Introduction

The FBI reported cybercrime losses hit $20.9 billion in 2025 — a 26% increase from the prior year, driven primarily by investment fraud and business email compromise. Across the Atlantic, payment fraud in Europe reached €4.2 billion in 2024, up from €3.5 billion the year before. Fraud losses are climbing — and banks are squarely in the crosshairs.

Banks face pressure from both sophisticated fraudsters and regulators who expect documented, systematic fraud risk programs. In the US, OCC Bulletin 2019-37 directs all national banks to maintain sound fraud risk management as part of their operational risk framework. That regulatory pressure extends internationally: the UK now mandates reimbursement for Authorized Push Payment (APP) fraud up to £85,000 per claim, making unassessed fraud risk a direct financial liability.

This guide walks through what a bank fraud risk assessment entails: the methodology, governance requirements, and how to build a program that matures over time. It's written for compliance officers, risk managers, and BSA officers who need practical, implementation-ready guidance.

What Is a Fraud Risk Assessment for Banks?

A fraud risk assessment is a structured process for identifying and prioritizing the fraud threats a bank faces, then measuring their potential financial impact. It differs from AML/BSA compliance: where AML programs detect suspicious activity under Bank Secrecy Act requirements, fraud risk assessments focus on operational risk from direct financial crime.

That scope covers two distinct categories:

- Internal fraud — employee misconduct, insider abuse, embezzlement

- External fraud — identity theft, account takeover, authorized push payment (APP) scams, first-party fraud, check fraud

According to the ACFE 2024 Report to the Nations, 22% of occupational fraud cases involve losses of $1 million or more, with a median loss of $145,000 per case. Numbers at that scale are precisely why regulators across jurisdictions now require banks to maintain formal, documented fraud risk frameworks — not as a best practice, but as an expectation tied to supervisory review.

Why Fraud Risk Assessment Is Non-Negotiable

Regulatory scrutiny on fraud frameworks has intensified across jurisdictions:

- United States: The OCC, FFIEC, and federal banking regulators expect documented fraud risk management systems proportionate to each bank's size, complexity, and risk profile

- United Kingdom: The FCA and Payment Systems Regulator now mandate APP fraud reimbursement, effective October 2024, with banks liable for up to £85,000 per claim on Faster Payments and CHAPS

- European Union: The EBA highlights that while strong customer authentication reduced traditional fraud, new manipulation-based fraud types are rising, requiring updated mitigation approaches

Banks that lack a documented fraud risk assessment expose themselves to enforcement actions, consent orders, and direct loss absorption — consequences that a structured framework is specifically designed to prevent.

Types of Fraud Risk Assessments Used by Banks

Banks employ three primary types of fraud risk assessments, each serving distinct operational and regulatory purposes.

Customer Risk Assessment (CRA)

The CRA evaluates the fraud risk posed by individual customers or customer segments. This assessment focuses on the likelihood of first-party fraud (customers misrepresenting information to obtain credit or services) and application fraud (identity theft or synthetic identity fraud at account opening).

CRA factors typically include:

- Transaction volume and velocity patterns

- Account purpose and stated use case

- Identity verification quality and documentation completeness

- Customer behavior consistency with stated profile

- Geographic and jurisdictional risk indicators

Many banks integrate CRA with BSA/AML customer due diligence processes, using existing know-your-customer (KYC) infrastructure to assess fraud risk alongside money laundering risk.

Product Risk Assessment

This assessment evaluates fraud exposure by product line or delivery channel. Different products carry inherently different fraud risks based on transaction speed, verification mechanisms, and recovery capabilities.

According to the 2025 AFP Payments Fraud and Control Survey:

- 63% of organizations experienced attempted or actual check fraud in 2024

- 63% reported wire transfers as the payment method most impacted by Business Email Compromise

- 50% reported ACH credits were targeted by BEC attacks

Cross-border wire transfers and real-time payment rails carry higher inherent fraud risk than in-branch cash transactions. Best practice requires building fraud controls into product design from the outset rather than bolting them on after losses occur.

Enterprise-Wide Fraud Risk Assessment

The enterprise-wide assessment is the most comprehensive of the three. It maps fraud risks across the entire organization and connects directly into the enterprise risk management (ERM) framework, giving fraud risk the same board-level visibility as credit, market, and operational risk.

