Introduction

Most financial organizations rely on dozens — sometimes hundreds — of third-party vendors for everything from core banking infrastructure to payment processing, KYC verification, and cloud services. Each relationship carries real operational, financial, and reputational exposure.

The problem is that many organizations manage these relationships reactively. A vendor underperforms, a breach occurs, or a regulator asks questions — and only then does someone scramble for a contract or a due diligence file. In regulated industries like fintech, banking, and crypto, that approach invites exam findings, enforcement actions, and the kind of remediation that takes years to recover from.

According to IBM's 2024 Cost of a Data Breach report, the average breach costs financial firms $6.08 million — 22% above the global average. Meanwhile, the 2024 Verizon DBIR found that 15% of confirmed breaches involved a third party, up 68% year over year.

Those numbers make vendor oversight a board-level concern, not just a compliance checkbox. This guide covers:

- What a vendor management program actually is and why structure matters

- Core components and the five-phase lifecycle

- Compliance requirements for regulated financial services

- Common operational pitfalls and how to avoid them

- Best practices that separate programs that hold up under examination from those that don't

Key Takeaways

- VMPs formalize how organizations select, monitor, and exit vendor relationships — gaps here draw regulatory scrutiny, not just audit findings

- Effective VMPs follow five phases: planning, due diligence, contract negotiation, ongoing monitoring, and exit management

- Regulators treat inadequate vendor oversight as an "unsafe and unsound" practice — examiners act on it

- Risk-tiering is the most practical tool for managing large vendor inventories with limited staff

- Early-stage fintechs can meet sponsor bank and examiner expectations through fractional compliance leadership

What Is a Vendor Management Program and Why Does It Matter?

A vendor management program (VMP) is a structured framework of processes, policies, tools, and governance that guides how an organization selects, onboards, monitors, and exits third-party vendor relationships. The goal is straightforward: get more value from vendors while keeping the risks they introduce under control.

The difference between a VMP and ad hoc vendor oversight shows up fast in practice. Without a formal program, vendor decisions happen in silos:

- A business unit signs a contract nobody in compliance reviewed

- An agreement auto-renews because nobody tracked the expiration date

- Performance reviews never happen, and due diligence documents go stale

By the time an examiner or incident surfaces these gaps, fixing them reactively costs far more than building the program correctly the first time.

The Scale Problem Is Real

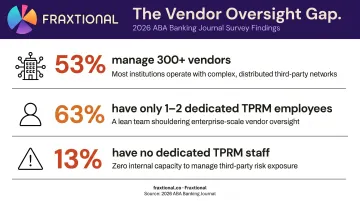

The staffing data makes this gap concrete. A 2026 ABA Banking Journal survey found that:

- 53% of financial institutions manage 300+ vendors

- 63% have only 1–2 dedicated TPRM employees

- 13% have no dedicated TPRM staff at all

That gap between vendor volume and oversight capacity is where risks accumulate. A formal VMP won't shrink that vendor list — but it gives a two-person TPRM team a defensible, documented basis for deciding which vendors get scrutiny first and which ones can wait.

Key Elements of an Effective Vendor Management Program

A VMP is only as strong as its structural components. Five elements are non-negotiable.

Vendor Governance Framework

Every program needs clear ownership. The most widely adopted structure follows a three-lines model:

- First line: Business units owning day-to-day vendor relationships

- Second line: Vendor management and compliance teams handling policy oversight, risk assessment, and escalation

- Third line: Internal audit providing independent validation that the program functions as designed

Defined decision-making authority at each level prevents vendor decisions from defaulting to whoever is loudest or most convenient.

Written Policies and Procedures

Standardized written policies govern vendor qualification, selection, contract execution, performance monitoring, risk assessment, and offboarding. Consistency across these procedures is what protects organizations during audits. Having the policies matters less than demonstrating they're actually followed.

Vendor Risk Management Framework

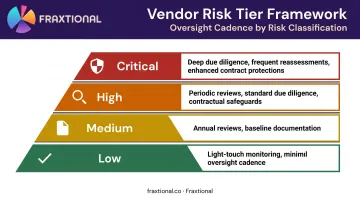

Vendors are not all equal. A SaaS tool for internal scheduling carries very different risk than the payment processor handling customer funds. Effective risk frameworks categorize vendors into tiers and match oversight intensity accordingly:

- Critical: Deep due diligence, frequent reassessments, enhanced contract protections

- High: Periodic reviews, standard due diligence, contractual safeguards

- Medium: Annual reviews, baseline documentation requirements

- Low: Light-touch monitoring, minimal oversight cadence

Contract Standards

Robust vendor contracts should include:

- Clear SLAs and measurable KPIs

- Data protection and confidentiality clauses

- Right-to-audit provisions

- Breach and disruption notification requirements

- Subcontracting limits and disclosure obligations

- Data return and destruction requirements on termination

Templated contract terms reduce negotiation risk and ensure no critical clause is accidentally omitted under deal-time pressure.

