Introduction

Financial crime doesn't announce itself. According to UNODC, between $800 billion and $2 trillion is laundered globally each year — roughly 2–5% of global GDP. Regulators in the US, UK, EU, and Canada have responded with aggressive, stepped-up enforcement, and the pressure on fintechs, banks, and crypto firms to get screening right has never been higher.

Yet many growing businesses still treat AML screening as a vague compliance obligation — something to set up at onboarding and revisit when an auditor asks. That gap is exactly what regulators and examiners are trained to find.

Getting screening wrong doesn't just invite fines — it can freeze banking relationships, trigger remediation orders, and become a deal-breaker during investor due diligence. This article breaks down what AML screening actually covers, why it extends well beyond onboarding, and where programs most commonly fail.

Key Takeaways

- AML screening checks customers, entities, and transactions against sanctions lists, PEP databases, watchlists, and adverse media sources

- Required by law under the BSA (US), POCA (UK), PCMLTFA (Canada), and EU AML Directives — covering banks, fintechs, MSBs, and crypto firms

- Core benefits: staying compliant, catching financial crime early, and protecting business relationships

- Skipping it exposes firms to regulatory fines, enforcement orders, reputational damage, and lost banking partnerships

- Screening is required at onboarding and on an ongoing basis, because customer risk profiles change over time

What Is AML Screening?

AML screening is the process of cross-checking customers, entities, and transactions against authoritative risk databases to identify potential involvement in:

- Money laundering and fraud

- Terrorism financing

- Sanctions violations and other financial crimes

It sits within a broader compliance lifecycle. Screening typically begins during customer onboarding as part of Customer Due Diligence (CDD) — but it doesn't stop there. Sanctions lists update without warning, PEP statuses change, and adverse media can surface months after a customer was first approved. Ongoing monitoring isn't optional; it's where most screening programs are weakest.

More than a compliance checkbox, AML screening is a risk intelligence function. It generates the information compliance teams need to make defensible decisions about who to onboard and which transactions to process — before a risk exposure becomes a regulatory or financial liability.

What Does AML Screening Include?

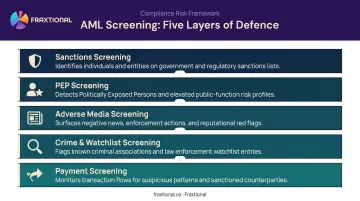

AML screening isn't one check. It's a layered process across five distinct data sources, each catching a different category of risk.

Sanctions Screening

Sanctions screening checks customers and entities against government-issued lists that prohibit financial dealings with designated individuals, organizations, or countries. Key sources include:

- OFAC SDN List (US)

- UK Sanctions List (UK — now the sole official source after the OFSI Consolidated List closed on 28 January 2026)

- EU Consolidated Financial Sanctions List

- UN Security Council Consolidated List

These lists update frequently and without advance notice. A firm that screens against a stale list, even inadvertently, has no defensible position when regulators come asking.

PEP Screening

Politically Exposed Persons (PEPs) are individuals holding or having held prominent public positions: government officials, senior executives of state-owned enterprises, and similar roles where bribery and corruption risk is structurally higher. FATF's guidance on Recommendations 12 and 22 requires firms to apply Enhanced Due Diligence (EDD) for any PEP relationship.

Critically, the risk perimeter extends to Relatives and Close Associates (RCAs), not just the named officeholder. UK Money Laundering Regulations 2017 (Regulation 35) and FCA Finalised Guidance FG25/3 both confirm this scope. PEP screening should trigger EDD review, not automatic rejection.

Adverse Media Screening

Adverse media screening checks customers against news articles, court filings, regulatory announcements, and online sources for red flags that don't yet appear on formal lists.

Its value is timing. A fraud investigation, a regulatory inquiry, or an association with criminal activity can surface in media weeks or months before any formal sanctions designation. The Wolfsberg Group and ACAMS both support negative news screening as a risk-based early warning control: a category of signal that structured databases simply can't replicate.

Crime and Watchlist Screening

This component checks individuals against databases of known or suspected financial criminals, money launderers, terrorists, and human traffickers, maintained by law enforcement bodies and international agencies. These databases update continuously, which makes checking them against a stale snapshot a meaningful compliance gap.

Payment Screening

The four checks above focus on who a customer is. Payment screening focuses on what they're doing. Rather than verifying identities at onboarding, it analyzes individual transactions in real time, checking sender and recipient details against sanctions and risk databases before funds move.

This matters most for cross-border payments and high-value transactions, where the window for inadvertent sanctions exposure is narrowest and the regulatory consequences are most immediate.

