This scenario plays out regularly across fintech, crypto, and embedded finance. Operational due diligence (ODD) is the moment where a company's internal readiness gets stress-tested by someone with the authority to walk away.

This guide covers what ODD actually is, the five areas it examines, how the process works step by step, and why compliance has become the central gating factor for financial services companies facing investor or sponsor bank scrutiny.

Key Takeaways

- ODD is forward-looking diligence: it evaluates whether an operating model can actually deliver on the deal thesis, not just whether the historical numbers are clean

- Five core areas: organizational structure, operational processes, technology, compliance/risk management, and human capital

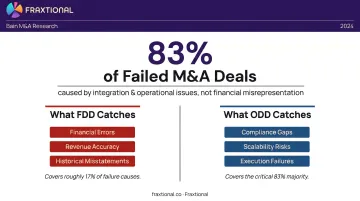

- Bain research links integration failures to 83% of failed M&A deals—ODD surfaces those risks before you sign

- For fintechs and crypto firms, compliance maturity is a gating factor—not one checkbox among many

- Fractional compliance leadership directly addresses the most common ODD red flag: no visible compliance executive

What Is Operational Due Diligence?

Operational due diligence is an investigative review of how a target company actually operates: its processes, management structure, technology, and risk controls, and whether the business is sustainable, scalable, and capable of delivering value after the deal closes.

Deloitte describes ODD as a "bespoke, continuous, and iterative process" for formulating and testing an investment thesis. Unlike financial due diligence, ODD is forward-looking — it assesses what a buyer or investor can actually do with a business once they own or partner with it.

What ODD Is Trying to Answer

- Can this business execute its plan with the people and systems it currently has?

- What operational risks could derail the deal or erode value post-close?

- Where are the value-creation opportunities that aren't visible in the financials?

When ODD Gets Triggered

ODD surfaces across more deal types than most teams expect:

- M&A transactions — the acquiring party assesses whether the target can integrate and operate under new ownership

- Private equity investments — PE firms test whether the portfolio company can deliver the projected returns

- Capital raises (Series A/B) — investors assess operational maturity before committing capital

- Sponsor bank partnerships — banks conduct ODD-style reviews before agreeing to sponsor a fintech's banking products, because FDIC guidance is clear that a bank's use of a fintech does not reduce its own regulatory accountability

Key Areas Assessed During Operational Due Diligence

ODD scope is tailored to the deal and the company. That said, five areas appear in almost every ODD exercise regardless of context.

Organizational Structure and Management

Reviewers assess the management team's experience, track record, and capacity to execute—particularly under new ownership or a new partnership structure. Key-person risk gets examined closely here. If one individual holds critical relationships, institutional knowledge, or decision-making authority, their departure post-deal could derail operations entirely.

Operational Processes and Systems

Day-to-day workflows, supply chain (or service delivery) dependencies, IT infrastructure, and data security protocols all come under review. The central question is scalability: can existing processes support projected growth without requiring disproportionate capital investment?

Technology, Data, and Cybersecurity

Every financial services company is a technology company. ODD evaluates whether systems are current, secure, and compatible with the buyer's or partner's infrastructure. Security debt — the accumulated risk from deferred patching, outdated architecture, and unresolved vulnerabilities — can reshape deal terms or trigger renegotiation.

Risk Management and Regulatory Compliance

For financial services companies, this is where ODD most often determines deal outcomes. Reviewers check:

- Licensing status and regulatory standing

- AML/KYC program design and enforcement

- Consumer protection and data privacy frameworks

- Cybersecurity governance and incident response

Gaps in any of these areas are among the most common deal-breakers.

Human Capital and Culture

Workforce strategy, retention rates, and organizational culture get evaluated because culture determines whether post-transaction operational improvements can realistically be implemented. Cultural misalignment is consistently underestimated as a deal risk—and frequently surfaces as a problem 12 months after close.

Operational Due Diligence vs. Financial Due Diligence

The distinction is straightforward: financial due diligence looks backward, ODD looks forward.

| Financial Due Diligence | Operational Due Diligence | |

|---|---|---|

| Focus | Historical financial performance | Future operational capacity |

| Key questions | Are the numbers accurate? Is the business economically sound? | Can this business scale? What risks exist post-close? |

| Primary outputs | Valuation support, SPA inputs | Value-creation plan, risk register |

| Time orientation | Backward-looking | Forward-looking |

FDD validates the price. ODD validates whether that price is achievable.