This holistic view enables banks to:

- Map all fraud threats and assess control effectiveness against each

- Compute residual risk scores to quantify exposure

- Identify control gaps and eliminate redundant processes

- Allocate prevention resources based on data rather than historical budget allocations

The Four-Step Fraud Risk Assessment Methodology

The ACAMS best practice framework — consistent with OCC and FFIEC guidance — breaks fraud risk assessment into four sequential stages, each requiring active stakeholder involvement and documented outputs.

Step 1: Risk Identification

This stage involves building a fraud taxonomy: a structured catalog of all historical, current, and plausible future fraud scenarios relevant to the bank's products, customers, and geographies. The taxonomy should cover:

- First-party fraud: customers intentionally misrepresenting information

- Second-party fraud: money muling and authorized person misuse

- Third-party fraud: account takeover, phishing, business email compromise, identity theft

- Internal fraud: employee embezzlement, insider abuse, unauthorized account access

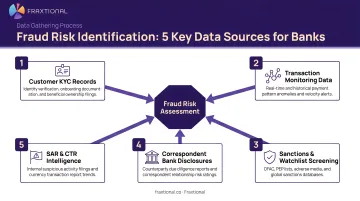

How banks gather this data:

- Structured staff surveys across frontline operations, fraud investigation teams, and business units

- Cross-referencing existing data including fraud loss reports, KPIs, KRIs, and incident logs

- Senior executive interviews to capture strategic risk concerns and emerging threats

- Business unit workshops to identify product-specific and channel-specific vulnerabilities

- External fraud intelligence from industry bodies, peer institutions, FBI IC3 reports, and regulatory bulletins

The output is a comprehensive fraud risk register listing every identified fraud scenario with preliminary severity ratings.

Step 2: Risk and Control Analysis

Risk prioritization comes next. A risk prioritization matrix (heat map) rates each identified fraud risk on two dimensions:

- Likelihood: Probability and frequency of occurrence based on historical data and emerging threat intelligence

- Consequence: Financial loss magnitude, operational disruption, customer harm, and reputational damage

The matrix produces risk scores that allow banks to focus attention on high and very high rated risks rather than spreading resources thinly across all possible threats.

Control mapping follows risk prioritization. For each high-priority fraud risk, identify:

- Preventive controls — multi-factor authentication, segregation of duties, identity verification, dual authorization on wire transfers

- Detective controls — transaction monitoring alerts, anomaly detection, SAR filing trend analysis, complaint review, exception reporting

- Response controls — account freeze procedures, SAR filing workflows, law enforcement coordination, fraud recovery processes

The ACFE 2024 Anti-Fraud Technology Report found that 91% of organizations now use data analysis techniques in anti-fraud programs, with 57% using exception reporting and anomaly detection.

Each control must be assessed for implementation quality and actual effectiveness using audit results, assurance reviews, and testing evidence.

Step 3: Residual Risk Evaluation

After controls are applied, residual risk is what remains. Banks must compare residual risk against documented risk appetite and tolerance thresholds established in their risk management policy.

Decision framework for risks above tolerance:

- Avoid: Exit the business line or discontinue the product

- Accept: Document formal acceptance with enhanced monitoring and board approval

- Test: Pressure-test controls via independent audit or assurance review

- Reduce: Add new controls or enhance existing ones to lower likelihood or impact

Banks may accept residual risk above tolerance when the business benefit outweighs the risk consequence — supporting a high-value correspondent banking relationship is a common example. That decision requires documented justification and formal approval from the senior business owner.

Step 4: Risk Treatment

Risk treatment specifies concrete control actions: maintaining existing controls, enhancing them, or building new ones. Controls fall into three categories:

Prevention (stop fraud before it occurs):

- Real-time behavioral analytics

- Device fingerprinting and biometric authentication

- Mandatory consecutive vacation policies for high-risk roles

Detection (identify fraud as it happens):

- Transaction monitoring with velocity checks and geographic anomaly alerts

- SAR filing trend analysis

- Whistleblower hotlines and exit interview processes

Response (limit damage after fraud is confirmed):

- Account freeze procedures

- Fraud recovery and restitution workflows

- Law enforcement coordination protocols

Once treatment decisions are made, banks should score and prioritize residual risks, then secure formal buy-in from fraud risk owners and control owners. Set implementation timelines and draft the fraud risk assessment report for presentation to the board, audit committee, senior management, and relevant specialists.

