Introduction

Financial services are no longer a bank-only business. Uber lets drivers cash out trip earnings instantly. Apple offers a credit card built directly into your iPhone. Chime runs checking accounts, debit cards, and early paycheck features without holding a single banking license. The infrastructure making all of this possible has a name: Banking as a Service, or BaaS.

BaaS is the model that lets non-bank companies offer regulated financial products by plugging into a licensed bank's infrastructure through APIs. No charter required. No years-long application process. Just a partnership, an API connection, and a compliance program built to survive examiner scrutiny.

This article covers what BaaS is, how the participant chain works, who benefits and how, and how it differs from embedded finance and open banking. It also addresses why compliance — not the API or the product — is what determines whether a BaaS arrangement holds together under regulatory pressure.

Key Takeaways

- BaaS lets non-bank businesses offer financial products by accessing a licensed bank's regulated infrastructure via APIs

- The global BaaS market is growing at ~17% annually and is projected to exceed $60B by the early 2030s

- Banks unlock new revenue streams, fintechs avoid building from scratch, and consumers get more financial choices

- BaaS is the back-end layer — embedded finance is the consumer-facing result

- Post-Synapse, strong compliance infrastructure is now a hard requirement for any BaaS partnership

What Is Banking as a Service (BaaS)?

BaaS is a model in which licensed banks open their regulated infrastructure — deposits, payments, card issuance, lending — to non-bank businesses through APIs. Those businesses can then offer financial products to their customers without obtaining a banking license themselves.

With traditional banking, customers go to the bank. BaaS inverts that relationship: the bank's capabilities travel to the customer through third-party platforms and apps they already use — without the end user ever touching a bank branch or application.

The Three Core Participants

Every BaaS arrangement involves at least three parties:

- The licensed bank — holds the charter, owns the regulatory obligations, provides the infrastructure

- The BaaS platform or middleware — often a fintech intermediary that packages and normalizes the bank's capabilities for easier integration

- The non-bank distributor — the company building the end-user product (the neobank, the ride-share app, the e-commerce platform)

The end user typically only ever sees the distributor's brand — the licensed bank operates entirely behind the scenes.

Market Context

According to Allied Market Research, the global BaaS market was valued at $12.2 billion in 2023 and is projected to reach $60 billion by 2032, growing at a 17% CAGR. Mordor Intelligence's projections use a different methodology but land in the same range — roughly $65.78 billion by 2031 at a 17.83% CAGR.

Research firms differ on the baseline, but the direction is the same. BaaS adoption is accelerating across retail, gig economy, and embedded finance — and with that growth comes a corresponding rise in regulatory scrutiny for every participant in the stack.

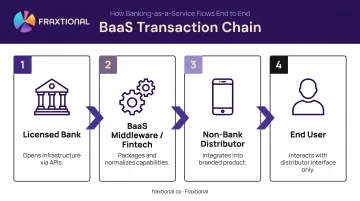

How BaaS Works: Technology, APIs, and the Participant Chain

APIs (Application Programming Interfaces) are the technical backbone of BaaS. The Bank for International Settlements defines them as rules and specifications that let software programs communicate with each other. In a BaaS context, that means a non-bank company can access specific banking functions on demand: payments processing, KYC verification, account management, card issuance.

The Transaction Flow

Here's how a BaaS arrangement actually works end-to-end:

- The licensed bank opens its infrastructure via APIs, defining what capabilities partners can access

- A fintech or BaaS middleware company connects to those APIs, packages the capabilities, and makes them easier to integrate

- The non-bank distributor integrates those packaged capabilities into its own product or app

- The end user interacts with the distributor's branded interface, never touching the bank directly

In white-label banking, the customer sees one brand — the regulated bank sits behind the scenes handling compliance, funds custody, and regulatory obligations.

Four Participant Configurations

In practice, participants play different roles depending on how deeply they're integrated:

| Configuration | Description |

|---|---|

| Provider | Bank offers license and infrastructure only |

| Provider-Aggregator | Bank bundles third-party vendor capabilities alongside its own |

| Distributor | Non-bank company uses BaaS to offer white-label financial products |

| Distributor-Aggregator | Non-bank company adds additional products on top of core BaaS |

Each configuration relies on the same underlying mechanics, though the technical tools vary. APIs enable two-way data and functionality exchange — used for interactive functions like account opening or KYC checks. Webhooks are lighter and one-directional, better suited for event-driven notifications like transaction alerts. Most BaaS arrangements use both.

