Introduction

Most fintechs and financial firms discover their KYC compliance gaps at the worst possible moment — during a sponsor bank review, a regulatory examination, or when trying to launch in a new market. By then, what looked like a manageable checklist has become a complex, multi-jurisdictional obligation with real consequences attached.

Regulators don't grade on a curve. FinCEN assessed a $1.3 billion penalty against TD Bank in 2024 — the largest ever against a US depository institution. The UK's FCA fined Starling Bank £28.96 million in 2024 for opening accounts for high-risk customers despite agreed restrictions.

Neither was a small or unsophisticated firm. That's exactly the gap KYC consulting exists to close.

This guide covers what KYC consultants actually do, the four program pillars they build and maintain, when to bring one in, how requirements differ across the US, UK, EU, and Canada, and how to evaluate the right partner.

Key Takeaways

- KYC is an ongoing regulatory obligation — not a one-time onboarding step — and the penalties for getting it wrong are substantial

- KYC consultants design programs, run gap analyses, select vendors, and represent you to regulators and sponsor banks

- Every KYC program rests on four pillars: CIP, CDD, EDD, and Ongoing Monitoring

- Bring in a consultant at launch, during regulatory scrutiny, when scaling, or when a full-time hire isn't practical

- Fractional compliance models give early-stage companies director-level expertise without the full-time cost

What Is KYC and Why Does It Require Specialist Oversight?

Know Your Customer (KYC) refers to the policies, procedures, and controls financial institutions use to verify customer identities, assess risk profiles, and monitor activity to prevent money laundering, fraud, and terrorist financing. It is not a one-time onboarding event. Regulations treat it as a continuous obligation that evolves with each customer relationship.

The compliance challenge is that KYC looks deceptively straightforward until you try to build a defensible program. Several factors make it genuinely hard:

- Jurisdictional variation — FinCEN, FCA, FATF, and FINTRAC each impose distinct requirements that don't map neatly onto each other

- Business model specificity — a crypto exchange, a lending platform, and a prepaid card program face different customer risk profiles and need different control architectures

- Enforcement consequences — regulatory fines, license revocation, and sponsor bank termination are all real outcomes, not theoretical ones

The enforcement record speaks for itself. FinCEN's 2023 $3.4 billion civil money penalty against Binance for willful Bank Secrecy Act violations — including a five-year monitorship — illustrates what happens when a high-volume business treats KYC as an afterthought.

The FCA fined Guaranty Trust Bank UK £7.67 million in 2023 for inadequate customer risk assessments and transaction monitoring. The FCA cited a prior £525,000 fine from 2013 for the same systemic failings — meaning a decade passed without the bank fixing its core problems.

Most early-stage and mid-market companies lack the internal depth to design and run a defensible KYC program. The median US compliance officer salary was $78,420 as of May 2024 — but a single compliance officer rarely has the multi-jurisdictional regulatory expertise a growing fintech actually needs. KYC consultants fill that gap: they bring multi-jurisdictional program experience, cross-vertical pattern recognition, and regulatory credibility — without the overhead or lead time of a full executive search.

What Does a KYC Consultant Actually Do?

KYC consulting is not purely advisory. Depending on the engagement, a consultant may design, build, review, or operationally run a KYC program. The three most common engagement types are:

- Program build-out — designing a KYC program from scratch for a new regulated business

- Gap analysis and remediation — reviewing an existing program against regulatory requirements and producing a remediation roadmap

- Ongoing fractional leadership — acting as the embedded compliance director on a continuing basis

Program Design

At the program design stage, consultants develop the core policy documentation a regulated business needs:

- Customer Identification Program (CIP) policies

- Risk appetite statements and customer acceptance policies

- AML/KYC procedures tailored to the company's onboarding channel

- Board-approved compliance frameworks with version tracking and role-based responsibilities

The goal is documentation that holds up to sponsor bank scrutiny and regulator review — not generic templates. Fraxtional's approach, for example, produces policies built around a client's actual product structure, team, and regulatory exposure, not off-the-shelf frameworks that require significant rework before passing sponsor bank or regulatory review.

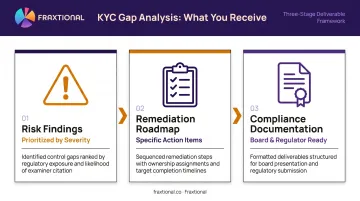

Gap Analysis and Audit

Gap analysis engagements review existing KYC processes against regulatory requirements and surface specific deficiencies. Common findings include:

- Missing Enhanced Due Diligence triggers

- Inadequate PEP screening coverage

- Incomplete beneficial ownership documentation

- Transaction monitoring rules not calibrated to the business's actual activity patterns

Outputs typically include prioritized risk findings organized by severity, remediation roadmaps with specific action items, and compliance-ready documentation suitable for board review or regulatory response.

Operational Build-Out and Technology

Once the program framework is in place, consultants help select and implement the technology layer. This typically covers:

- Sanctions screening tools and PEP databases

- Adverse media feeds and document verification systems

- Transaction monitoring platforms

The selection process involves evaluating vendor fit for the business's product type and volume, then overseeing implementation and rule calibration so the system works in practice — not just on paper.

