Under the Bank Secrecy Act, operating as a Money Services Business (MSB) without registering with FinCEN can trigger civil penalties of $5,000 per day and criminal exposure. Yet the registration process itself is straightforward if you know what's required, when deadlines fall, and what comes after you file.

This guide covers exactly that — from determining whether you need to register, to completing Form 107, to understanding the ongoing obligations that registration triggers.

Key Takeaways

- FinCEN registration (Form 107) is a mandatory federal requirement for MSBs — including money transmitters and crypto firms — and must be filed within 180 days of commencing operations

- File electronically via the BSA E-Filing System — paper filings have not been accepted since 2012

- MSBs must renew every two years by December 31, and retain documentation for five years

- Missing the deadline carries $5,000 per day in civil penalties and potential criminal prosecution

- FinCEN registration is not a license to operate: state money transmitter licenses are separate, additional requirements

What Is FinCEN Registration and Why Does It Exist?

FinCEN — the Financial Crimes Enforcement Network — is a bureau of the U.S. Department of the Treasury. Its mission is to safeguard the financial system from illicit activity, counter money laundering and terrorist financing, and promote national security through financial intelligence.

The legal duty to register rests on 31 U.S.C. § 5330, which requires any person who owns or controls a money transmitting business to register with the Secretary of the Treasury. Congress added this requirement through the Money Laundering Suppression Act of 1994, establishing the first federal registry of non-bank financial institutions in the money services space.

What Registration Actually Does

Registration is how FinCEN's surveillance mandate becomes operational — it's the mechanism by which your business enters the federal compliance framework. Regulators and law enforcement use the registry to identify, monitor, and examine money services businesses. It does not mean you're approved to operate.

FinCEN is explicit on this point: MSB registration is not a recommendation, certification of legitimacy, or endorsement by any government agency. Filing it satisfies a federal reporting requirement — nothing more, nothing less.

FinCEN Registration vs. State Licensing

These are two entirely different things:

| Requirement | Governed By | Purpose |

|---|---|---|

| FinCEN Registration (Form 107) | Federal — BSA | Establishes MSB in federal registry |

| Money Transmitter License (MTL) | State regulators | Authorizes operation within that state |

You need both. FinCEN registration does not authorize you to transmit money in California, New York, Texas, or anywhere else. State MTLs are separate applications with separate regulators, separate fees, and separate timelines.

Who Needs to Register with FinCEN — and Who Doesn't

MSB status is defined under 31 CFR 1010.100(ff). A business qualifies as an MSB if it operates wholly or substantially in the United States in any of these capacities:

- Dealer in foreign exchange

- Check casher

- Issuer or seller of traveler's checks or money orders

- Provider or seller of prepaid access

- Money transmitter

- The U.S. Postal Service (excluding postage/philatelic products)

Fintechs, payment apps, and crypto platforms most commonly fall under category 5 (money transmitter) or category 1 (dealer in foreign exchange).

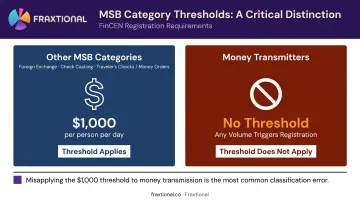

The $1,000 Threshold — and Why It Doesn't Apply to Money Transmitters

For categories like foreign exchange, check cashing, and traveler's checks/money orders, registration is only required if the business exceeds $1,000 per person per day in transactions.

Money transmitters have no such threshold. Under 31 CFR 1010.100(ff)(5), money transmission triggers MSB status regardless of volume. If you transmit money — even a single transaction — you're a money transmitter that needs to register. Misapplying the $1,000 threshold to money transmission is the most common classification error in the space, and it's not a defensible mistake.

Crypto and Virtual Currency Platforms

Per FinCEN guidance FIN-2013-G001, a user of virtual currency is not an MSB. An administrator or exchanger of convertible virtual currency is — treated as a money transmitter, with narrow exemptions. If your platform accepts and transmits crypto, or buys and sells it for customers, you need to register.

The Agent Exemption

A business that is an MSB solely because it acts as an agent of another registered MSB does not need to independently register. The classic example: a supermarket that sells money orders on behalf of a registered MSB is the MSB's agent and doesn't file separately.