Why ODD Can't Be Skipped

Bain's research on M&A outcomes is unambiguous: when deals fail, integration issues are at the root 83% of the time. Not financial misrepresentation—execution and operational failures. FDD may confirm that the revenue is real, but it won't tell you whether the company's compliance program will survive sponsor bank scrutiny or whether its tech stack can handle 10x transaction volume.

The Broader Due Diligence Ecosystem

ODD sits alongside several other workstreams that feed into a complete picture:

- CDD (Commercial Due Diligence) — market position and competitive landscape assessment

- LDD (Legal Due Diligence) — contracts, IP, litigation exposure

- ITDD (IT Due Diligence) — technology architecture, integration requirements

- HCDD (Human Capital Due Diligence) — workforce, org structure, compensation

- VDD (Vendor Due Diligence) — sell-side ODD the seller commissions to build buyer confidence and accelerate the process

The Operational Due Diligence Process: A Step-by-Step Framework

Most effective ODD exercises follow a four-stage structure, even when the specific scope varies by deal.

Stage 1: Initial Operational Overview

This is rapid triage. The goal is to determine whether a deeper dive is warranted before significant resources are committed. Reviewers identify strategic fit, flag obvious deal-breakers, and surface potential quick wins. If nothing disqualifying appears, the process advances.

Stage 2: Document Review

This stage verifies what management has represented. Key review areas typically include:

- Internal compliance policies and procedures

- Relevant licenses and regulatory permits

- Technology stack documentation and IP ownership

- KPI benchmarking against industry comparators

- AML program documentation, SAR/CTR procedures, and KYC frameworks

Organized, well-maintained documentation signals operational maturity. A data room that requires extensive back-and-forth to assemble signals the opposite.

Stage 3: Management Deep Dive

Structured interviews with operations managers and department heads cover physical or digital infrastructure and process bottlenecks. For remote-first financial services companies, this typically means virtual sessions with department heads and direct access to system environments.

This is also where compliance leadership gets tested directly. Investors and sponsor banks want to speak with a designated BSA Officer or CCO — not a founder who "handles compliance." The absence of named compliance leadership at this stage raises immediate questions.

Stage 4: Value Creation Projections and Reporting

Findings are synthesized into an ODD report covering:

- Prioritized value-creation opportunities

- Capital investment required to bring operations to target standard

- Post-merger or post-partnership integration synergies

- Realistic implementation timeline with clear ownership

A complete ODD report — spanning management, operational processes, technology, compliance, data management, and HR — gives deal teams the evidence they need to negotiate terms, set integration priorities, and move forward with confidence.

Why Compliance Is a Make-or-Break Factor in ODD for Fintech and Crypto Companies

For regulated financial services companies, compliance isn't one section of an ODD checklist. It's often the single factor that determines whether a deal proceeds.

FDIC guidance makes the bank perspective explicit: before entering a fintech partnership, banks should review the fintech's business experience, financial condition, legal and regulatory compliance, risk management and controls, information security, and operational resilience. The bank retains full regulatory accountability regardless of what the fintech has or hasn't built.

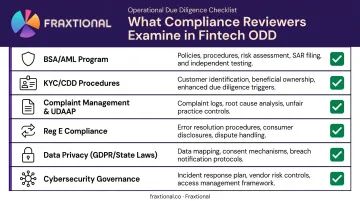

What Compliance Reviewers Actually Examine

In financial services ODD, compliance review goes well beyond asking whether policies exist. Reviewers want evidence:

- BSA/AML program: design, effectiveness, documentation, and independent audit history

- KYC/CDD procedures: beneficial ownership identification, customer risk profiles, ongoing monitoring

- Complaint management, disclosure practices, and fair treatment controls (UDAAP)

- Electronic fund transfer disclosures and error resolution procedures (Reg E, US companies)

- Data privacy: GDPR compliance for EU/UK entities, state privacy law compliance for US operations

- Cybersecurity governance: ICT risk framework, incident response, third-party security oversight

For crypto firms specifically, the bar is higher. The FCA supervises UK cryptoasset businesses under AML/CTF rules and requires registration before services can be provided. FinCEN applies Bank Secrecy Act rules to money transmission denominated in convertible virtual currency. Gaps in AML controls aren't just a compliance concern; they're a licensing and operational viability issue.

