Introduction

Financial services firms face a stark reality: regulatory audits are not optional disruptions but recurring tests that measure the strength of your compliance program under scrutiny. The cost of failing extends well beyond fines. TD Bank's record-breaking $1.3 billion FinCEN penalty in October 2024 for AML program failures shows how inadequate compliance infrastructure can escalate to existential threats — criminal liability, growth restrictions, and permanent reputational damage.

Fintech companies, crypto firms, and growth-stage banks face acute pressure. Unlike established institutions, they navigate BSA/AML, Reg E, UDAAP, GDPR, and evolving crypto regulations without mature compliance departments — and must meet the same examination standards as larger competitors.

Tighter budgets and faster growth cycles make that gap harder to close.

This guide addresses that gap directly, covering practical best practices across the full audit lifecycle: preparation before examinations begin, execution during fieldwork, and remediation after findings are issued. We'll also cover common pitfalls and the compliance leadership structures that consistently drive audit success.

TLDR:

- Regulatory audits test your entire compliance program; failure brings billion-dollar fines and growth restrictions

- Year-round readiness—not last-minute scrambling—separates firms that pass from those that don't

- Experienced compliance leadership (CCO, BSA Officer, MLRO) is non-negotiable for credible auditor engagement

- Post-audit remediation matters as much as the exam itself; regulators track whether you fix what they flag

- Fractional compliance models deliver director-level expertise at a fraction of the cost

What Is a Regulatory Audit?

A regulatory audit is a formal examination by an external regulatory body or authorized third party to assess whether your organization adheres to applicable laws, regulations, and internal policies. For financial services firms, these examinations cover critical areas including BSA/AML, consumer protection, data privacy, and financial reporting.

Regulators such as the OCC, FinCEN, FDIC, FCA, or state banking authorities verify that institutions maintain adequate controls, monitor transactions, and protect consumers. Outcomes can range from clean reports to matters requiring attention (MRAs), enforcement actions, or significant financial penalties.

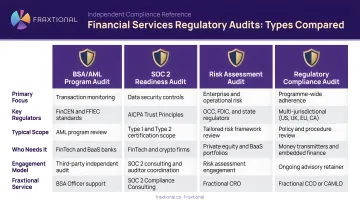

Types of Audits in Financial Services

Different examination types serve distinct purposes and occur on varying schedules:

| Audit Type | Who Conducts It | Typical Frequency | Key Requirement |

|---|---|---|---|

| Regulatory Examination | OCC, FDIC, FinCEN, FCA, state agencies | Every 12–18 months | Full-scope review of supervisory framework and risk management |

| Independent Third-Party Audit | External auditors or qualified independent parties | Annually (risk-based) | FFIEC-mandated BSA/AML testing; results reported to board |

| Internal Audit | In-house compliance team | Ongoing / quarterly | Self-assessment between exams; validates procedures match actual practices |

| Sponsor Bank Program Review | Sponsor bank oversight teams | Increasing in frequency | Third-party relationship compliance per 2023 Interagency Guidance |

Each type carries distinct stakes. Independent AML testing failures, for instance, carry direct enforcement risk: FinCEN's $3.5 million penalty against Paxful specifically cited years of inadequate independent testing as a primary violation.

Sponsor bank reviews deserve particular attention for BaaS and embedded finance companies. The 2023 Interagency Guidance makes clear that banks cannot outsource compliance liability to their fintech partners. FDIC consent orders against Lineage Bank and Thread Bank show that inadequate fintech oversight now triggers severe growth restrictions — for the bank and the fintech alike.

Before the Audit: Building Year-Round Compliance Readiness

Audit readiness begins long before an examiner sends a request letter. Organizations that build compliance into daily operations arrive at examinations with fewer findings, faster document turnaround, and more credibility with regulators.

Conduct Regular Internal Pre-Audit Reviews and Mock Examinations

Simulating an actual audit reveals gaps before regulators do. Effective mock examinations include document requests matching typical regulator inquiries, control walkthroughs testing whether procedures work as documented, and personnel interviews evaluating whether your team can articulate compliance responsibilities clearly.

Findings from your previous exam should serve as the starting checklist for every subsequent preparation cycle. Regulators track whether previously flagged items have been remediated. Recurring deficiencies signal to examiners that management either can't fix problems or won't.

