The consequences are severe. Federal civil penalties accrue at $10,556 per day for each day of non-registration. Criminal exposure under 18 U.S.C. §1960 carries up to five years in prison per count. State regulators pursue enforcement years after unlicensed activity ends, often through coordinated multi-state actions. Founders and executives face personal criminal liability that survives corporate dissolution.

This article covers the full spectrum of penalties for operating without a money transmitter license: federal civil enforcement, federal criminal prosecution, state-level actions, personal liability for executives, and the hidden operational costs that never appear in enforcement orders but can destroy a business just as effectively.

Key Takeaways

- Operating without a money transmitter license is a federal felony under 18 U.S.C. §1960, punishable by up to five years in prison

- Federal civil penalties accrue at $10,556 per violation per day with no practical cap on total fines

- State regulators pursue enforcement years after unlicensed activity ends—silence from regulators is not approval

- Founders and executives face personal criminal liability; dissolving the company does not eliminate individual exposure

- Crypto, DeFi, and fintech startups fall under the same MTL requirements as traditional money transmitters—no exemptions for "innovation"

- Licensing costs thousands upfront; enforcement fines routinely reach millions—compliance is the cheaper path by far

What Is an Unlicensed Money Transmitter?

An unlicensed money transmitter is any business that accepts money or monetary value from one party to transmit to another—domestically or internationally—without obtaining the required federal registration and state-level money transmitter licenses.

"Unlicensed" covers three common scenarios:

- Starting operations without ever registering with FinCEN or applying for state licenses

- Assuming an exemption applies when your business model doesn't actually qualify

- Not recognizing that your product—crypto wallets, embedded payments, prepaid cards—triggers licensing requirements

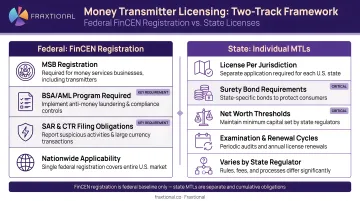

The Two-Track Licensing Framework

All money transmitters must satisfy two separate regulatory requirements:

| Requirement | Details |

|---|---|

| Federal MSB Registration (FinCEN) | Required within 180 days of beginning operations under the Bank Secrecy Act. Establishes your BSA/AML compliance obligations. |

| State Money Transmitter Licenses | Required in each state where customers are located. Nearly every U.S. state (except Montana) requires a separate license with independent fees and ongoing requirements. |

Critical distinction: FinCEN registration is not a license. It does not authorize money transmission and does not replace state licensing. Both are mandatory.

Common Business Models That Trigger Licensing

Regulators treat the following business models as money transmitters:

- Remittance services — domestic or international money transfers

- Crypto exchanges and wallets — platforms that accept and transmit convertible virtual currency

- P2P payment apps — consumer-to-consumer payment platforms

- Bill payment platforms — services that accept funds to pay third-party bills

- Currency exchangers — foreign exchange and crypto-to-fiat conversion

- Prepaid card issuers — stored-value card programs

- Marketplace facilitators — platforms that hold funds between buyers and sellers

- Payroll processors — services transmitting wages to employees

Operating offshore or using a foreign corporate structure does not eliminate U.S. licensing obligations if U.S. customers are involved. FinCEN regulations apply to any foreign-located person doing business "wholly or in substantial part within the United States." The $110 million penalty against BTC-e exchange confirms this extraterritorial reach is enforced.

Federal Penalties for Operating Without a License

Civil Penalties Under the Bank Secrecy Act

Under 31 U.S.C. §5330 and 31 CFR 1022.380, any person or entity that fails to comply with MSB registration requirements is liable for a civil monetary penalty. The statute explicitly states that "each day a violation continues constitutes a separate violation."

For penalties assessed on or after January 17, 2025, the inflation-adjusted maximum is $10,556 per day. A company operating unregistered for 12 months faces up to 365 separate violation counts — potentially exceeding $3.8 million in statutory penalties before any negotiation.

In December 2025, FinCEN assessed a $3.5 million civil penalty against Paxful, a peer-to-peer crypto exchange. The consent order noted Paxful operated as an unregistered MSB for 974 days, explicitly applying FinCEN's per-day penalty calculation authority.

Beyond fines, FinCEN may seek court orders halting all money transmission operations until compliance is achieved. The business can be forced to stop serving customers entirely while remediation is underway — not just fined.