Regulatory Liaison and Sponsor Bank Support

Experienced KYC consultants often act as the compliance interface with regulators and sponsor banks. This includes preparing documentation for pre-deal due diligence, responding to examiner inquiries, and representing the business's compliance posture in bank onboarding processes. For fintechs seeking BaaS or sponsor bank relationships, this function alone can be the difference between a 60-day onboarding and a stalled deal.

The Four Pillars of a KYC Program

KYC consultants work within a structural framework built on four core components. Understanding these pillars helps clarify what consultants are actually building or fixing.

Customer Identification Program (CIP)

CIP is the foundation — documented policies and procedures for collecting, verifying, and recording customer identity information before a financial relationship begins. Under 31 CFR 1020.220, US banks must maintain written, risk-based CIP procedures covering name, date of birth, address, and identification number at minimum.

Consultants ensure CIP policies meet jurisdiction-specific requirements and are actually executable for the company's onboarding channel — digital, in-person, or hybrid. A CIP designed for branch banking doesn't work for a mobile-first crypto platform, and vice versa.

Customer Due Diligence and Enhanced Due Diligence

CDD involves assessing each customer's risk profile — source of wealth, intended transaction behavior, and beneficial ownership for business customers. FinCEN's CDD Final Rule requires covered financial institutions to identify and verify beneficial owners using a 25% ownership prong plus a control prong.

EDD applies to higher-risk customers, including:

- Politically exposed persons (PEPs)

- Customers from high-risk jurisdictions

- Unusual or complex business structures

FATF Recommendation 10 requires ongoing monitoring and EDD controls — including senior management approval and source of funds verification for foreign PEPs.

Consultants define the risk thresholds, screening triggers, and escalation protocols that determine when EDD applies. Without those defined criteria, firms either over-trigger EDD (creating operational bottlenecks) or miss it entirely (creating regulatory exposure).

Ongoing Monitoring and Periodic Review

KYC doesn't end at account opening. Consultants design transaction monitoring frameworks and periodic review cadences tiered by risk level. High-risk customers require more frequent review than low-risk ones, and the monitoring rules need calibration to the business's specific transaction patterns and product types.

Perpetual KYC (pKYC) takes this further — replacing static periodic reviews with automated, real-time monitoring that flags changes in customer behavior or profile as they happen. Rather than revisiting a file every few years, the system reacts continuously. KYC consultants advising on pKYC focus on the data infrastructure and vendor integrations required to make it operational, not just the concept.

When Should Your Business Bring In a KYC Consultant?

There are four clear triggers for engaging external KYC expertise:

1. Startup and Launch Building a new financial product — payments, lending, crypto, embedded finance — requires a KYC program before go-live. Sponsor banks and regulators expect a functioning program, not a plan to build one. Consultants design the program from scratch, ensuring it satisfies sponsor bank requirements from day one. Fraxtional clients have cited scenarios where fixing a KYC policy within days avoided onboarding delays with sponsor banks — delays that would otherwise have cost weeks.

2. Regulatory Examination or Enforcement Action When a company receives a regulatory inquiry or enforcement action related to AML/KYC deficiencies, bringing in a consultant to lead remediation is typically required. The consultant acts as both a technical advisor and a credibility signal to regulators, demonstrating the company has engaged qualified help and is taking findings seriously.

3. Scaling and Entering New Markets Crossing a regulatory threshold, launching in a new jurisdiction, or acquiring customers in a higher-risk segment often makes an existing KYC program inadequate. Starling Bank's £28.96 million fine is a concrete example: the firm opened over 54,000 accounts for 49,000 high-risk customers despite agreed restrictions. Scaling without updating the KYC program to match the risk profile is a common and expensive mistake.

4. Cost and Capacity Constraints Many companies at seed and Series A stages cannot justify a full-time Chief Compliance Officer or BSA Officer. A fractional KYC compliance consultant provides director-level expertise and ongoing program ownership at a fraction of the cost. Fraxtional clients typically save 50–70% compared to a full-time executive hire.

Fraxtional's fractional model directly addresses this gap. Directors embed into the business under named titles, with scope that adjusts as the company grows:

- Named title use: CCO, BSA Officer, MLRO, or CAMLO — without a full-time hire

- Active participation: attending internal meetings, owning deliverables, and representing the company to banks and regulators

- Flexible scope: engagement scales with funding stage, transaction volume, and jurisdictional complexity

KYC Consulting Across Jurisdictions: US, UK, EU, and Canada

KYC obligations differ materially across jurisdictions. A program designed for one market won't automatically satisfy another.

| Jurisdiction | Primary Regulator | Key Framework | Notable Requirement |

|---|---|---|---|

| United States | FinCEN | Bank Secrecy Act / USA PATRIOT Act | Written CIP, CDD Final Rule, SAR filing, state MTLs |

| United Kingdom | FCA | Money Laundering Regulations 2017 | MLRO appointment, business-wide risk assessment |

| European Union | AMLA (from 2028) | Regulation (EU) 2024/1624 | Harmonized AML/CFT obligations across member states |

| Canada | FINTRAC | Proceeds of Crime Act | Compliance officer appointment, effectiveness testing every 2 years |

US: The BSA and USA PATRIOT Act require a Customer Identification Program, Suspicious Activity Report filing, and ongoing AML monitoring. FinCEN oversees federal compliance, while state-level money transmitter licenses add jurisdiction-specific requirements. The Conference of State Bank Supervisors reports that 31 states have enacted the Money Transmission Modernization Act, covering 99% of reported money transmission activity.