Build a Centralized Compliance Documentation System

Auditors measure both the substance of controls and your organization's ability to produce evidence quickly. A centralized repository should contain:

- Current policies and procedures with version control

- Training records showing who was trained, when, and on what topics

- Risk assessments documenting how you identified and prioritized compliance risks

- Audit trails demonstrating how decisions were made and approved

- Corrective action logs tracking remediation of prior findings

The FFIEC BSA/AML Examination Manual requires that most BSA records, including SARs and CTRs, be maintained for at least five years from filing. Customer identification information must be retained for five years after account closure. Disorganized or incomplete records signal broader control failures to examiners.

Perform Ongoing Risk-Based Prioritization Aligned with Regulator Focus Areas

Current supervisory priorities should directly shape where your internal audit resources go. Key focus areas right now include:

- OCC (FY 2025): Third-party risks (especially bank-fintech arrangements), payment systems innovation, and BSA/AML compliance

- FinCEN: National AML/CFT priorities covering corruption, cybercrime, terrorist financing, fraud, and transnational criminal organizations

- ECB (2025–2027): Operational resilience — specifically IT outsourcing, security, and cyber risk under DORA

If third-party risk management is a supervisory priority and you operate a BaaS model, allocate more review time to vendor due diligence, contract compliance provisions, and partner monitoring documentation.

Designate a Cross-Functional Audit Response Team

Role clarity prevents bottlenecks during document production. Your audit response team should include:

- Compliance Lead: Coordinates the overall response, serves as primary auditor contact, and ensures consistency

- Legal: Reviews sensitive matters, advises on privileges, and interprets regulatory requirements

- Operations: Provides transaction data, process documentation, and operational context

- IT/Data: Extracts system records, validates data integrity, and explains technical controls

Assigning a single point of contact for auditor communication reduces confusion and prevents contradictory responses. This person should maintain a communication log documenting all examiner interactions.

Ensure Vendor and Third-Party Compliance Is Audit-Ready

Regulators increasingly scrutinize compliance programs of BaaS providers, payment processors, and other critical vendors. The Interagency Guidance requires rigorous due diligence, contractual right-to-audit provisions, ongoing monitoring, and documented termination strategies.

Your audit-ready vendor file should contain:

- Initial due diligence reports and risk assessments

- Contracts specifying compliance obligations and audit rights

- Ongoing monitoring documentation (SOC 2 reports, control attestations, periodic reviews)

- Evidence of vendor performance against compliance commitments

- Contingency plans for vendor failure or relationship termination

During the Audit: Best Practices for Execution

Maintain Professional, Transparent, and Proactive Communication

Examiners respond positively to organizations that demonstrate they understand what is being assessed and are prepared to engage substantively. Adversarial or evasive postures consistently produce worse outcomes.

Set the tone early with a comprehensive overview of your compliance program structure, key personnel, and recent enhancements. Proactively disclose known issues you're already remediating — rather than waiting for examiners to discover them. This signals self-awareness and accountability from the start.

Two actions that consistently improve examiner perception:

- Early transparency: Surfacing issues yourself before they're found shifts the dynamic from defensive to collaborative

- Program ownership: Demonstrating that leadership understands the compliance program's gaps and remediation status builds credibility fast

Respond to Document Requests Promptly, Accurately, and Completely

Provide exactly what is requested without over-producing (which raises new questions) or under-producing (which signals disorganization). Review every submission for accuracy before delivery.

Create a document request tracking log:

- Request number and date received

- Description of information requested

- Person responsible for compiling response

- Target completion date

- Actual submission date

- Review/approval documentation

A tracking log like this keeps every request accounted for and gives you a defensible record of your responsiveness if questions arise later.

Document All Examiner Interactions in Real Time

Maintain a running log during the audit that captures:

- Date, time, and participants in each meeting or call

- Topics discussed and questions raised

- Verbal responses provided by your team

- Follow-up items or additional requests

- Examiner feedback or preliminary observations

This log protects your organization legally, enables better follow-up, and creates a reference record for future audit cycles. If examiners later dispute what was discussed, contemporaneous documentation provides clarity.

Manage Internal Stakeholders and Subject Matter Experts

Prepare personnel for examiner interviews by:

- Providing talking points aligned with documented policies

- Setting clear expectations about interview scope and format

- Establishing escalation protocols for unexpected or sensitive questions

- Conducting mock interviews for employees unfamiliar with regulatory examinations

Instruct team members to answer questions directly and truthfully but to avoid speculation or offering opinions beyond their expertise. "I don't know, but I can find out" is always preferable to guessing.