The critical qualifier is "solely." If that supermarket also independently conducts MSB activities beyond the agency relationship, it must register on its own.

Who Is Excluded

- Banks as defined under 31 CFR 1010.100(d)

- Persons registered with and functionally regulated by the SEC or CFTC

These entities are explicitly excluded from MSB classification and don't file Form 107.

When the classification question is genuinely unclear, register. The cost of filing is trivial compared to the penalties for operating unregistered.

How to Register with FinCEN: Step-by-Step

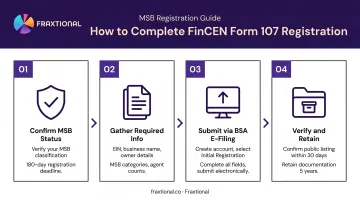

Registration is done entirely online. Paper filings for Form 107 were eliminated as of July 1, 2012. Every filing goes through FinCEN's BSA E-Filing System. The four steps below walk you through confirming your status, gathering your documents, submitting Form 107, and locking in your records.

Step 1: Confirm MSB Status and Identify Your Filing Deadline

The 180-day clock starts the day after your business is established as an MSB — meaning the date it begins offering qualifying services. Missing this deadline is a federal violation under the BSA, regardless of transaction volume.

If you've already passed your deadline, file immediately. Each additional day is a separate violation.

Step 2: Gather Required Information for Form 107

You'll need the following before opening the filing:

- Legal business name and any DBAs/trade names

- Principal business address

- Employer Identification Number (EIN/Tax ID) — missing or incorrect EINs are one of the most common filing errors and will prevent your business from appearing in FinCEN's public MSB Registrant Search

- Owner or controlling person details (name, title, contact information)

- MSB activity categories you're registering under

- Number of branches and number of agents

- Estimated business volume

Step 3: Complete and Submit Form 107 via BSA E-Filing

- Create a BSA E-Filing account if you don't have one

- Start a new RMSB (Registration of Money Services Business) filing

- Select the correct filing type: Initial Registration, Renewal, Re-registration, or Correction

- Complete all required fields — leave nothing blank

- Submit electronically

- Confirm your listing — your business should appear in FinCEN's MSB Registrant Search within approximately 30 days for complete electronic filings

Step 4: Verify Registration and Retain Documentation

FinCEN no longer sends paper acknowledgment letters. Your confirmation is the electronic receipt from BSA E-Filing plus your listing in the public MSB Registrant Search.

Under 31 CFR 1022.380, you must retain the following at a U.S. location for five years:

- A copy of the filed Form 107

- Your registration number (if assigned)

- Business volume estimates, ownership details, and any other supporting documentation used to complete the filing

Ongoing Obligations After FinCEN Registration

Registration is not a one-time event. The CFR creates a calendar of renewal obligations, event-driven re-registration triggers, and examination-ready recordkeeping requirements that run continuously.

Biennial Renewal

MSBs must renew every two calendar years by filing an updated Form 107 by December 31 of the second calendar year. FinCEN does not send reminders. If you miss the renewal, your business is removed from the registrant database and falls out of compliance. There is no grace period.

Set a calendar reminder from the day you file — FinCEN won't follow up.

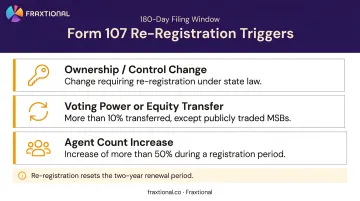

Re-Registration Triggers

Certain business changes require filing a new Form 107 within 180 days of the triggering event:

- A change in ownership or control requiring re-registration under state law

- Transfer of more than 10% of voting power or equity interest (except for publicly traded MSBs)

- An increase in agents of more than 50% during a registration period

Re-registration resets your two-year renewal period from the date of the new filing.

Agent List Requirements

MSBs that use agents must maintain a current agent list containing each agent's name, address, phone number, services provided, transaction volumes, and banking relationship details. This list is revised each January 1 and must be available for examination on request — it is not filed with FinCEN.

