Introduction

Fintech companies, crypto firms, and banks integrating blockchain-based services face a sharp challenge: digital assets introduce familiar financial risks — fraud, money laundering, operational failures — but in an environment traditional risk frameworks were not built to handle. Regulatory obligations are evolving rapidly, and the risk types themselves are unfamiliar territory.

The 2022 crypto winter erased approximately $2 trillion in market value, exposing structural gaps in custody, AML controls, and governance across the industry.

This guide covers:

- Key risk categories unique to digital assets

- The current regulatory landscape across the US, UK, and EU

- Best practices for building a risk program that satisfies sponsor banks and regulators

- When organizations should seek specialized compliance leadership

What Is Digital Asset Risk Management?

Digital asset risk management is the process of identifying, assessing, and mitigating risks associated with cryptocurrencies, stablecoins, NFTs, and other blockchain-based assets. Compliance obligations span the Bank Secrecy Act (BSA), FinCEN requirements, OFAC sanctions, and international frameworks including MiCA and FCA registration.

The foundational framework mirrors traditional finance: assess customer, product, and geography exposure; evaluate controls; close gaps; build governance. What's different is the underlying data environment.

Blockchain transactions are public, permanent, and traceable across wallets and chains — but that transparency comes with new risk vectors:

- Transactions are irreversible, with no chargebacks

- Counterparties may be pseudonymous

- Funds can move across borders and blockchains in seconds

Digital asset risk management applies across entity types: centralized exchanges, DeFi protocols, fintech platforms, money transmitters, embedded finance companies, and traditional banks integrating crypto services. Each has a different exposure profile, but all must address the same core risk categories:

- Operational risk — process failures, third-party dependencies, custody controls

- Cybersecurity risk — wallet exploits, key management, smart contract vulnerabilities

- Market risk — price volatility, liquidity gaps, stablecoin de-pegging

- AML/KYC risk — sanctions exposure, transaction monitoring, customer due diligence

- Fraud risk — account takeover, synthetic identity, social engineering

Key Risk Categories Unique to Digital Assets

Operational Risks

Operational risks in digital assets stem from unregulated or lightly supervised trading platforms, commingled customer assets, and inadequate custody safeguards. Firms must verify whether platforms they work with are registered as Money Service Businesses (MSBs) with FinCEN and licensed in relevant states. Under FinCEN guidance FIN-2019-G001, persons accepting and transmitting convertible virtual currency are classified as money transmitters and must register as MSBs.

Key operational vulnerabilities include:

- Platform supervision gaps: Many exchanges operate without federal or state registration

- Commingled assets: Customer funds mixed with operational capital, creating insolvency risk

- Custody failures: Inadequate controls over private keys or multi-signature wallets

Cybersecurity Risks

Crypto platform hacks resulted in $2.2 billion stolen in 2024 across 303 incidents — making cybersecurity one of the most direct threats to digital asset operations. The three primary attack vectors are direct hacks on hot wallets and exchanges, phishing campaigns impersonating trading platforms, and loss or theft of private keys.

Unlike traditional banking, on-chain transactions are irreversible. The Financial Stability Oversight Council (FSOC) explicitly warns that the "near immutability" of distributed ledger transactions means they "may be reversed only under certain relatively limited circumstances." There are no chargebacks. Once assets are sent, they cannot be recalled.

Market Risks

Beyond custody and cybersecurity, market structure itself introduces significant exposure. Digital asset markets are characterized by high price volatility, liquidity risk, stablecoin run risk, and counterparty risk. In May 2022, the algorithmic stablecoin TerraUSD (UST) depegged, resulting in an $18.5 billion loss — demonstrating how panic-driven depegging can cascade across the entire ecosystem.

Primary market risks:

- Prices can swing double-digit percentages within hours

- Thinly traded assets are difficult to exit without moving the market

- Rapid redemption demand can break a stablecoin's peg

- Once transferred, assets cannot be recalled from a defaulting counterparty

AML/KYC Risks

Permissionless blockchain environments make KYC verification difficult, elevating AML risk. FATF guidance notes that permissionless environments pose distinct AML/CFT challenges because the underlying protocols do not require identification or verification of participants.

Compliance programs must go beyond replicating traditional finance AML methods. Blockchain's traceability can enhance detection — every transaction is recorded on a public ledger — but this requires specialized tooling beyond standard AML workflows:

- Multi-hop tracing to follow funds across layered transactions

- Wallet screening against sanctions lists and flagged addresses

- Cross-chain analysis to track assets moving between blockchains

Fraud Risks

Digital asset fraud is dominated by social engineering schemes. Social media is the top contact method by aggregate reported losses for cryptocurrency investment scams, often termed "pig butchering." Chainalysis estimates $17 billion was stolen in crypto scams and fraud in 2025.

Common fraud vectors:

- Social media scams: Fake investment platforms promoted through messaging apps and social networks

- Interface manipulation: Fraudulent trading platforms or wallet interfaces designed to steal credentials

- Impersonation: Criminals posing as legitimate exchanges or customer support to redirect funds

The Regulatory Compliance Landscape for Digital Assets

US Federal Framework

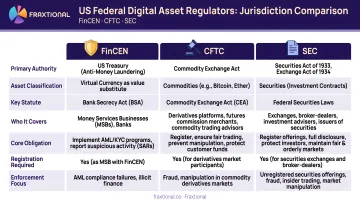

Three federal regulators share oversight of the US digital asset space, each with distinct jurisdiction:

- FinCEN: Requires digital asset platforms serving US customers to register as MSBs and implement BSA-compliant AML programs

- CFTC: Oversees derivative and leveraged digital asset products

- SEC: Has jurisdiction over digital assets classified as securities

In March 2026, the SEC and CFTC issued a joint interpretation clarifying how federal laws apply to crypto assets — specifically distinguishing digital commodities from digital securities.

The GENIUS Act (signed July 2025) establishes a federal regulatory framework for stablecoin issuers. Permitted payment stablecoin issuers (PPSIs) must maintain 1-to-1 reserves using US currency, demand deposits, or short-term Treasury bills. They are also explicitly subject to the Bank Secrecy Act, requiring effective AML and sanctions compliance programs.

State-Level Requirements

Federal registration doesn't eliminate state-level obligations. Many states require separate money transmission licenses, and 31 states have enacted the Conference of State Bank Supervisors (CSBS) Money Transmission Modernization Act (MTMA) to harmonize standards — but individual state licenses are still required. Firms operating across multiple states must track each jurisdiction's specific requirements, timelines, and renewal obligations independently.