Compliance Maturity as an ODD Signal

A company with a documented compliance program, a designated compliance officer, regular independent audits, and clear escalation protocols sends a credible signal to reviewers. That credibility is built on evidence, not verbal assurances.

A company relying on informal compliance processes raises immediate flags. A founder who describes compliance as "something we're still building out" will delay or derail the review outright.

This is where engaging a fractional CCO, BSA Officer, or MLRO becomes practical rather than optional. Fraxtional's compliance leaders serve as named officers on regulatory filings, manage AML programs built to FFIEC and FinCEN standards, and participate directly in investor and sponsor bank conversations.

What that looks like in practice:

- Named officer placement on regulatory filings (CCO, BSA Officer, MLRO, CAMLO)

- Board-approved policies and procedures aligned to FFIEC and FinCEN standards

- Direct participation in investor and sponsor bank due diligence conversations

One CEO from a Series A neobank described the process: "Our investors were impressed with how ready we were" — after rebuilding their entire AML stack before a funding round with Fraxtional's support.

For early-stage companies that can't justify a full-time compliance executive, fractional leadership provides director-level expertise at a fraction of the cost. It closes the single most visible gap ODD reviewers flag.

Common Challenges in Operational Due Diligence

Poor Documentation Practices

Companies with inconsistent record-keeping or no centralized compliance files slow ODD down and signal operational immaturity. The mitigation is straightforward: treat audit-readiness as a continuous posture, not a pre-deal scramble.

Core documentation to maintain on an ongoing basis:

- Current AML/BSA policies with version history

- KYC/CDD procedures with evidence of implementation

- Independent audit reports from the past 12–24 months

- SAR/CTR logs and escalation records

- Licensing documentation for all operating jurisdictions

Time Pressure

ODD runs against deal timelines. The risk is missing material issues because reviewers had to move faster than the evidence warranted. Structured checklists, divided workstreams, and prioritizing high-risk areas first—compliance chief among them—help manage this without sacrificing accuracy.

Expertise Gaps on the Reviewing Team

Time pressure compounds when the reviewing team also lacks sector-specific knowledge. When a buyer or investor is less familiar with the target's vertical—particularly in crypto, BaaS, or embedded finance—ODD quality suffers without the right subject-matter expertise. A generalist reviewer often lacks the benchmarks to evaluate what a credible crypto AML program actually requires.

Engaging external specialists with deep regulatory knowledge of the target's operating jurisdictions closes this gap. Fraxtional's independent audit services help firms prepare for sponsor bank due diligence or investor reviews, delivering prioritized remediation findings that give reviewers an objective, third-party read on compliance program quality.

Frequently Asked Questions

What does operational due diligence do?

ODD investigates whether a company's operations, processes, and management structure are sustainable and scalable, and whether they can deliver on the deal thesis. It identifies operational risks and value-creation opportunities before a transaction closes, giving buyers and investors a realistic picture of what they're actually acquiring.

What is the difference between CDD and VDD?

CDD (Commercial Due Diligence) is buy-side work: the investor assesses the target's market position and competitive landscape. VDD (Vendor Due Diligence) is sell-side, where the company being acquired commissions its own review proactively to build buyer confidence, surface issues early, and accelerate the process.

What is the difference between operational due diligence and financial due diligence?

Financial due diligence analyzes historical financials to validate economic value. ODD examines how the business will actually operate and create value post-transaction. Both are necessary, but only ODD tells you whether the operating model can deliver what the financial model projects.

What are common red flags found during operational due diligence?

The most frequently surfaced issues include:

- Key-person dependency

- Outdated or non-scalable technology

- Weak or undocumented compliance programs

- No designated compliance officer

- Supply chain or partner concentration risk

- Poor data management practices

- High employee turnover in critical functions

How long does operational due diligence typically take?

Timelines vary by deal complexity, company size, data room quality, and regulatory exposure. Smaller transactions may complete ODD in a few weeks; complex M&A or PE deals can run several months. ODD typically runs in parallel with other diligence workstreams rather than sequentially.

What triggers an ODD review for fintech or crypto companies?

The most common triggers are a capital raise (Series A or B), a private equity investment, an acquisition, or a sponsor bank partnership application. Investors and banks increasingly conduct ODD specifically to assess compliance maturity—because in regulated financial services, operational and compliance readiness are inseparable.