compliance testing lies not in its existence on a compliance calendar, but in what it reveals, how quickly findings are remediated, and how consistently it's applied across the firm's highest-risk areas.

Those findings — and what firms do with them — are what compound over time. Firms with a consistent testing track record earn faster regulatory approvals, stronger banking partnerships, and smoother investor due diligence. Firms that skip testing accumulate hidden risk that only surfaces under examination, at the worst possible moment and with the most visibility.

Compliance testing is an operational discipline, not a calendar checkbox. The firms that build it into their regular cadence are the ones regulators trust, investors clear faster, and banking partners approve without friction.

Frequently Asked Questions

What is meant by compliance testing?

Compliance testing is the structured process of evaluating whether a firm's controls, policies, and procedures are functioning as intended and aligned with applicable regulatory requirements. It's distinct from simply having written policies — testing verifies that those policies are actually followed in day-to-day operations.

What are the key elements of a compliance program?

A sound compliance program includes a written policy framework, defined controls, ongoing monitoring and testing, staff training, a risk assessment process, and a designated compliance officer responsible for oversight and regulatory reporting.

How is compliance testing different from a compliance audit?

Compliance testing is an ongoing internal process the firm uses to verify controls are working. A compliance audit is typically a formal, periodic review — often conducted by an external party — that evaluates the overall compliance program against regulatory standards.

How often should fintech companies conduct compliance testing?

Higher-risk areas like AML transaction monitoring and KYC should be tested quarterly. Broader policy and procedure reviews are typically done semi-annually, with a full program-level assessment at least annually. New products, regulatory changes, new banking relationships, or operational shifts should each prompt additional testing.

Who is responsible for running compliance testing?

The Chief Compliance Officer or BSA Officer typically owns the compliance testing program, with support from operations and legal teams. For companies without a full-time CCO, fractional compliance leadership can cover this role — owning the testing schedule, conducting reviews, and producing documentation that satisfies regulators and sponsor banks.

What happens if a firm fails a compliance test?

A failed internal compliance test is not inherently negative — it's the purpose of the process. What matters is that the finding is documented, reported to leadership, and remediated with a clear corrective action plan. Leaving a finding unaddressed is what draws regulatory scrutiny — not the finding itself.