Performance Monitoring and Evaluation

Contracts set expectations. Monitoring confirms whether vendors are meeting them. This means tracking SLA performance, conducting periodic reviews, and creating structured feedback loops. Performance data should feed directly into contract renewal decisions. If it isn't influencing outcomes, the monitoring process isn't working.

The Vendor Management Lifecycle: Five Phases Explained

The 2023 OCC/FDIC/Fed Interagency Guidance structures third-party risk management around a five-phase continuous lifecycle. That structure is worth following closely.

Phase 1 — Planning

Before engaging any vendor, define the business case. Determine whether outsourcing is appropriate, assess initial risk and criticality, and establish clear roles for managing the relationship. This phase prevents organizations from inheriting risks they never consciously evaluated.

Phase 2 — Due Diligence and Vendor Selection

Due diligence should be risk-based — the depth of scrutiny should match the vendor's risk tier. For critical vendors, this typically includes reviewing:

- Financial stability and audited financials

- Security posture and SOC reports

- Regulatory compliance history

- Operational resilience and business continuity capabilities

- Sanctions screening where applicable

Total value matters, not just price. A cheaper vendor with poor security controls can create significantly more cost downstream.

Phase 3 — Contract Negotiation

Contract negotiation is where risk mitigation gets embedded in writing — not just price and scope. Key objectives include:

- Establishing measurable performance metrics upfront

- Defining liability clearly and specifically

- Securing audit and access rights that allow independent verification

- Embedding breach notification timelines

- Including termination rights tied to performance failures or changes in risk profile

Never rely solely on vendor-provided performance data. The contract must preserve the organization's right to verify independently.

Phase 4 — Ongoing Monitoring

Continuous oversight is the most resource-intensive phase and the one most organizations underinvest in. It covers:

- SLA tracking against established KPIs

- Periodic risk reassessments triggered by time or material changes

- Due diligence document refresh cycles

- Contract renewal management (before, not after, expiry)

- Rapid response protocols when a vendor's risk profile changes materially

Phase 5 — Termination and Offboarding

Exit planning should happen during onboarding, not when the relationship ends. A clear termination procedure covers:

- Data return or destruction per contractual and regulatory requirements

- Access revocation across all connected systems

- Transition planning to protect service continuity

- Final invoice settlement and contract close-out

For critical vendors, regulators expect documented exit strategies showing the organization could replace the vendor without operational disruption.

Vendor Management in Regulated Financial Services

For banks, fintechs, and crypto firms, vendor management carries real enforcement consequences. It's a regulatory expectation with teeth, not a box to check on a risk framework checklist.

The Regulatory Baseline

US banking regulators (OCC, FDIC, Federal Reserve) hold institutions fully accountable for the actions of their third-party vendors. Inadequate oversight is explicitly classified as an "unsafe and unsound" practice. Recent enforcement actions make this concrete:

- Cross River Bank (2023): FDIC required non-objection approval before new third-party credit products and mandated enhanced third-party compliance controls and board oversight

- Blue Ridge Bank (2024): OCC issued a cease-and-desist covering IT activities provided by third parties and broader risk governance failures

- Evolve Bank & Trust (2024): Federal Reserve found the bank failed to maintain an effective risk-management framework for fintech partnerships, requiring enhanced onboarding, monitoring, and offboarding controls

These aren't outliers. Each action signals what examiners now treat as baseline expectations — and what your own VMP will be measured against.

Jurisdiction-Specific Requirements

Different regulatory frameworks create specific vendor due diligence and monitoring requirements:

| Jurisdiction | Key Framework | Core Vendor Obligation |

|---|---|---|

| US | OCC/FDIC/Fed Interagency Guidance | Full lifecycle risk management; board accountability |

| UK | FCA SYSC 8.1 / PRA SS2/21 | Outsourcing must not impair internal control quality |

| EU | DORA (effective Jan 2025) | ICT third-party risk management; mandatory contract provisions |

| Canada | OSFI Third-Party Risk Management Guideline | Risk-commensurate monitoring for all third-party arrangements |

| Cross-border | GDPR / UK GDPR / PIPEDA | Written contracts with processors; subprocessor controls |

BSA/AML obligations add another layer: FFIEC guidance specifically requires banks serving third-party payment processors to maintain documented policies, procedures, and risk management processes for those relationships.

The Sponsor Bank Problem for Fintechs

Fintechs operating under a bank sponsor arrangement face heightened vendor scrutiny because the sponsor bank is also exposed to the fintech's third-party risk. A weak VMP creates regulatory exposure for the fintech and puts the banking partnership itself at risk.

Early-stage fintechs commonly manage dozens of vendor relationships with no dedicated CCO or BSA Officer on staff. That gap creates exactly the kind of oversight deficiency that sponsor banks and examiners flag. Common consequences include:

- Delayed or revoked sponsor bank approvals due to inadequate third-party controls

- Examiner findings tied to missing vendor management policies or undocumented onboarding

- Increased scrutiny on the sponsor bank, which can tighten the entire partnership

Fraxtional's fractional CCO and CRO services provide director-level vendor oversight that sponsor banks and examiners expect, including vendor management policy development as a core deliverable, without the cost of a full-time executive hire.