Governance, Internal Controls, and Regulatory Compliance

Board Accountability and Oversight

The board is ultimately accountable for fraud risk oversight — a standard OCC Bulletin 2019-37 makes explicit. This means regular reporting on fraud exposure and loss data, backed by a board-adopted code of ethics that sets expectations from the top down.

The board may delegate specific anti-fraud responsibilities to the audit committee, operational risk committee, or named executives, but accountability cannot be fully delegated. Regular board reporting should include:

- Current fraud risk assessment results and residual risk levels

- Fraud loss trends by type (internal, external, product line)

- SAR filing volumes and trends

- Status of fraud risk mitigation initiatives

- Material fraud incidents and lessons learned

Preventive vs. Detective Controls

Preventive controls stop fraud before it occurs:

- Customer Identification Program (CIP) procedures with document verification

- Dual authorization on wire transfers above specified thresholds

- Mandatory consecutive vacation policies for employees with access to funds or sensitive data

- Real-time behavioral analytics that block suspicious transactions before settlement

Detective controls identify fraud after it happens:

- Exception reporting and transaction monitoring alerts

- SAR filing trend analysis to identify emerging fraud typologies

- Whistleblower hotlines for reporting suspected internal fraud

- Exit interview processes that may reveal control weaknesses

Together, these controls form a layered defense — preventive controls reduce how often fraud occurs, while detective controls determine how quickly and decisively the bank responds when it does.

SAR Filing Obligations

Under 12 CFR 21.11, national banks must file a Suspicious Activity Report for known or suspected fraud meeting regulatory thresholds:

| Scenario | Threshold |

|---|---|

| Insider abuse | Any amount |

| Identifiable suspect | $5,000 or more |

| No identifiable suspect | $25,000 or more |

| Potential money laundering or BSA violation | $5,000 or more |

The fraud risk assessment should include workflows that route confirmed or suspected fraud findings into the SAR process and track filing trends as a fraud risk metric.

Audit and Review Requirements

OCC guidance requires that both internal and external audits explicitly cover fraud risk. Sound fraud governance structures include:

- Retrospective reviews — conducted after significant fraud incidents to pinpoint which controls failed and why

- Third-party relationship audits — evaluating vendor access privileges, data handling, and contract-level security obligations

- Independent risk management reviews — verifying that documented controls are actually operating as designed, not just on paper

- Annual fraud risk assessment updates — refreshed to account for new products, delivery channels, and emerging threat typologies

Fraud Risk Monitoring, Measurement, and Reporting

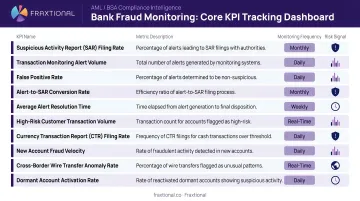

Core Fraud Metrics Banks Should Track

OCC Bulletin 2019-37 outlines specific fraud metrics regulators expect banks to monitor:

- Fraud losses by type (internal, external, loan, card, check, account opening)

- Fraud recovery rates and net fraud losses

- ACH return rates and chargeback volumes

- Number and dollar value of fraud investigations opened

- SAR filing counts and trends

- Civil and criminal subpoena volume

- Percentage of customers claiming victim fraud

Larger, more complex banks typically maintain these metrics in an operational loss database that categorizes and tracks fraud incidents over time, enabling trend analysis and benchmarking.

Live Fraud Risk Dashboards

The ACAMS 2025 guidance highlights the transition to "Live Dashboards" built for board committees to review fraud KRIs and KPIs in near real-time. These dashboards summarize:

- Changes in the threat landscape based on external intelligence

- Recent fraud events and their resolutions

- Top residual risks above risk appetite

- Implementation status of counter-risk initiatives

Effective dashboards make fraud data accessible to non-specialist decision-makers, enabling boards and executive management to fulfill oversight responsibilities without requiring deep technical expertise.

Breaking Down Organizational Silos

Fraud risk is most effectively managed by cross-functional teams bringing together fraud risk, cyber risk, AML, legal, and operations functions. The fraud risk assessment process often reveals synergies: multi-factor authentication protocols deployed in one business unit, for example, can be replicated across others, allowing banks to centralize fraud operations and eliminate redundant controls.