Key Benefits of BaaS — For Banks, Fintechs, and Customers

For Banks

BaaS turns regulatory infrastructure from a sunk cost into a revenue-generating asset. Banks have already spent years and significant capital building the compliance frameworks, charter obligations, and risk management systems that regulators require. BaaS lets them monetize all of that through fee-based partnerships with non-bank distributors.

Two specific advantages follow:

- Revenue from existing infrastructure: Fee income from fintech partners, without building new products from scratch

- Broader distribution at lower cost: Products placed inside ride-share apps, e-commerce platforms, and consumer fintech tools — at a fraction of traditional customer acquisition costs

For Fintechs and Non-Bank Companies

Speed to market is the most immediate benefit. Obtaining a banking charter in the US is a multi-year commitment — the OCC targets a decision within 120 days, but capital must be raised within 12 months and the bank must open within 18 months of preliminary approval. In the UK, the Bank of England's mobilization period runs up to 12 months post-authorization.

A BaaS partnership sidesteps all of that.

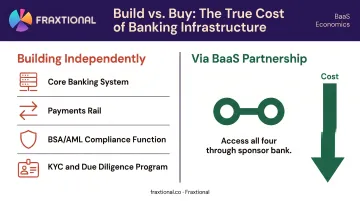

The cost case is just as compelling. Instead of independently building:

- A core banking system

- A payments rail

- A compliance and BSA/AML function

- A KYC and customer due diligence program

...fintechs can access all of it through a sponsor bank relationship, freeing budget for product development and customer experience.

For End Customers

Consider what a customer experiences when their payroll app offers an instant savings account, or their e-commerce platform extends a buy-now-pay-later option at checkout. That's BaaS at work — and it only exists because lower barriers to fintech entry brought more products into competition.

That competitive pressure historically drives better pricing, improved features, and more intuitive user experiences. BaaS enables that embedded convenience directly: customers can open accounts, access loans, or make payments inside apps they already use daily.

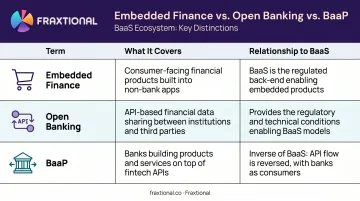

BaaS vs. Embedded Finance, Open Banking, and BaaP

These terms get used interchangeably, but they describe different things.

BaaS vs. Embedded Finance

BaaS is the infrastructure layer: the bank's APIs, regulated services, and compliance backbone. Embedded finance is what the consumer actually sees and uses: a loan offered at checkout, a savings account inside a payroll app. BaaS makes embedded finance possible. You can't have the consumer-facing product without the regulated back-end enabling it.

BaaS vs. Open Banking

Open banking governs the API-based sharing of financial data between institutions, often under consumer-permissioned frameworks. BaaS goes further: it shares both data and functional capabilities — the ability to open accounts, move money, and issue cards. Open banking often provides the regulatory foundation that makes BaaS arrangements possible.

BaaS vs. Banking as a Platform (BaaP)

BaaP is essentially the inverse of BaaS. In BaaP, a bank builds on top of third-party fintech APIs to expand its own product offerings. In BaaS, a non-bank builds on top of the bank's APIs. Both models rely on API-driven partnerships — they just point in opposite directions. That distinction matters for compliance: in BaaS, the sponsor bank retains regulatory accountability for the non-bank partner's activity, while in BaaP, the bank is the consumer of third-party services.

| Term | What It Covers | Relationship to BaaS |

|---|---|---|

| Embedded Finance | Consumer-facing financial products (loans, accounts, cards) built into non-bank apps | BaaS is the regulated back-end that makes it possible |

| Open Banking | API-based sharing of financial data under consumer-permissioned frameworks | Provides the regulatory conditions BaaS often operates within |

| BaaP | Banks building on top of third-party fintech APIs to expand their own offerings | The inverse of BaaS — API flow runs in the opposite direction |

Real-World BaaS Examples

Chime + The Bancorp Bank / Stride Bank

Chime is the most cited neobank BaaS example in the US. Chime holds no banking license — its SEC S-1/A filings confirm it is a financial technology company. The Bancorp Bank, N.A. and Stride Bank, N.A. (both FDIC-insured) provide the regulated backbone. Chime's relationship with Bancorp began in 2013; Stride Bank was added in 2019. Every checking account, debit card, and early paycheck feature runs through those partner banks.

Apple Card + Goldman Sachs

Apple Card launched in August 2019 through Goldman Sachs Bank USA. The customer experience is entirely Apple's — biometric approvals, Daily Cash rewards, spending summaries in the Wallet app. But Goldman Sachs Bank USA is the issuer, handles underwriting, manages the platform, and bears the regulatory compliance obligations. The cardholder agreement is formally between the customer and Goldman Sachs Bank USA, Salt Lake City Branch.

