Introduction

The fintech regulatory environment heading into 2026 is unlike anything that came before it. DORA has been enforceable for EU entities since January 2025. MiCA's transitional arrangements for crypto-asset service providers run until July 1, 2026. The FCA Consumer Duty is fully bedded in across both open and closed product books. And CFPB's Section 1033 open banking rule (finalized in October 2024) is already under reconsideration, keeping US-focused teams in a state of ongoing uncertainty.

The consequences of getting this wrong are not abstract. According to Fenergo, global financial institution penalties reached $4.22 billion in H1 2025 alone — a 417% increase year over year — with North America accounting for 95% of that figure.

Beyond the fines, non-compliance creates compounding problems:

- Kills sponsor bank relationships, often permanently

- Stalls fundraising rounds at due diligence

- Erodes customer trust that takes years to rebuild

This article delivers a jurisdiction-aware compliance checklist for 2026 across four core pillars: regulatory licensing and registration, AML/KYC and financial crime prevention, data privacy and cybersecurity, and operational governance. Each section includes actionable steps fintech teams can act on immediately.

Key Takeaways

- Penalties are accelerating — $4.22B in H1 2025 alone, with transaction monitoring failures driving the largest share

- Four pillars matter most: licensing, AML/KYC, data privacy/cybersecurity, and operational governance

- Identify licensing obligations before you build — not after your first customer complaint

- AML programs must be risk-based and live, not static documents drafted at launch

- Fractional compliance roles (CCO, BSA Officer, MLRO, CAMLO) satisfy regulatory and sponsor bank requirements without a full-time hire

What Is a Fintech Compliance Checklist — And Why It Matters in 2026

A fintech compliance checklist is a structured framework mapping the regulatory, operational, technology, and reporting obligations a company must meet to operate legally. It functions as both a build guide for new companies and an audit tool for established ones.

What Makes 2026 Specifically Demanding

The regulatory calendar has compressed significantly. Here's what fintech teams must now plan around:

| Regulation | Jurisdiction | Status in 2026 |

|---|---|---|

| DORA | EU | Enforceable from January 17, 2025 — 20 entity types in scope |

| MiCA | EU | CASP transitional arrangements end July 1, 2026 |

| FCA Consumer Duty | UK | Fully in force for all product books since July 31, 2024 |

| CFPB Section 1033 | US | Finalized October 2024, under reconsideration since August 2025 |

| FINTRAC MSB updates | Canada | New agent eligibility verification requirement from October 1, 2025 |

Multiple US state privacy laws also activated in 2024 and 2025 — Colorado, Texas, and Oregon among them — with Indiana, Kentucky, and Rhode Island joining in January 2026.

Who This Checklist Applies To

These regulations apply across a wide range of company types. This framework is built for:

- Fintech startups (seed to Series B)

- Crypto and digital asset firms

- Embedded finance platforms

- Money transmitters

- BaaS-enabled products

...operating in any combination of the US, UK, EU, and Canada — whether you hold a direct license or rely on a sponsor bank's infrastructure. Operating under a sponsor bank does not shift compliance responsibility to the bank.

Licensing, Registration & Regulatory Compliance

Identify Your Regulatory Obligations First

Before building or expanding a product, map your regulatory footprint. The combination of business activity, target jurisdiction, and customer base determines your licensing obligations — and getting that mapping wrong is expensive.

Start with these questions:

- What activity does your product perform? Payments, lending, crypto, embedded finance, and investment products each trigger different frameworks

- Which jurisdictions are in scope? Your obligations change materially between US states, let alone between the US, UK, and EU

- Are you operating directly or via a sponsor bank? Both require compliance programs; only one requires you to hold the license

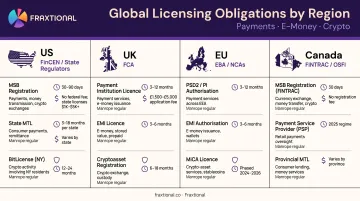

Key regulatory bodies by region:

- US: FinCEN (MSB registration), OCC (national bank charters), CFPB (consumer data rights), SEC/CFTC/FINRA depending on product type

- UK: FCA (payment services, e-money, cryptoasset registration)

- EU: National competent authorities under PSD2, MiCA, and DORA

- Canada: FINTRAC (MSB/VASP registration), provincial regulators

Obtain and Maintain the Right Licenses

Common registrations and licenses by activity type:

- US money transmission: FinCEN MSB registration (renewed every two years) plus state Money Transmitter Licenses — fees vary significantly by state (New York's MTL carries no application fee but requires a separate BitLicense for virtual currency; California's DFPI charges $5,000 non-refundable; Texas charges $10,000 non-refundable through NMLS)

- UK payments and e-money: FCA authorization or registration under the Payment Services Regulations 2017 and Electronic Money Regulations 2011

- EU payments and e-money: EBA PSD2 authorization and registration guidelines

- Crypto: FCA cryptoasset registration (UK), MiCA CASP authorization (EU), FINTRAC registration for virtual currency dealing (Canada)

Build license maintenance into operations from day one. Track renewal deadlines, periodic reporting obligations, and material change notifications. A lapsed or incorrect license can trigger federal criminal charges in the US and significant regulatory sanctions elsewhere.

Teams managing multi-state licensing often work with Fraxtional's Money Transmitter Licensing advisory service, which covers pre-filing strategy, application preparation, regulator communication, and ongoing renewal tracking across all US states and districts.

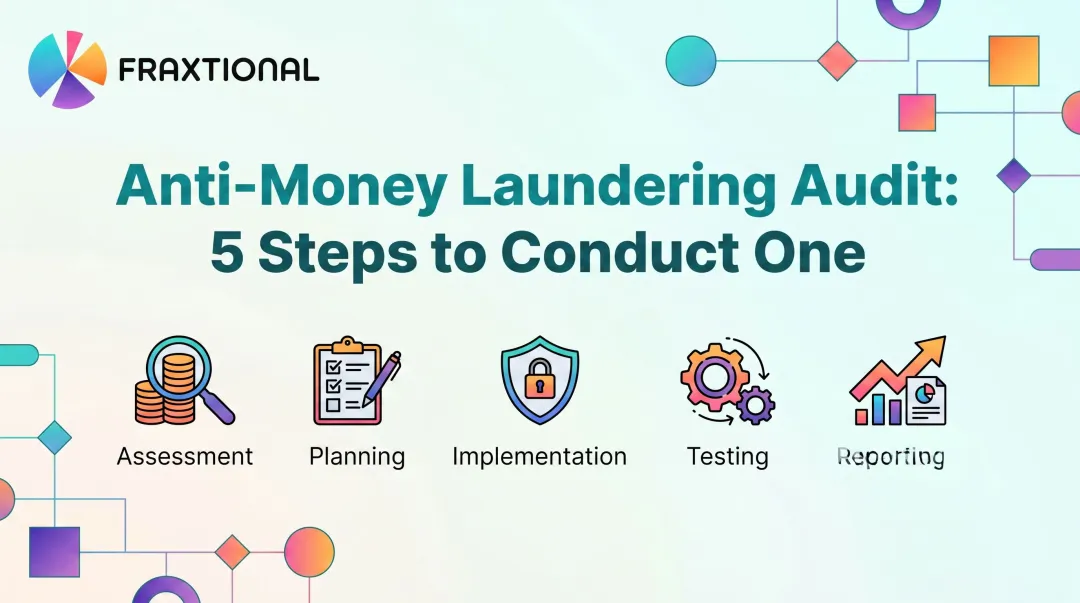

AML, KYC & Financial Crime Prevention

The numbers are stark: Fenergo reported $4.6 billion in global AML enforcement actions in 2024, with $3.3 billion directly linked to transaction monitoring failures. The gap is almost never in documentation. It's in controls.

Build a Risk-Based KYC Program

Customer Identification Program (CIP) — the baseline:

- Collect and verify name, date of birth, address, and government-issued ID for every customer at onboarding

- Screen against OFAC sanctions lists, PEP databases, and adverse media sources at onboarding and on an ongoing basis

Tiered due diligence — calibrate depth to risk:

- Standard CDD for lower-risk profiles

- Enhanced Due Diligence (EDD) for PEPs, high-transaction-volume accounts, and customers in high-risk geographies

- Document the rationale for every risk classification — this is what examiners and sponsor banks check first

Establish Transaction Monitoring and Reporting

A real-time transaction monitoring system is non-negotiable. Set threshold rules and behavioral analytics calibrated to your specific product's risk profile. A crypto exchange has a materially different pattern library than a payroll fintech.

SAR filing requirements by jurisdiction:

- US: File with FinCEN via the BSA E-Filing System within required timelines

- UK: Submit to the NCA — the UKFIU receives more than 850,000 SARs annually

- Canada: Report to FINTRAC — which received 631,137 Suspicious Transaction Reports in 2023-24 alone

Maintain detailed investigation records, findings, and response documentation for every report filed.