UK and EU: The FCA supervises UK firms under the Money Laundering Regulations 2017. Core obligations include:

- Business-wide risk assessments and proportionate controls

- Customer due diligence (CDD) and enhanced due diligence (EDD) for higher-risk customers

- Continuous monitoring of customer relationships

- MLRO appointment for regulated firms

The EU is building out AMLA as a centralized supervisory authority, with direct oversight of 40 high-risk financial institutions beginning in 2028. Post-Brexit, UK and EU rules have diverged significantly — firms operating in both markets need a consultant with genuine cross-border experience.

Canada: FINTRAC administers Canada's AML/KYC regime under the Proceeds of Crime (Money Laundering) and Terrorist Financing Act. The CAMLO designation is a required role for many regulated entities — not a title that can be left unfilled at a supervised firm. Fraxtional's Canadian practice, led by a CAMS-certified CAMLO with nine years of experience across money remittance and digital assets, supports clients on FINTRAC compliance and high-risk geographic assessments.

How to Choose the Right KYC Consultant

Three criteria matter most:

Jurisdictional depth. Check whether the consultant has direct regulatory experience in your specific markets — not just familiarity with general principles. A consultant who knows FinCEN requirements well but has never worked with the FCA or FINTRAC isn't the right choice for a multi-market fintech.

Business model alignment. KYC for a crypto exchange looks different from KYC for a lending platform or a prepaid card program. The risk profiles, customer types, and screening requirements differ significantly. A consultant who has only worked with traditional banks may produce a technically compliant but operationally misaligned program.

Senior-led delivery. Large consulting firms frequently deploy junior analysts while senior partners remain distant. For KYC engagements — which require regulatory credibility, sponsor bank relationships, and judgment calls that templates can't resolve — that model produces slower results and weaker outcomes. Boutique and fractional compliance firms that provide director-level ownership of every engagement tend to be more effective.

Fraxtional's structure is built around this principle. Directors attend every client call, review policies directly, and handle sponsor bank and investor Q&A — there's no hand-off to junior staff. One client put it plainly:

"The director was on every call and reviewed every policy as if she were part of the internal team."

Watch for these red flags when evaluating KYC consultants:

- Generic policy templates not tailored to the business model or onboarding channel

- No direct experience with sponsor bank due diligence processes

- Unfamiliarity with regulators in your specific jurisdiction

- No clear plan for scaling support as the business grows

- Inability to take a named compliance role if required

Frequently Asked Questions

What is a KYC consultant?

A KYC consultant is a compliance professional who helps businesses design, implement, and manage Know Your Customer programs, covering identity verification, risk frameworks, AML screening, and regulatory documentation. Engagements range from one-time program builds and gap analyses to ongoing advisory or fractional leadership arrangements.

Is there KYC in the UK?

KYC is mandatory in the UK, enforced by the Financial Conduct Authority under the Money Laundering Regulations 2017. Regulated firms must verify customer identities, conduct due diligence, and maintain ongoing monitoring — with enforcement fines reaching into the tens of millions for firms with inadequate controls.

What does KYC stand for?

KYC stands for Know Your Customer — a regulatory framework requiring businesses to verify customer identities, assess financial crime risk, and monitor activity to prevent money laundering, fraud, and terrorist financing. It applies to financial institutions, fintechs, crypto firms, and a range of other regulated entities.

What is the difference between KYC consulting and AML consulting?

KYC focuses specifically on customer identity verification and risk profiling. AML consulting covers the broader compliance program including transaction monitoring, suspicious activity reporting, and regulatory filings. In practice, KYC is a core component of any AML compliance program, and most consultants address both together.

How much does KYC consulting cost?

Costs vary based on engagement scope, consultant seniority, and jurisdictional complexity. Fractional compliance models typically cost 50–70% less than full-time executive hires and avoid recruitment costs, benefits, and long-term commitment. For startups and growth-stage fintechs, the fractional model is generally the most cost-effective path to director-level expertise.

Can a startup use a fractional compliance officer instead of hiring a full-time KYC compliance lead?

Many early-stage fintechs and crypto firms use fractional compliance officers to access director-level KYC expertise without the cost of a full-time hire. It's a practical fit for seed and Series A companies that need to satisfy sponsor bank or regulatory requirements before they're ready to justify a permanent CCO or BSA Officer.