The numbers reflect this shift. According to Thomson Reuters' 2023 Cost of Compliance report, 38% of compliance functions outsourced some or all functionality in 2023, up from 30% the year before — and that figure climbs to 75% among smaller financial institutions with $60B or less in assets. Outsourcing compliance is no longer an edge-case workaround. It's how a growing majority of regulated firms meet their obligations.

Still, many organizations underestimate what outsourcing actually delivers — and what goes wrong when it's handled poorly or deferred until a crisis forces the issue.

This article is a practical guide to the measurable benefits and honest considerations of compliance outsourcing, written for fintech, banking, and crypto companies weighing their options.

Key Takeaways

- Compliance outsourcing means delegating regulatory responsibilities — CCO, BSA Officer, MLRO, or CAMLO roles — to external specialists rather than making full-time hires

- Core benefits include cost efficiency, director-level expertise, global regulatory coverage, and faster audit readiness

- Key considerations include data security, vendor accountability, sector-specific experience, and clear internal ownership

- Outsourcing works best as an ongoing program with defined KPIs, not a reactive emergency measure

What Is Compliance Outsourcing?

Compliance outsourcing means engaging external professionals to manage regulatory obligations that would otherwise fall to internal staff. That can include AML program management, policy development, regulatory filings, risk assessments, SAR/CTR reporting, and senior compliance officer roles like CCO, BSA Officer, MLRO, or CAMLO.

Outsourcing is a delivery model — it determines how your compliance obligations get met, by whom, and at what cost. That distinction becomes concrete when regulators, auditors, or sponsor banks start evaluating your program.

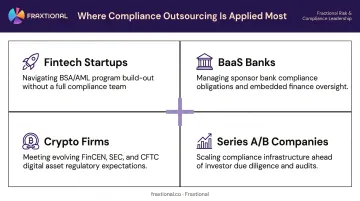

Where It's Most Commonly Applied

In financial services, compliance outsourcing shows up most frequently in these scenarios:

- Fintech startups without a dedicated compliance hire that need program infrastructure before their first sponsor bank conversation

- BaaS banks building or managing embedded finance programs with fintech partners

- Crypto firms navigating multi-jurisdiction licensing, FinCEN registration, and VASP regulations

- Series A/B companies preparing for sponsor bank relationships or investor due diligence

Each of these scenarios involves a different regulatory pressure point — but the same underlying question: who owns the compliance function, and are they qualified to defend it?

Key Benefits of Compliance Outsourcing

The advantages below are operational and financial — each maps to outcomes growth-stage companies track: cost per compliance function, time-to-audit-readiness, regulatory risk exposure, and leadership bandwidth.

Access to Director-Level Expertise Without Full-Time Commitment

Hiring a qualified Chief Compliance Officer or BSA Officer full-time is expensive. Robert Half's 2026 salary guide puts the CCO salary range at $171,750 to $233,000, and that's before benefits, recruiting costs, and onboarding time. Add the BLS-reported benefits overhead for senior finance and business roles — which averages $32.03/hour on top of wages — and the total cost of a full-time senior compliance hire climbs substantially.

Beyond cost, 61% of Thomson Reuters respondents expected senior compliance staff costs to rise, with 77% citing demand for skilled staff and specialist knowledge as the driver. Finding the right person takes time most growth-stage companies don't have.

Outsourcing solves both problems. An experienced compliance professional is embedded directly into company operations on a fractional or project basis, providing the same regulatory guidance, program oversight, and regulator-facing credibility as a full-time hire — without the full-time cost structure.

Fraxtional's director-led model illustrates how this works in practice. Every client receives direct oversight from an experienced compliance Director across BSA/AML, UDAAP, Reg E, privacy, and cyber risk. Directors can be named as CCO, BSA Officer, MLRO, or CAMLO on regulatory filings, contracts, and audits.

One client, a founder of a prepaid card fintech, put it plainly: "Fraxtional completely revamped our policies within weeks. Our sponsor bank approved them without a single revision."

This advantage matters most for: Seed through Series B companies that need a named compliance officer to satisfy regulatory requirements, investor expectations, or sponsor bank due diligence — but aren't yet at the scale to justify a full-time executive hire.

KPIs impacted: Compliance leadership cost, time-to-hire, sponsor bank approval timelines, examination outcomes.

Regulatory Agility Across Jurisdictions

Internal compliance teams typically specialize in one regulatory framework. That works until the business expands — or until the compliance landscape shifts faster than a single person can track.

Thomson Reuters monitored 61,228 regulatory events in 2023, averaging 234 daily alerts. Their survey found that **62% of compliance teams spent 1 to 7 hours per week just tracking and analyzing regulatory developments** — with G-SIB respondents spending considerably more time on this task.

Outsourced compliance providers operating across the US, UK, Canada, and EU bring current, applied knowledge of multiple frameworks simultaneously. Instead of your team chasing regulatory updates across FinCEN, FCA, FINTRAC, and MiCA independently, a provider monitors changes, assesses impact on your specific operations, and updates your program proactively.