Escalate Significant Findings Internally Immediately

Issues surfaced during fieldwork (control failures, policy gaps, data discrepancies) must reach senior management immediately — not be managed at the operational level. Auditors expect leadership engagement on material findings.

Create an escalation protocol specifying:

- What constitutes a "material" issue requiring immediate escalation

- Who must be notified (CEO, CFO, Board, external counsel)

- Timeline for notification

- Documentation requirements

When leadership responds visibly and quickly, it reinforces the message that your organization takes compliance seriously — which matters far more to examiners than a clean finding sheet.

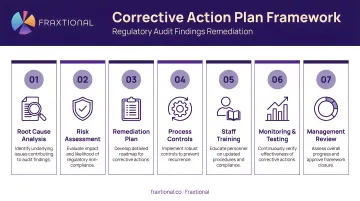

Post-Audit: Converting Findings Into Compliance Improvements

Thoroughly Analyze the Audit Report and Categorize Findings

Distinguish between:

- Material deficiencies: Require immediate remediation and pose significant risk

- Matters Requiring Attention (MRAs): Deficient practices that deviate from sound governance or result in noncompliance

- Observations: Areas for improvement that don't rise to formal enforcement level

Root cause analysis is more valuable than surface-level fixes. If examiners cite inadequate transaction monitoring, determine whether the root cause is insufficient staffing, outdated technology, inadequate training, or flawed policies. Addressing only the symptom ensures the problem recurs.

Build a Formal Corrective Action Plan with Named Owners and Realistic Deadlines

Regulators read a well-structured CAP as evidence that management understands the problem and has the discipline to fix it. Your plan should include:

- Specific finding reference from the examination report

- Root cause analysis summary

- Detailed remediation steps with assigned owners

- Realistic completion deadlines

- Success metrics demonstrating effectiveness

- Validation/testing procedures

- Board oversight and reporting mechanism

MRAs remain open until you implement an effective corrective action and examiners verify and validate its sustainability. Enter all findings into a tracking system with regular status updates, which examiners expect to see during follow-up reviews.

Use Audit Outcomes to Strengthen the Broader Compliance Program

Findings often point to systemic gaps in training, policy, process, or technology that will recur if not addressed at the program level. If multiple findings relate to vendor oversight, the issue likely isn't specific vendors but rather your entire third-party risk management framework.

Treat audits as a continuous improvement mechanism, not a pass/fail event. Each cycle should produce:

- Stronger policies and updated control documentation

- Targeted training that closes identified knowledge gaps

- Justified budget requests for compliance technology or staffing

- Board-level visibility into program maturity and open risks

Maintain the Regulator Relationship and Communicate Remediation Progress Proactively

Regulators view post-audit follow-through as a key indicator of management competence. Proactively sharing CAP milestones before the next exam builds credibility that translates into better CAMELS ratings and reduced scrutiny.

Establish a regular reporting cadence:

- Monthly internal status reviews for leadership

- Quarterly progress reports to your board

- Semi-annual updates to regulators documenting completed remediation

- Evidence packages (new policies, training records, control testing results) supporting closure requests

Waiting until the next exam to prove you fixed issues is a missed opportunity. Continuous, documented progress is what shifts examiner perception over time.

Common Regulatory Audit Pitfalls in Fintech and Financial Services

Failing to Learn from the Previous Examination

Organizations that don't systematically review prior findings as a baseline for the next audit cycle waste resources and damage credibility. Regulators track whether previously flagged items have been remediated—treating repeat findings as evidence of governance failure.

Create a "lessons learned" file after every examination that documents not just findings but also effective audit response practices, examiner preferences, and areas where your team struggled to produce documentation quickly.

Documentation and Policy Gaps That Expose Control Weaknesses

Regulators frequently cite the gap between what a firm does in practice and what its written policies reflect. Undocumented decisions, informal workarounds, and outdated procedures are recurring audit vulnerabilities at high-growth fintechs, where operational practice outpaces policy updates.