Common Challenges in Vendor Management and How to Overcome Them

Resource Constraints and Scale

The staffing gap described earlier isn't a compliance failure — it's a structural reality most organizations need to work within. The practical answer is risk-tiering. Not all 300 vendors deserve the same attention. Concentrating oversight resources on critical and high-risk vendors — those that could cause significant customer harm, operational disruption, or regulatory exposure if they fail — is more defensible than spreading thin coverage uniformly.

Visibility Gaps and Documentation Silos

Contracts in one department, due diligence files in another, and performance notes in somebody's email are common. Examiners find these gaps. The fix rarely requires expensive technology. Standardized intake processes, centralized vendor records, and periodic documentation audits keep files current before an exam or incident forces the issue.

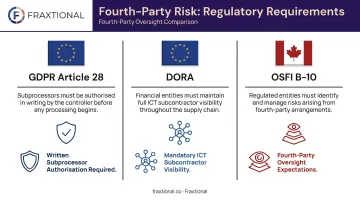

Fourth-Party and Subcontractor Risk

Fourth-party risk — the vendors your vendors rely on — creates hidden exposure that standard vendor oversight doesn't automatically capture. Several regulatory frameworks impose explicit obligations here:

- GDPR Article 28 requires processors to obtain prior written authorization before engaging subprocessors

- DORA mandates contractual visibility into material ICT subcontractors for financial entities in the EU

- OSFI B-10 imposes comparable fourth-party oversight expectations for Canadian federally regulated institutions

The practical approach: require vendors to disclose material subcontractors in their contracts, and add fourth-party review to periodic reassessments for critical vendors. You don't need to audit every fourth party — but you do need to know they exist and have a documented rationale for why they don't introduce unacceptable risk.

Best Practices for Building a Sustainable Vendor Management Program

Build for Adaptability

A VMP built rigidly for today's vendor landscape won't survive the company's next growth phase, new geographic expansion, or regulatory change. Modular program components — policies, risk frameworks, and monitoring procedures that can be updated independently — are far easier to maintain than rigid, all-or-nothing frameworks that require complete rebuilds.

Secure Board and Executive Sponsorship

The 2024 Community Bank Guide is clear: the board bears ultimate responsibility for third-party risk oversight. Without that visibility, vendor management stays understaffed and under-resourced. Board engagement translates directly into budget, accountability structures, and the organizational authority compliance teams need to enforce standards.

For fintechs that aren't ready for a full-time hire, fractional compliance leadership at the CCO or CRO level is a practical way to meet that standard — giving investors and sponsor banks the regulatory depth they expect without the overhead of a permanent executive.

Build in Continuous Improvement Cycles

No program stays current without deliberate review. Schedule regular evaluations to assess whether existing policies, risk tolerances, and monitoring cadences still reflect your vendor landscape and regulatory environment. Key inputs to that review should include:

- Feedback from vendor owners on day-to-day friction points

- Compliance team assessments of policy gaps or outdated controls

- Auditor findings from the most recent review cycle

Examiners charge significantly more than internal reviews — in credibility, remediation cost, and regulatory attention. Finding gaps yourself first is always the better outcome.

Frequently Asked Questions

What is the vendor management process?

Vendor management follows a structured five-phase lifecycle: planning, due diligence and vendor selection, contract negotiation, ongoing monitoring, and termination. Each phase is designed to identify, assess, and manage the risks third-party vendors introduce throughout the entire relationship.

What are the key elements of a vendor management program?

The core components are a governance framework with defined roles, written policies and procedures, a risk management framework with vendor tiering, contract standards, and a performance monitoring process. Done well, these elements produce consistent, auditable oversight that satisfies regulators and survives exam scrutiny.

What is the difference between vendor management and third-party risk management?

The terms are often used interchangeably. Vendor management tends to encompass the full commercial relationship — performance, spend, and contracts — while third-party risk management (TPRM) focuses specifically on identifying and mitigating the risks vendors introduce. In regulated financial services, the two are functionally inseparable.

How do regulated fintech companies approach vendor risk management?

Regulated fintechs must align their VMPs with specific frameworks, including BSA/AML, UDAAP, GDPR, FCA rules, and DORA, and are held fully accountable for their vendors' actions. Due diligence documentation, ongoing monitoring, and board-level oversight are non-negotiable — both for regulatory compliance and for maintaining sponsor bank confidence.

How often should vendor risk assessments be conducted?

Assessment frequency should be risk-based. Critical and high-risk vendors typically warrant annual or more frequent reassessments. Low-risk vendors can be reviewed less often. Reassessments should also be triggered by material changes in the vendor's business, ownership structure, or risk profile — not just the calendar.

What roles are responsible for vendor management within an organization?

Most programs follow the three-lines model. Vendor owners (first line) manage day-to-day relationships; the compliance or vendor management team (second line) handles policy oversight and risk assessment; internal audit (third line) independently validates that the program meets regulatory expectations.