Centralizing those controls matters because fraud schemes routinely exploit the gaps between departments. A single social engineering attack can span multiple risk domains simultaneously:

- Phishing (cyber risk)

- Wire fraud (payments operations)

- Money muling (AML concern)

Without cross-functional visibility, each team sees only its piece — and the scheme falls through the cracks.

How to Strengthen Your Fraud Risk Assessment Program Over Time

Assessment Frequency Best Practices

- Stable, mature banks: Conduct formal annual fraud risk assessments with quarterly dashboard reviews

- Growing banks or banks launching new products: Reassess more frequently, potentially semi-annually or quarterly

- Banks undergoing M&A activity: Conduct assessments before integration and again post-integration

- Trigger-based reassessments: Required after material changes in fraud typologies, regulatory guidance, or the bank's risk profile

The assessment frequency should be documented in the bank's fraud risk management policy and approved by the board.

AI and Technology Tools

Machine learning models, behavioral analytics, and real-time transaction monitoring systems are core components of modern bank fraud programs. According to the ACFE 2026 Anti-Fraud Technology Benchmarking Report, 25% of organizations now use AI/ML in their anti-fraud programs, up from 18% in 2024.

Benefits of AI-powered fraud detection:

- Real-time transaction scoring with adaptive risk models

- Reduced false positive rates through behavioral pattern recognition

- Automated alert prioritization based on risk severity

- Continuous model improvement through feedback loops

Critical limitations:

- Historical training data may contain biases requiring algorithmic transparency

- Explainability remains a challenge — only 6% of organizations feel completely confident explaining how their AI/ML models make anti-fraud decisions

- Generative AI tools can assist in drafting taxonomy frameworks or summarizing fraud intelligence but cannot replace expert judgment, regulatory knowledge, and stakeholder engagement required for compliant fraud risk assessments

What to Do When You Lack Dedicated Fraud Risk Expertise

Many community banks, fintechs, and growing financial institutions don't have a full-time Chief Risk Officer or BSA Officer with deep fraud risk assessment experience. Building this capability in-house requires:

- Hiring senior-level talent with regulatory credentials (CAMS, CFE, ACFE certifications)

- Investing in ongoing training and industry intelligence subscriptions

- Establishing governance structures and reporting frameworks

- Implementing technology platforms for monitoring and case management

For banks not ready to commit to full-time hires, a fractional compliance leader offers director-level fraud risk expertise on a flexible basis. Fraxtional's CRO and BSA Officer services, staffed by CAMS, CBP, and CEP-certified experts with direct examination experience from the OCC, FDIC, and CFPB, deliver the regulatory credibility that sponsor banks and examiners expect.

Frequently Asked Questions

What should be in a fraud risk assessment for banks?

A complete fraud risk assessment covers a fraud taxonomy, a risk and control matrix, residual risk scores benchmarked against risk appetite, and a fraud risk register with assigned owners. Documented control testing and a board-level presentation are required to satisfy examiner expectations.

What methods and frameworks are used in fraud risk assessment for banks?

The core frameworks are the ACAMS four-stage model, the FFIEC BSA/AML Examination Manual, the COSO/ACFE Fraud Risk Management Guide, and OCC Bulletin 2019-37. Banks with significant cyber-adjacent fraud exposure also incorporate ISO 31000 and NIST cybersecurity principles.

What is fraud risk management in banks?

Fraud risk management is the ongoing system of policies, processes, people, and controls a bank uses to identify, measure, monitor, and mitigate both internal and external fraud. It is a form of operational risk management and must be proportionate to the bank's size, complexity, and risk profile, with board oversight and regular reporting on fraud exposure and losses.

Can AI like ChatGPT be used to perform a fraud risk assessment for banks?

AI tools can support specific tasks such as drafting fraud taxonomy categories, summarizing regulatory guidance, or analyzing loss data patterns. However, AI cannot perform a complete fraud risk assessment, which requires human judgment, regulatory expertise, stakeholder interviews, control testing, and documented board-level sign-off to satisfy examiner expectations and meet OCC Bulletin 2019-37 standards.

What tools and software do banks use for fraud risk assessment?

Common tools include transaction monitoring platforms such as NICE Actimize and Verafin (used by over 2,000 banks and credit unions), identity verification systems, operational loss databases, and risk register software for control mapping. The right stack depends on transaction volumes, product complexity, and regulatory footprint.