Building that cross-jurisdictional pattern recognition in-house takes years — and constant maintenance. When a regulatory development in one market signals what's coming in another, an experienced provider advises ahead of enforcement, not in response to it.

Fraxtional's team maintains active expertise across:

- BSA/AML requirements and FinCEN obligations in the US

- MLRO requirements under UK and EU frameworks

- FINTRAC obligations in Canada

- VASP regulations for crypto and digital assets internationally

AML frameworks are aligned with FFIEC, FinCEN, and FATF standards, covering both domestic and cross-border operations.

This advantage matters most for: Companies expanding from one market to another, or those already operating across multiple licensing regimes — embedded finance platforms, crypto firms with global users, and cross-border payment providers.

KPIs impacted: Regulatory update response time, compliance gaps identified proactively vs. reactively, audit deficiency rates.

Cost Efficiency and Scalable Resource Allocation

Compliance demand isn't constant. Licensing applications, sponsor bank onboarding, M&A events, and regulatory examinations create temporary spikes that don't justify permanent headcount expansion — but do require senior-level attention.

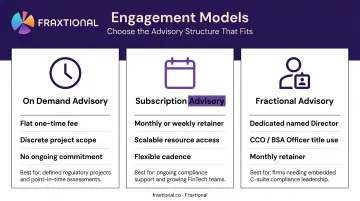

Outsourcing converts a fixed, high-overhead compliance function into flexible capacity. Engagement models can range from short-term advisory or gap assessments to long-term fractional leadership, allowing companies to match compliance spend to their actual regulatory obligations and growth stage.

Fraxtional's three engagement models reflect this directly:

- On Demand Advisory — flat one-time fee for discrete projects like audits, risk assessments, or sponsor bank introductions

- Subscription Advisory — monthly or weekly retainer for ongoing compliance support, with the ability to scale Director resources up or down

- Fractional Advisory — dedicated Director with named title use (CCO, BSA Officer, MLRO, CAMLO) on a monthly retainer, at a fraction of full-time executive cost

Fraxtional's fractional CRO/CCO services run 50–70% less than the cost of a full-time equivalent. A Series B fintech CEO who evaluated both options said: "After looking around at various options, including the hiring of a full-time BSA Officer, we were convinced that having a fractional resource provided us the most flexibility, but also the most expertise at the best price."

The savings extend beyond salary. Eliminated recruiting fees, no benefits overhead, no onboarding lag — and the ability to deploy the right level of expertise for each phase of the business, then scale back when the peak subsides.

This advantage matters most for: Series A and B companies managing rapid growth, organizations navigating a one-time licensing or sponsor bank event, or firms that have experienced a compliance officer departure and need program continuity without immediately committing to a permanent hire.

KPIs impacted: Compliance cost as a percentage of operating expenses, headcount vs. regulatory scope coverage, time-to-scale during growth events.

Key Considerations Before You Outsource Compliance

Outsourcing compliance delivers real advantages, but only when the engagement is structured correctly. Three areas require direct attention before you sign any agreement.

Vendor Accountability and Data Security

Compliance outsourcing involves sharing sensitive regulatory data, customer information, and internal policies with a third party. That creates significant exposure if the provider's data handling practices, security protocols, and contractual accountability haven't been reviewed.

Due diligence here should be treated with the same rigor you'd apply to any regulated vendor. At minimum, evaluate:

- Data handling and access control procedures

- Security certifications or frameworks the provider operates under

- Contractual terms covering confidentiality, liability, and breach notification

- Escalation paths if data handling issues arise during the engagement

Sector-Specific Experience Is Non-Negotiable

Compliance expertise in healthcare or insurance doesn't transfer to fintech, banking, or crypto. Each sector carries distinct regulatory frameworks, exam expectations, and sponsor bank dynamics that generalist consultants rarely understand at the required depth.

When evaluating a provider, ask specifically about:

- BSA/AML program builds and regulatory examination history

- Experience with sponsor bank relationships and fintech due diligence

- Familiarity with CAMLO requirements, VASP regulations, or whichever frameworks apply to your business

- Named compliance officer engagements and regulator-facing accountability

Internal Ownership Must Stay Clear

Outsourcing doesn't transfer your regulatory responsibility. OCC, Fed, and FDIC guidance is explicit: engaging a third party does not diminish a firm's obligation to operate safely and comply with applicable law. The FCA's SYSC 8 requirements make the same point for UK firms.

The most effective outsourcing arrangements define upfront who within the company owns the relationship, reviews deliverables, escalates issues, and interfaces with the external team. Without that internal accountability structure, outsourcing becomes a black box, and examiners will hold the firm — not the vendor — responsible when gaps surface.

What Happens When Compliance Outsourcing Is Delayed or Ignored

Some fintech and crypto companies defer compliance investment on the assumption they can "add it later." That assumption is expensive.

The enforcement record is clear. FinCEN's $3.4 billion consent order against Binance in 2023 cited willful BSA violations and an AML program that didn't exist for over a year after launch. BitMEX faced a $100 million penalty after six years of operating without a compliant AML program. FINTRAC imposed a CAD 6 million penalty on Binance in 2024 for failure to register and failure to report large virtual currency transactions.

