Introduction

Regulatory examinations are no longer a distant concern for fintech, crypto, and banking companies. The FDIC conducted 4,699 examinations in 2024, including 1,214 AML/CFT specialty reviews. The CFPB collected $170 million in civil penalties from 26 defendants in FY2024 alone. In the UK, the FCA issued over £186 million in fines and cancelled 1,456 firm authorizations in 2024/25.

The message is clear: "we'll figure it out when the time comes" is an approach that ends careers and companies.

Sponsor banks have tightened due diligence. Enforcement actions bring compounding consequences:

- Fines and monetary penalties

- License revocations and authorization cancellations

- Reputational damage that follows companies into future fundraising rounds

For fintechs operating across the US, UK, Canada, and EU, the compliance surface area keeps expanding.

This guide breaks down what regulatory readiness actually means, which regulations demand your attention, how to build a compliance program that holds up under scrutiny — and why getting there first is a competitive advantage.

Key Takeaways

- Regulatory readiness is the organizational state of being prepared to meet compliance obligations before regulators or bank partners identify gaps — not after.

- The critical domains include BSA/AML, UDAAP, Reg E, data privacy, and digital asset-specific frameworks across the US, UK, EU, and Canada.

- Every company needs a designated compliance owner (CCO, BSA Officer, CAMLO, or MLRO) supported by documented policies, regular risk assessments, and ongoing training.

- Treating compliance as a continuous program — not a one-time project — is what wins bank partnerships and unlocks faster market expansion.

What Is Regulatory Readiness and Why It Matters

Regulatory readiness is an organization's ongoing capability to meet current and evolving compliance obligations through documented controls, designated ownership, and active monitoring.

The distinction from basic compliance matters. Basic compliance means meeting today's known rules. Regulatory readiness means having systems and people that absorb new rules before those rules create exposure — a meaningful difference in fintech and crypto, where frameworks are still actively being written.

The Stakes Are Financial and Existential

Non-compliance in financial services carries consequences that go far beyond fines:

- License revocations — losing the ability to operate

- Sponsor bank de-risking — the bank ends the relationship, taking the fintech's infrastructure with it

- Exclusion from payment networks — operational shutdown for payment-dependent business models

- Enforcement actions on record — making future partnerships, licensing, and fundraising materially harder

The penalty numbers are stark. FinCEN assessed a $1.3 billion penalty against TD Bank in 2024 and a $3.4 billion civil money penalty against Binance in 2023 — the largest in US Treasury Department history. Both cases trace directly to treating BSA/AML as a back-office function rather than a core operational risk.

The Timing Trap

Regulatory readiness tends to surface as a priority only when a regulatory exam is announced or a sponsor bank raises concerns. By that point, closing documentation gaps and fixing policy deficiencies is expensive and urgent rather than orderly.

Seed-stage and Series A fintechs consistently underinvest in compliance infrastructure, then face a painful ramp-up when scaling, pursuing licensing, or entering a bank partnership. Building proactively costs far less than remediating under pressure — and investors and sponsor banks can tell the difference during due diligence.

The Regulatory Landscape: Key Rules to Navigate

Core US Obligations

The specific obligations depend on product type, customer base, and licensing status. For fintechs, money transmitters, and banking-adjacent firms, the primary frameworks are:

- BSA/AML — written policies, a designated compliance officer, Customer Identification Program (CIP), suspicious activity reporting (SARs), recordkeeping, and independent testing

- UDAAP — CFPB-enforced prohibition on unfair, deceptive, or abusive acts or practices in consumer financial products

- Regulation E — consumer protections for electronic fund transfers, covering dispute resolution, error correction, and disclosure requirements

- State money transmitter licensing — 31 states have enacted the Money Transmission Modernization Act in full or part; multi-state operators need a licensing strategy, not a spreadsheet

The CFPB's larger-participant rule for digital consumer payment applications took effect January 9, 2025. Nonbanks processing at least 50 million annual covered consumer payment transactions are now directly examinable by the CFPB. Large wallets and payment apps that built their models around lighter-touch oversight need to reassess their compliance posture now.