Why AML Screening Matters: Key Advantages

The value of AML screening goes well beyond avoiding fines. It directly shapes regulatory standing, financial exposure, and commercial viability — and those effects compound over time.

Advantage 1: Regulatory Compliance and Avoidance of Enforcement Action

AML screening is a legal obligation across every major jurisdiction where fintechs and financial services firms operate:

- US: Bank Secrecy Act and FinCEN requirements mandate risk-based controls, CDD, and suspicious activity reporting

- UK: POCA 2002, Money Laundering Regulations 2017, and FCA rules require proportionate policies, controls, and procedures

- EU: AMLD rules and the 2024 AML package require CDD, ongoing monitoring, EDD for high-risk cases

- Canada: PCMLTFA and FINTRAC guidance covers reporting entities from banks to casinos to crypto MSBs

Consistent, documented screening demonstrates to regulators that a functioning compliance program exists. It creates a defensible record that matters when a suspicious transaction is later investigated.

The financial stakes are concrete. In 2024, FinCEN assessed a record $1.3 billion penalty against TD Bank for willful BSA violations , the largest in US Treasury and FinCEN history. The same year, the FCA fined Starling Bank £28,959,426 specifically for financial sanctions screening failures. These aren't edge cases; they're the current enforcement baseline.

KPIs this affects:

- Number of regulatory findings per examination cycle

- Cost of compliance program vs. cost of penalties and remediation

- Audit resolution time

- Time-to-onboarding for low-risk customers

When it matters most: During rapid growth phases, new market entry, and sponsor bank applications — when regulators and banking partners scrutinize compliance programs most closely.

Advantage 2: Early Detection of Financial Crime Risk

AML screening acts as a pre-entry filter. Identifying high-risk individuals and entities before they enter the business is fundamentally cheaper (in time, legal exposure, and remediation) than detecting problems after a financial relationship is established.

A risk-based screening approach assigns risk scores based on sanctions hits, PEP status, adverse media, and geographic risk. This allows compliance teams to concentrate deeper investigation on genuinely high-risk cases, rather than treating every customer identically.

The operational scale is significant. The UK Financial Intelligence Unit received 866,616 SARs in 2024-25, with DAML requests denying £382.6 million to suspected criminals. That's the volume of financial crime detection that screening programs feed into — catching risk at onboarding is far more efficient than chasing it downstream.

Fraxtional's compliance directors have worked with clients where gaps in screening created exactly this remediation burden: back-testing customer portfolios, late SAR filings, and rebuilding regulator confidence , all significantly more costly than maintaining a consistent program from day one.

KPIs this affects:

- False positive rate and analyst investigation time

- SARs filed vs. risk-based expectations

- Percentage of high-risk customers identified at onboarding vs. post-onboarding

When it matters most: Fintechs with high-volume digital onboarding, crypto firms, cross-border payment companies, and any business operating in sectors or geographies where PEP and sanctions risk concentrations are higher.

Advantage 3: Protection of Business Reputation and Commercial Relationships

Being associated with financial crime, even unknowingly, creates lasting damage with regulators, sponsor banks, investors, and customers. AML screening provides the documented evidence that proper due diligence was conducted. Without that paper trail, a firm has no defense.

For fintechs and crypto firms specifically, sponsor bank relationships are often contingent on demonstrating a credible AML program. The Federal Reserve's 2024 enforcement action against Evolve Bank and Trust required improvements across BSA/AML, CDD, suspicious activity reporting, and OFAC compliance, directly impacting the fintech partners that relied on that relationship. AML screening quality is commercial infrastructure — sponsor bank access depends on it.

Investors see this clearly too. PE firms and acquirers conducting pre-deal due diligence examine AML screening maturity as a signal of operational readiness. A documented screening history with clear risk thresholds, calibrated parameters, and named director-level oversight supports valuation and reduces deal friction.

That's where fractional compliance leadership makes a concrete difference. One crypto lending platform came to Fraxtional after their sponsor bank required a named BSA Officer as a condition of the relationship. Fraxtional placed a fractional BSA Officer and restructured the AML framework.

The firm passed sponsor bank review ahead of schedule, turning a compliance gap into a commercial asset.

For early-stage fintechs and crypto firms without a full-time CCO or BSA Officer, Fraxtional's fractional BSA Officer and MLRO services provide named, director-level oversight, covering SAR filings, screening, sanctions controls, and regulator communications, without the cost of a full-time executive hire.