Designate qualified AML leadership. Regulators require a named BSA/AML Officer (US), MLRO (UK), or CAMLO (Canada) with real authority and resources — not a title on paper.

For early-stage fintechs not yet ready for a full-time hire, Fraxtional provides fractional BSA Officer, MLRO, and CAMLO services (including named title use in regulatory filings) that satisfy this requirement. These placements are accepted by sponsor banks across lending, crypto, and payments verticals.

Cash App: An $80M Enforcement Case State regulators issued an $80 million BSA/AML penalty against Block/Cash App on January 15, 2025, citing failures in customer due diligence, identity verification, suspicious activity reporting, and high-risk account controls. The CFPB separately ordered $175 million in consumer redress and penalties for fraud and dispute-handling failures. Neither action was an edge case. Both traced back to systematic program gaps.

Data Privacy, Cybersecurity & Technology Compliance

Map Your Data Privacy Obligations by Jurisdiction

Privacy obligations for fintechs are not uniform — and the number of active frameworks is growing. Map your exposure against each:

- US: GLBA Safeguards Rule (nine-element written information security program; breach notification for 500+ consumers effective May 2024), plus state laws: CCPA (California), TDPSA (Texas, effective July 2024), Oregon Consumer Privacy Act (effective July 2024), and Indiana, Kentucky, and Rhode Island laws (effective January 2026)

- UK: UK GDPR and the Data Protection Act 2018

- EU: GDPR — Article 33 requires supervisory authority notification within 72 hours of becoming aware of a personal data breach; EUR 1.25 billion in total DPA fines were issued in 2024

- Canada: PIPEDA (breach records kept for two years) and Quebec's Law 25 (privacy impact assessments, confidentiality incident notification, incident register)

Conduct a data mapping exercise documenting what personal and financial data is collected, how it is stored, who it is shared with, retention periods, and customer rights. Update the mapping at least annually — and immediately after any material change to your data flows or vendor relationships.

Implement Cybersecurity Controls

Start with these baseline technical controls:

- AES-256 encryption for data at rest; TLS 1.3 for data in transit

- Multi-factor authentication for all users and administrators

- Role-based access controls and network segmentation isolating critical financial systems

- Regular penetration testing and vulnerability assessments

- Documented Incident Response Plan — tested before an incident, not written during one

That foundation feeds directly into the regulatory requirements that apply based on where you operate.

DORA for EU-regulated fintechs: Enforceable since January 17, 2025, DORA requires covered entities to build an ICT risk management framework across five pillars:

- ICT risk management

- ICT-related incident reporting

- Digital operational resilience testing

- ICT third-party risk management

- Information sharing

If you operate in the EU or partner with EU-regulated banks, assess whether you fall within scope and run a gap analysis now. The transitional window has closed.

Payment processing: PCI DSS v4.0.1 is the active supported version following v4.0's retirement on December 31, 2024. Align your network architecture, cardholder data protection, vulnerability management, and security testing with v4.0.1 requirements.

For EU and UK payment services, PSD2 Strong Customer Authentication is mandatory. The FCA's SCA rules apply to online card and account payments — non-compliance exposes you to both regulatory action and increased fraud liability.

Operational Governance, Training & Vendor Management

Regulators and sponsor banks don't just want compliance policies on paper — they want evidence of who owns them, who enforces them, and who escalates when something goes wrong. Governance structure is what answers those questions.

Governance Structure

- Designate compliance leadership with real authority — not a title on an org chart but someone who reports findings to the board and has the standing to escalate concerns

- Document senior management oversight of the compliance program — regulators and sponsor banks want to see this in writing

- For resource-constrained fintechs, a fractional CCO model delivers director-level oversight, board-level reporting, and documented governance frameworks — a practical path when a full-time hire isn't yet feasible

Compliance Training

Training is evidence. Regulators and sponsor banks look for it:

- AML/KYC onboarding training within the first 10 days of employment

- Annual full-program refreshers for all staff

- Role-specific modules: marketing (advertising rules, UDAAP), customer-facing staff (complaint handling, Reg E), back-office teams (recordkeeping, SAR procedures)

- Attendance and quiz result records — these are your evidence of due diligence

Vendor and Third-Party Risk Management

The OCC/FDIC/Federal Reserve 2024 guidance confirms that banks are expected to conduct due diligence, contract negotiation, and ongoing monitoring for all third-party relationships — including fintech partnerships. Fintechs face the same scrutiny from their own vendors in reverse: your regulators and sponsor banks will ask how you manage the third parties you rely on.