International Regulatory Obligations

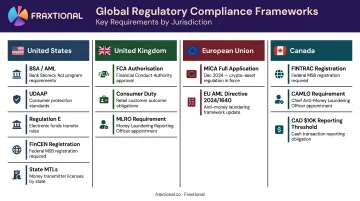

Cross-border operators face overlapping and sometimes conflicting requirements across jurisdictions:

| Jurisdiction | Key Frameworks |

|---|---|

| United States | BSA/AML, UDAAP, Reg E, FinCEN registration, state MTLs |

| United Kingdom | FCA authorization, Consumer Duty (effective July 31, 2023), MLRO requirement |

| European Union | MiCA (full application December 2024), EU AML package (Directive 2024/1640) |

| Canada | FINTRAC registration, CAMLO requirement, large virtual currency transaction reporting at CAD $10,000+ |

MiCA reached full application in December 2024, establishing uniform EU market rules for crypto-assets. EU crypto firms that haven't completed authorization-ready governance, white-paper preparation, and CASP controls are already behind.

A US-built compliance program does not automatically satisfy FCA or FINTRAC obligations. Each regime has its own authorization thresholds, designated officer requirements, and reporting triggers — and regulators in each jurisdiction will expect you to know the difference.

Core Strategies to Build and Sustain Regulatory Readiness

Establish Compliance Leadership and Define Accountability

A designated compliance leader is the single most important element of a regulatory readiness program. Without an owner, there is no one monitoring regulatory changes, managing audit processes, or building relationships with regulators and bank partners.

Many growth-stage fintechs assign compliance responsibility to legal counsel or the CFO. That arrangement has a predictable failure point: a regulatory exam, a sponsor bank audit, or an investor due diligence review — when the absence of a real compliance owner becomes impossible to paper over.

The signals that informal compliance management has been outgrown:

- Sponsor bank conversations stalling in due diligence without clear explanation

- No single person who can articulate the compliance program to an examiner

- Policies that haven't been reviewed since the last licensing application

- SAR filings or transaction monitoring reviews falling behind during leadership transitions

That's why Fraxtional builds policies with version tracking and clear update paths, ensuring documentation reflects current operations — not the company as it existed two product iterations ago. When one Fraxtional client's sponsor bank reviewed their AML policies, they were approved without a single revision. That outcome is what happens when documentation is designed to withstand scrutiny from the start.

Conduct Risk Assessments, Internal Audits, and Mock Exams

A risk assessment is not a checkbox. It is the mechanism by which a company understands where it actually stands relative to regulatory expectations.

The risk assessment process:

- Map high-risk functions: onboarding, transaction monitoring, complaint handling, and vendor relationships

- Compare against regulatory expectations at a granular level, not a high-level gap analysis

- Document gaps prioritized by customer harm risk, financial exposure, and implementation effort

- Remediate with evidence — the corrective action plan becomes proof of proactive management

That prioritized gap list is a powerful artifact to show regulators. It demonstrates that the company identified its own weaknesses before being told to find them.

Internal audits and mock exams take this further. Scheduled compliance audits at regular intervals — FINTRAC requires a two-year effectiveness review by regulation — surface findings on the company's own timeline. Findings identified internally can be fixed before they become regulatory findings.

The Evolve Bank and Trust consent order (2024) and the Blue Ridge Bank order (2024) both cited deficiencies in compliance management, BSA/AML controls, and third-party risk management. In both cases, the issues were not new — they had existed and grown unaddressed. A functioning internal audit and mock exam process would have surfaced those gaps earlier, when remediation was still manageable.

Assessments are most rigorous when the reviewer has distance from the business. External compliance advisors, with no stake in minimizing findings, consistently surface issues that internal self-assessments miss.

Common Gaps That Derail Regulatory Readiness

The same three gaps show up repeatedly in regulatory enforcement actions and sponsor bank due diligence failures.

Treating Compliance as a Project, Not a Program

Companies frequently build compliance infrastructure for a specific trigger — a licensing application, a bank partnership deal — and then fail to maintain it. It's also the most avoidable.

Regulations evolve. Business models expand. A compliance program that was adequate at Series A may be materially deficient by Series B if it hasn't been updated. The Cross River Bank FDIC consent order (2023) cited unsafe and unsound fair-lending practices tied to third-party lending — a business line that had grown without proportionate compliance infrastructure growth.

No Designated Compliance Ownership

Relying on founders, general counsel, or informal arrangements to "handle compliance" creates blind spots that become visible at the worst possible moments. The most common signals:

- No one person can describe the full compliance program in a regulator conversation

- Compliance decisions get made in legal reviews, not compliance reviews

- Key documentation lives in personal folders, not a shared compliance repository

- Leadership transitions create gaps in SAR filings, monitoring reviews, and sanctions checks

A vacant compliance leadership role is an immediate regulatory and operational risk — not just an HR vacancy to backfill on a timeline.