BSA Compliance Obligations That Registration Triggers

FinCEN registration triggers the full BSA compliance framework under 31 CFR Part 1022. Registered MSBs are required to:

- Implement a written AML program with internal controls

- Appoint a designated compliance officer (BSA Officer)

- Conduct ongoing staff training

- File Suspicious Activity Reports (SARs) where required

- File Currency Transaction Reports (CTRs) for qualifying transactions

For early-stage fintechs and MSBs without a full-time compliance team, this is where the workload becomes difficult to manage. Building an AML program, appointing a named BSA Officer, and maintaining SAR/CTR workflows requires real compliance depth — not just a checkbox.

Fraxtional places a director-level BSA Officer directly into your team under a fractional engagement, covering AML program development, SAR/CTR workflows, and ongoing monitoring. It's the compliance infrastructure you need without a permanent executive hire.

Common Mistakes and Misconceptions About FinCEN Registration

Mistake 1: Treating Registration as a License to Operate

The most consequential misconception. Appearing on FinCEN's MSB registrant list does not authorize you to offer money transmission services in any U.S. state. State MTLs are entirely separate. Operating in a state without the required license is an independent violation — regardless of your federal registration status.

Mistake 2: Filing Errors That Break the Registration

Common errors that cause Form 107 filings to fail or be incomplete:

- Missing or incorrect EIN — prevents your business from appearing in FinCEN's public database

- Wrong filing type — selecting Renewal instead of Initial Registration, or vice versa

- Blank required fields — particularly business volume estimates and agent counts

- No retained documentation — failing to keep copies of the filing and supporting materials for five years

A correction filing is available if errors are discovered after submission. Use it promptly if you find problems.

Mistake 3: Assuming Registration Completes the Compliance Obligation

Filing Form 107 opens the door — it doesn't close the compliance loop. Companies that register without then building an AML program, appointing a compliance officer, or establishing SAR/CTR procedures face ongoing regulatory exposure from day one.

FinCEN's enforcement record reflects this consistently. In 2019, FinCEN penalized Eric Powers $35,350 for operating as a peer-to-peer virtual currency exchanger without registering as an MSB. In 2017, BTC-e faced a $110,003,314 penalty for operating as an unregistered MSB and willfully violating U.S. AML laws.

For early-stage fintechs that need AML program ownership but aren't ready for a full-time hire, Fraxtional's Fractional Advisory engagement places a named CCO or BSA Officer who takes direct responsibility for documentation, SAR/CTR reporting, staff training, and regulatory filings.

One Series B fintech CEO put it plainly: "After looking around at various options, including the hiring of a full-time BSA Officer, we were convinced that having a fractional resource provided us the most flexibility, but also the most expertise at the best price."

Frequently Asked Questions

How do I register with FinCEN?

File FinCEN Form 107 (Registration of Money Services Business) electronically through FinCEN's BSA E-Filing System within 180 days of establishing your MSB. Paper filings are no longer accepted. Complete all required fields including your EIN, owner details, MSB activity categories, and estimated business volume.

What is the purpose of FinCEN?

FinCEN is a U.S. Treasury bureau that administers the Bank Secrecy Act, analyzes financial intelligence, and works to detect and prevent money laundering and terrorist financing. Its mandate also covers Beneficial Ownership Information reporting under the Corporate Transparency Act.

Does FinCEN still exist?

Yes. FinCEN is an active U.S. Treasury bureau currently administering BSA compliance for all covered financial institutions, including MSBs.

What happens if I miss the 180-day FinCEN registration deadline?

Missing the deadline is a federal violation. Under 31 U.S.C. § 5330 and § 5321, civil penalties can reach $5,000 per day; willful violations also carry criminal exposure with fines up to $250,000, imprisonment up to five years, or both. File as soon as possible if your deadline has passed.

Does FinCEN registration replace state money transmitter licenses?

No. FinCEN registration satisfies the federal BSA filing obligation only. It grants no authority to operate as an MSB in any state. Each state has its own licensing process, requirements, and fees that must be met independently.

How often do MSBs need to renew their FinCEN registration?

Every two years, by December 31 of the second calendar year. FinCEN does not issue renewal reminders. Track this deadline internally — missing it removes your business from the registrant database and creates an immediate compliance gap.