For every vendor — BaaS providers, data processors, KYC/AML tech vendors, and payment processors — apply the same rigor:

- Conduct risk-based due diligence before onboarding

- Categorize vendors by risk level

- Include compliance obligations, audit rights, and incident notification requirements in every contract

- Monitor performance on a continuous basis — regulators treat static, point-in-time reviews as insufficient

Common Fintech Compliance Mistakes to Avoid in 2026

Three patterns surface repeatedly across enforcement actions and failed sponsor bank audits:

1. Treating compliance as a launch-day setup. Regulations change, products evolve, and regulators expect active programs with evidence of ongoing monitoring. Deloitte's research found 46% of early-stage fintechs up to Series B lack an internal audit function and only 34% have a dedicated board risk committee.

Static documentation from launch day will not survive a regulatory examination. Build in quarterly policy reviews and a process for tracking regulatory changes in every jurisdiction you operate.

2. Underestimating multi-jurisdictional complexity. Fintechs expanding across US states — or entering the UK or EU — discover that compliance frameworks don't transfer cleanly. Each jurisdiction has distinct requirements across:

- Licensing thresholds and registration triggers

- AML reporting obligations and SAR/CTR timelines

- Data privacy rights (CCPA, GDPR, PIPEDA)

- Consumer protection standards and disclosure rules

Conduct a full regulatory mapping exercise before entering any new market. Sigue Corporation's failure in March 2024 left thousands of California customers unable to access at least $2 million in money orders and remittances — a direct result of inadequate state-level compliance infrastructure.

3. Delaying compliance leadership until after a problem surfaces. The Block/Cash App penalties — $80 million for AML failures and $175 million for consumer protection failures, both announced in January 2025 — show how quickly costs escalate when problems compound. Waiting until a regulatory inquiry or failed sponsor bank audit to appoint qualified compliance leadership amplifies both the financial exposure and the reputational damage.

Fintechs that establish compliance leadership early enter investor due diligence, bank partnership reviews, and regulatory examinations from a position of demonstrated readiness — not remediation.

Frequently Asked Questions

What are the most important compliance requirements for fintech companies in 2026?

Four areas drive most enforcement actions: jurisdiction-specific licensing and registration; a risk-based AML/KYC program with transaction monitoring and SAR filing; data privacy and cybersecurity controls (GLBA, GDPR, UK GDPR, PIPEDA); and operational governance with a designated compliance officer and documented staff training. These requirements are interdependent — weak governance undermines everything else.

Do fintech startups need a full-time Chief Compliance Officer from day one?

A designated compliance leader is required by most regulators and sponsor banks, but it doesn't have to be a full-time hire from the start. Fractional CCO, BSA Officer, MLRO, and CAMLO arrangements are widely accepted and cost-effective. Fraxtional's compliance leaders carry named title use in regulatory filings and can scale up or down as your business grows.

What is the difference between AML and KYC in fintech compliance?

KYC (Know Your Customer) is the process of verifying customer identity and assessing risk at onboarding — it is one component of a broader program. AML (Anti-Money Laundering) encompasses KYC plus ongoing transaction monitoring, suspicious activity reporting, staff training, and risk assessments across the full customer lifecycle. Think of KYC as the front door; AML is the whole building.

How does DORA affect fintech companies operating in the EU in 2026?

DORA (enforceable from January 17, 2025) requires EU-regulated financial entities to implement an ICT risk management framework, resilience testing, and formal third-party ICT provider oversight across five defined pillars. If you operate in the EU or partner with EU-regulated banks, confirm your scope and run a gap analysis before your next audit cycle.

What are the penalties for fintech non-compliance?

Fines can be severe — Block/Cash App faced a combined $255 million in penalties in early 2025, and Binance settled with FinCEN for $3.4 billion in 2023. Non-financial consequences (license revocation, lost sponsor bank relationships, investor scrutiny) can be equally damaging for early-stage companies.

How can early-stage fintechs manage compliance without a large internal team?

Prioritize the obligations most critical to your model and jurisdiction — typically MSB registration, a written AML program, and a core data privacy policy. Use RegTech tools to automate monitoring and evidence collection. Fraxtional offers fractional CCO, BSA Officer, MLRO, and CAMLO engagements structured for seed-to-Series B companies that need senior expertise without a full-time hire.