Uber + Green Dot / Branch + Evolve Bank & Trust

Uber has embedded two distinct financial products into its driver app through separate BaaS partnerships:

- Uber Checking by GoBank (March 2016): Powered by Green Dot, integrated directly into the Uber Driver app with instant trip earnings deposits

- Uber Pro Card: A Mastercard business debit card issued by Evolve Bank & Trust via Branch, with automatic cashout after trips and cash-back benefits

The Compliance Reality of BaaS Partnerships

Fintechs entering BaaS arrangements don't need a banking license — but they do need to be compliance-ready from day one.

Even though the licensed bank carries the regulatory charter, non-bank distributors in a BaaS arrangement are contractually and operationally expected to maintain their own KYC, AML transaction monitoring, and customer due diligence practices. Sponsor banks don't just want a distribution partner — they want a compliance partner.

The Post-Synapse Wake-Up Call

The collapse of Synapse Financial Technologies made this reality unavoidable. Synapse filed for Chapter 11 bankruptcy on April 22, 2024. The CFPB subsequently commenced an adversary proceeding, filing a complaint and proposed stipulated final judgment on August 21, 2025. The failure exposed serious reconciliation and consumer protection gaps across the BaaS middleware layer.

In direct response, the Federal Reserve, FDIC, and OCC issued a joint statement on July 25, 2024 on banks' arrangements with third parties to deliver deposit products and services. The guidance emphasizes governance, third-party monitoring, AML/CFT compliance, consumer protection, and operational risk — and it holds banks accountable for how they oversee their fintech partners.

The message to the market was clear: sloppy BaaS arrangements will attract regulatory action.

The Compliance Gap Fintechs Face

Most early-stage fintechs need a credible BSA Officer, a documented AML program, and a compliance framework that can survive a sponsor bank review. What they have is a product roadmap and a limited budget. Hiring a full-time Chief Compliance Officer is expensive and often impractical at seed or Series A stage.

Fractional compliance leadership fills that gap directly. Fraxtional works with both sides of the BaaS ecosystem: sponsor banks managing third-party fintech program risk, and fintech distributors building programs that satisfy bank onboarding requirements. Their fractional leaders serve as named BSA Officers, CCOs, CAMLOs, and MLROs — positions formally referenced in regulatory filings and partnership agreements.

The practical scope typically covers:

- BSA/AML program development and ongoing management

- Policy and procedure documentation tailored to sponsor bank expectations

- Third-party risk oversight frameworks

- UDAAP and Reg E compliance

- Ongoing audit readiness

One CEO summarized the dynamic plainly: "After looking around at various options, including hiring a full-time BSA Officer, we were convinced that having a fractional resource provided us the most flexibility, but also the most expertise at the best price. Fraxtional met that need, delivering a Director that supported us in discussions with a new sponsor bank and other key stakeholders."

For fintechs navigating their first sponsor bank relationship, that combination — named leadership, documented programs, and audit-ready practices — is often what moves a deal from stalled to signed.

Frequently Asked Questions

What is BaaS in banking?

BaaS (Banking as a Service) is a model where licensed banks open their infrastructure and services to non-bank businesses via APIs, allowing those businesses to offer financial products — accounts, payments, or loans — without obtaining a banking license. The bank holds the charter and regulatory obligations; the non-bank company owns the customer relationship.

What are examples of BaaS?

The most cited examples are Chime (backed by The Bancorp Bank and Stride Bank), Apple Card (issued by Goldman Sachs Bank USA), and Uber's driver financial tools (built through Green Dot and, more recently, Evolve Bank & Trust via Branch).

What is the difference between BaaS and embedded finance?

BaaS is the back-end infrastructure — the bank's APIs, regulated capabilities, and compliance obligations. Embedded finance is what the consumer sees: a payment option at checkout, a savings account inside an app. BaaS makes embedded finance possible; the two terms describe different layers of the same arrangement.

Who is responsible for compliance in a BaaS arrangement?

The licensed bank holds ultimate regulatory accountability, but non-bank partners are contractually required to maintain their own KYC, AML, and consumer protection practices. The 2024 joint guidance from the Fed, FDIC, and OCC confirmed that regulators hold both parties to high standards.

Is BaaS regulated?

BaaS arrangements operate within existing banking regulatory frameworks — FDIC, OCC, FCA, and others depending on jurisdiction. Following the Synapse collapse and the July 2024 joint agency statement, regulatory scrutiny of bank-fintech partnerships has increased considerably in the US, UK, and EU.