Two scenarios examiners cite repeatedly:

- Your transaction monitoring system has been enhanced, but your AML policy still describes the old process — that's a documentation gap, regardless of how well the system actually works

- Your team makes risk decisions in Slack, but those decisions never make it into case notes — without written records, you can't demonstrate control effectiveness

Underestimating the Scope of Third-Party and Sponsor Bank Oversight Reviews

Embedded finance and BaaS-model companies face heightened scrutiny of partner oversight programs. The FDIC's consent orders against Lineage Bank and Thread Bank in 2024 mandated severe growth restrictions—including prohibitions on new fintech partnerships—due to inadequate third-party risk management.

Your sponsor bank oversight file needs to show examiners a complete picture of how you manage partner risk. At minimum, it should demonstrate that you:

- Conducted due diligence before partner onboarding

- Negotiated contracts with clear compliance obligations and audit rights

- Monitor partner performance continuously through attestations, reports, and reviews

- Maintain documented contingency plans for partner failure or termination

- Escalate partner compliance issues to leadership and your board

The Role of Compliance Leadership in Audit Readiness

Audit readiness is inseparable from having experienced compliance leadership in place. A dedicated CCO, BSA Officer, or CAMLO who owns the program end-to-end and maintains regulator relationships differs sharply from the reactive posture of firms that scramble for compliance resources only after an audit is announced.

Leadership with direct regulatory experience understands how examiners think, what documentation they expect, and how to frame findings and remediation credibly. These leaders know which controls matter most, how to prioritize limited resources, and when issues require immediate board escalation versus operational resolution.

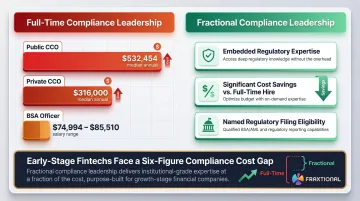

The Compliance Leadership Cost Challenge

Compliance leadership compensation has risen significantly. Public company Chief Compliance Officers earn a median total compensation of $532,454, while private company CCOs earn a median of $316,000. Even BSA Officers command average salaries ranging from $74,994 to $85,510.

Most early- and growth-stage fintech and crypto firms cannot justify or fund a full-time Chief Compliance Officer or BSA Officer—but still face the same regulatory examination standards as larger institutions. This creates a dangerous gap: startups need director-level compliance expertise but lack the budget or operational scale for permanent executive hiring.

Fractional Compliance Leadership as a Strategic Alternative

Fractional compliance leadership—such as a fractional CCO or fractional BSA Officer through a firm like Fraxtional—provides director-level regulatory expertise at a cost structure that fits a startup's growth stage.

These engagements deliver experienced compliance executives who can be officially named in regulatory filings, represent your company during examinations, and build audit-ready programs without the $300,000+ annual cost of a full-time executive hire.

Fractional leaders bring a specific advantage during audits: direct familiarity with how regulators think, what sponsor banks require, and how to present findings and remediation plans credibly. That perspective is hard to develop without sitting through many examinations across different regulatory environments.

For firms navigating US, UK, EU, and Canadian regulations simultaneously, experienced fractional leadership provides both compliance depth and geographic breadth—coverage that would otherwise require multiple full-time hires.

Frequently Asked Questions

What is a regulatory audit?

A regulatory audit is a formal review by a government regulator or authorized third party to assess an organization's adherence to applicable laws, rules, and standards. Outcomes can include findings, corrective action requirements, or enforcement actions.

What is legal regulatory compliance?

Legal regulatory compliance refers to an organization's ongoing obligation to meet all applicable laws, government regulations, and industry rules in its operating jurisdiction. In financial services, this spans areas like AML, consumer protection, data privacy, and licensing requirements.

What are the functions of regulatory compliance?

A compliance program covers several interconnected functions:

- Identifying applicable regulations and mapping them to business operations

- Implementing controls, policies, and procedures to meet those requirements

- Monitoring adherence and conducting internal audits

- Training staff and reporting findings to regulators and leadership

What does a regulatory compliance manager do?

A regulatory compliance manager oversees the design and execution of a firm's compliance program, manages regulatory relationships, leads audit preparation, and ensures that policies and controls reflect current regulatory requirements.

When should I hire a regulatory compliance consultant?

A regulatory compliance consultant makes sense when your firm needs specialized expertise for a specific project—such as audit preparation, a gap assessment, or a licensing application—without the overhead of a full-time hire. Fractional compliance officers fill a similar role on an ongoing basis, providing embedded leadership at a fraction of the cost.