Weak Record-Keeping and Documentation Practices

Regulators and bank partners want evidence, not assurances. Records that must be accessible at any time include:

- Training logs and completion records

- SAR filings and supporting case documentation

- CIP records for customer identification

- Internal audit findings and corrective action plans

- Transaction monitoring alert disposition records

- Sanctions screening logs

Disorganized or incomplete records are themselves a compliance finding — independent of the underlying activity they're meant to document. During a sponsor bank review, failing to produce a training log on request carries the same weight as never running the training at all.

Turning Regulatory Readiness Into a Competitive Advantage

Sponsor Bank Relationships

For fintechs and embedded finance companies, accessing banking infrastructure depends on convincing a sponsor bank that the compliance program is sound — and that confidence needs to be sustained over the life of the partnership, not just at onboarding.

Interagency guidance is clear that using third parties does not diminish a bank's responsibility to comply with law and consumer protection requirements. Banks know this, which is why their due diligence on fintech partners has become far more rigorous following consent orders against Evolve, Blue Ridge, and Cross River.

A well-documented, examiner-ready compliance program shortens the due diligence process and protects the relationship. Fraxtional has direct experience on this front — one prepaid wallet client reported being onboarded by a sponsor bank in under 60 days after Fraxtional introductions and program preparation, after having approached several banks independently with no traction.

Named compliance leadership matters here too. One crypto lending platform that needed to appoint a BSA Officer before their sponsor bank would proceed used Fraxtional to build that function and pass review faster than anticipated.

Investor and M&A Due Diligence

Private equity firms and strategic acquirers treat compliance program maturity as a material factor in valuation and deal timing. Companies that are audit-ready and can articulate a clear compliance story attract faster, cleaner transactions. Companies with unresolved gaps face price adjustments, deal delays, or findings that derail transactions entirely.

One Series A neobank that used Fraxtional to rebuild its AML stack before a funding round found investors impressed with the level of preparation — a detail that shows up in deal dynamics more than most founders expect.

Market Expansion Speed

Regulatory readiness is what allows a company to add new products, enter new geographies, or expand into new customer segments without triggering a compliance remediation cycle first.

Continuous readiness translates directly into speed. Companies that treat compliance as a periodic project have to stop, assess, and rebuild before they can move — while competitors who were already prepared have already moved. The practical differences show up across the business:

- Act on product or geographic expansion without a remediation delay

- Attract enterprise customers who screen counterparties on compliance posture

- Reduce friction in banking partner and distribution channel negotiations

- Enter investor conversations without compliance gaps on the table

Frequently Asked Questions

What is regulatory readiness?

Regulatory readiness is an organization's ongoing capability to meet current and upcoming compliance obligations through documented controls, designated ownership, and active monitoring. It's distinct from passing a single audit: the infrastructure must exist to absorb new rules and adapt before they create exposure.

What regulations do fintech companies need to comply with in the US, UK, and Canada?

In the US, the primary frameworks are BSA/AML, UDAAP, Reg E, and state money transmitter licensing. In the UK, FCA authorization and Consumer Duty apply. In Canada, FINTRAC registration and CAMLO obligations govern. Specific requirements depend on product type, customer base, and licensing status.

When should a startup engage a compliance officer or BSA Officer?

The key trigger points are pre-licensing, pre-bank partnership, and ahead of regulatory supervision. Companies not yet ready to hire full-time can access director-level expertise through fractional compliance models, getting a named compliance leader in days rather than months, at a fraction of the full-time cost.

What is the difference between a CCO, BSA Officer, CAMLO, and MLRO?

The CCO oversees all regulatory obligations broadly. The BSA Officer is the designated AML lead under US law, while the CAMLO fills that same role in Canada under FINTRAC. The MLRO is the UK and EU equivalent, required by FCA-regulated firms.

How do I prepare my company for a regulatory exam?

Start by identifying high-risk functions, conducting an independent risk assessment, closing documentation gaps, and running a mock exam. The corrective action plan from that internal audit is itself evidence of proactive management to examiners.

What does regulatory readiness mean for crypto firms?

Crypto firms face BSA/AML obligations and FinCEN registration in the US, FCA registration in the UK, and MiCA compliance in the EU (full application December 2024). All require AML and KYC programs calibrated to digital asset-specific risks. The regulatory landscape is moving fast. A framework built 18 months ago likely needs revisiting.