These aren't edge cases. They're the predictable outcome of building volume before building compliance infrastructure.

Beyond enforcement risk, delayed compliance creates three immediate operational problems:

- Sponsor bank failures — without a named, credentialed compliance officer, companies often can't pass sponsor bank due diligence, stalling or ending the banking relationship entirely

- Investor friction — institutional investors conducting pre-deal diligence increasingly require demonstrated regulatory readiness; underdeveloped programs create deal risk

- Internal absorption costs — when a COO, CTO, or founding attorney absorbs compliance responsibilities, the fragmentation of attention produces errors, personal liability exposure, and costs that typically exceed what an outsourced engagement would have cost from the start

Each of these problems compounds the next. Reactive remediation — cleaning up after an enforcement inquiry, sponsor bank concern, or failed audit — costs more and takes longer than building proactively. Fraxtional works with companies in exactly these situations, and the pattern is consistent: firms that delayed pay more to fix it than they would have paid to prevent it.

How to Get the Most Value from Compliance Outsourcing

Treat It as an Ongoing Program

Compliance outsourcing works best when the provider is embedded consistently — attending internal meetings, reviewing operational changes, updating policies in real time, and participating in investor or regulator conversations as they arise. Bringing a provider in only for audits or annual reviews leaves the program reactive by design.

Fraxtional Directors work this way as standard practice — present on calls, across policy reviews, and available for sponsor bank or investor questions as they come up, not just at scheduled checkpoints.

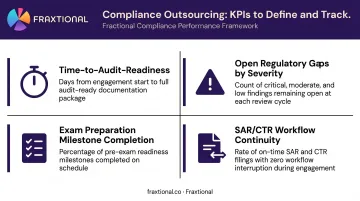

Define Outcomes and Review Them Regularly

Set clear KPIs at the start of every engagement. Useful starting points include:

- Time-to-audit-readiness for key compliance domains

- Number of open regulatory gaps, tracked by severity

- Exam preparation milestone completion

- SAR/CTR workflow continuity metrics

Review these on a regular cadence. Providers who report against defined metrics consistently perform better than those who report only on completed tasks.

Choose a Partner Whose Model Fits Your Stage

For fintech, banking, and crypto companies, the criteria that matter most are:

- Demonstrated experience across the specific regulatory frameworks and jurisdictions you operate in

- A director-led model where every engagement receives direct senior oversight, not hand-offs to junior staff

- Flexible terms that scale with your business rather than locking you into fixed commitments

Fraxtional's model is built around these criteria. The firm serves clients across the US, UK, Canada, and EU through CCO, BSA Officer, MLRO, and CAMLO engagements on flexible terms built for growth-stage companies in regulated financial services.

Conclusion

Compliance outsourcing is a strategic delivery model — not a shortcut. When structured correctly, it gives growth-stage companies access to senior expertise, cross-jurisdictional agility, and program continuity without the cost and commitment of a full-time executive hire.

Those benefits are cumulative. Companies that build a consistent, well-governed compliance program early are better positioned when it counts most — sponsor bank approvals, investor due diligence, regulatory examinations, and cross-border expansion. Waiting until scale to address compliance rarely saves money. It just moves the cost to a moment when the stakes are higher and the margin for error is smaller.

Frequently Asked Questions

What is outsourcing compliance?

Compliance outsourcing means delegating regulatory responsibilities — such as AML program management, risk assessments, policy development, or the CCO role itself — to external specialists rather than managing them entirely with internal staff. The company retains regulatory accountability; the provider delivers the expertise and execution.

Can you outsource a compliance officer?

Yes. A compliance officer role can be held on a fractional basis, where an experienced professional provides the oversight, program management, and regulatory accountability of a named CCO without being a full-time employee. Fraxtional Directors can be listed as named compliance leads on regulatory filings, contracts, and audits.

What are the main risks of outsourcing compliance?

The core risks are vendor data security exposure, unclear accountability between the external provider and internal team, and selecting a generalist provider without relevant sector experience. All three can be mitigated through thorough due diligence and well-structured engagement agreements.

How does compliance outsourcing work for fintech startups?

For fintech startups, compliance outsourcing typically means engaging a fractional compliance leader — CCO, BSA Officer, or MLRO — to build the program, support sponsor bank relationships, and prepare for regulatory exams. Engagement models are structured to fit early-stage budgets.

What is a fractional compliance officer?

A fractional compliance officer is an experienced professional who serves in an executive compliance role on a part-time or project basis. They provide the same regulatory oversight and named accountability as a full-time hire, at a lower cost, and can be embedded directly into the organization's leadership structure.

When does outsourcing make more sense than hiring in-house?

Outsourcing is typically the stronger choice in three situations:

- The regulatory scope is too specialized or cross-jurisdictional for a single in-house hire

- The company is pre-Series B and can't yet justify a full-time CCO salary

- Speed to regulatory readiness is critical and a lengthy hiring process isn't an option