KPIs this affects:

- Time to secure sponsor bank partnership

- Investor due diligence outcomes

- Regulatory examination ratings

- Onboarding completion rates

When this is most critical: When raising capital, applying for a money transmitter license, entering a new regulated market, or seeking a BaaS or sponsor bank relationship.

What Happens When AML Screening Is Ignored

The consequences aren't theoretical — they're documented and they compound.

Regulatory consequences:

- Monetary penalties from FinCEN, FCA, FINTRAC, or equivalent regulators

- Enforcement orders and mandatory remediation programs

- Potential criminal referrals for senior officers in serious cases

NatWest was fined £264,772,619 in 2021 after convictions for three offences of failing to comply with money laundering regulations. TD Bank pleaded guilty to BSA and money laundering conspiracy violations in 2024. Both cases reflect where enforcement posture stands today.

Operational consequences:

- Onboarding sanctioned entities or money launderers creates direct legal liability

- Asset freezes and reputational damage that's difficult to reverse

- Loss of banking relationships that can effectively end a fintech's ability to operate

Screening gaps also compound over time. Back-testing entire customer portfolios, filing late SARs, and rebuilding regulator confidence costs far more than maintaining a consistent program from the start. Fraxtional has worked with clients where remediation costs ran several multiples of what a proper screening program would have required annually.

How to Get the Most Value from Your AML Screening Program

AML screening delivers real value only when it's applied consistently — not just at onboarding, but through ongoing monitoring that responds to list changes, PEP status shifts, and emerging adverse media.

The calibration challenge is real: over-screening buries analysts in false positives and creates compliance fatigue, while under-screening leaves gaps regulators will find. Effective programs define clear risk thresholds, tune screening parameters regularly, and document the rationale behind every significant decision.

Fraxtional's approach covers optimizing rule sets for transaction monitoring, implementing OFAC and PEP screening processes, and validating that filtering technology is actually working as designed.

A few principles that make the difference:

- Screen at onboarding and on an ongoing basis — sanctions lists and customer risk profiles both change

- Align rescreening frequency to your risk-based approach, not a fixed calendar

- Document threshold decisions; auditors and regulators want to see the reasoning, not just the outcome

- Treat adverse media as a complement to, not a substitute for, official list screening

For fintechs, crypto firms, and embedded finance companies scaling quickly without a full-time compliance team, Fraxtional's fractional BSA Officer and MLRO services offer a workable structure for managing this well. Each engagement provides named, director-level oversight of the AML screening program: screening parameter review, risk threshold sign-off, SAR governance, and regulator or sponsor bank interfacing.

Engagement models are flexible, scaling with transaction volume and risk appetite as the business grows — without the cost or commitment of a full-time hire.

AML screening isn't a one-time setup task. The programs that hold up under regulatory scrutiny — and actually catch risk — are the ones treated as living infrastructure, not a compliance checkbox.

Frequently Asked Questions

What does AML screening include?

AML screening typically covers five components: sanctions screening, PEP and RCA checks, adverse media screening, crime and watchlist screening, and (where relevant) payment screening. Each cross-references customer data against a different category of risk database, and together they form a layered financial crime detection system.

How much does AML screening cost in the UK?

Costs vary based on customer volume, product risk, geographic exposure, and whether a firm uses third-party platforms, in-house infrastructure, or fractional compliance oversight. UK Money Laundering Regulations 2017 (Regulation 19) require controls proportionate to the business — the FCA expects investment to scale with risk profile.

Who is required to perform AML screening?

Regulated entities include banks, fintechs, crypto firms and VASPs, money service businesses, insurers, real estate firms, casinos, and many professional service providers. Requirements vary by jurisdiction but are derived from FATF standards and implemented through local legislation across the US, UK, EU, and Canada.

What is the difference between AML screening and KYC?

KYC verifies who a customer is. AML screening takes that verified identity and checks it against risk databases (sanctions lists, PEP lists, adverse media, and watchlists) to assess financial crime risk. KYC is a prerequisite for AML screening, not a substitute for it.

How often should AML screening be conducted?

Screening should occur at onboarding and on a continuing basis thereafter. Sanctions lists update without warning, and a customer's risk profile can change materially after onboarding. Rescreening frequency should reflect the firm's risk-based approach and regulatory requirements, not a fixed annual schedule.

What happens if a business fails to conduct AML screening?

Consequences include regulatory fines, enforcement orders, mandatory remediation programs, reputational damage, and potential loss of banking relationships or operating licenses. Larger institutions typically face harsher penalties, but early-stage fintechs and crypto firms are not exempt, particularly when seeking sponsor bank partnerships or regulatory approvals.