Criminal Penalties Under 18 U.S.C. §1960

Operating an unlicensed money transmitting business is a federal felony under 18 U.S.C. §1960. Anyone who "knowingly conducts, controls, manages, supervises, directs, or owns" any part of an unlicensed money transmitting business can face:

- Up to five years in prison per count

- Criminal fines with no statutory maximum

- Asset forfeiture of property used in or derived from the unlicensed operation

Courts have interpreted the "knowingly" standard broadly. The statute requires only that the person knew they were operating the business — not that they knew a license was required. In United States v. Faiella (2014), the court rejected a Bitcoin exchanger's motion to dismiss, confirming ignorance of the law is not a defense.

The exposure compounds quickly. Under §1960(b)(1)(B), any money transmitting business affecting interstate or foreign commerce that fails to comply with FinCEN registration requirements is separately subject to criminal prosecution — meaning federal prosecutors can charge both the failure to register and the unlicensed operation statute simultaneously.

Major Federal Enforcement Actions

These three cases illustrate how civil penalties, criminal charges, and asset forfeiture operate together — not as separate tracks, but as simultaneous enforcement tools.

| Case | Civil Penalty | Criminal Outcome |

|---|---|---|

| BTC-e / Alexander Vinnik (2017) | $110M against BTC-e; $12M personal against Vinnik | Indicted under §1960; pleaded guilty to money laundering conspiracy in 2024 |

| Ripple Labs (2015) | $700,000 | Consent order; three-year look-back, independent auditors through 2020 |

| Larry Dean Harmon / Helix (2020) | $60M personal penalty | Pleaded guilty; 36 months in prison (2024); $400M+ asset forfeiture |

The Harmon case is worth noting in particular: the $60 million civil penalty, the prison sentence, and the $400 million forfeiture all stemmed from a single core failure — operating as an unregistered MSB. Each enforcement layer built on the last.

State-Level Enforcement and Penalties

Nearly every state requires a separate money transmitter license, and operating without one is a violation of state law from day one. Unlike federal enforcement, state licensing violations are state-specific offenses—a company serving customers in 20 states without licenses has potentially 20 separate enforcement exposures.

Criminal Classifications and Civil Penalties by State

Several states treat unlicensed money transmission as a state-level felony:

| State | Criminal Classification | Civil/Administrative Penalty |

|---|---|---|

| Florida | 3rd, 2nd, or 1st-degree felony (scales with transaction volume); fines up to $250,000 or twice the currency value | Up to $1,000 per day of unlicensed operation |

| New York | Class A misdemeanor; escalates to Class E felony if transaction volumes exceed $250,000/year | Forfeiture amounts determined by the superintendent |

| Texas | 3rd-degree felony | Up to $5,000 per violation, or $5,000 per day for continuing violations |

| California | N/A (civil enforcement) | Up to $1,000 per violation, or $1,000 per day for continuing violations |

| Washington | N/A (civil enforcement) | Up to $100 per violation per day |

State Enforcement Tools

State regulators deploy a range of enforcement mechanisms beyond fines:

- Cease-and-desist orders halt operations in that state immediately and become public records — damaging reputation with banking partners, investors, and other regulators.

- Forced wind-down requirements compel the company to transfer customer funds to a licensed entity and exit the market entirely.

- Future licensing bars allow some states to permanently disqualify companies from applying for licenses based on prior unlicensed activity.

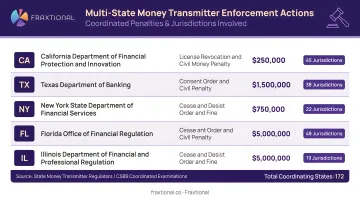

Multi-State Coordinated Enforcement

The Conference of State Bank Supervisors (CSBS) and the Nationwide Multistate Licensing System (NMLS) facilitate extensive information sharing among state regulators. When one state regulator identifies a licensing violation, it commonly shares information with peer regulators, triggering simultaneous enforcement actions in multiple jurisdictions.

Recent enforcement actions illustrate the scale of coordinated exposure:

- In 2025, state regulators from California, New York, Massachusetts, Minnesota, Nebraska, and Texas issued a joint $4.2 million consent order against Wise US, Inc. for AML deficiencies discovered during a multi-state examination.

- 48 state regulators levied an $80 million penalty against Block, Inc. (Cash App) for BSA/AML violations.

Initial discovery in one state rarely stays there.

Retroactive Enforcement

State regulators have pursued enforcement years after unlicensed activity ended. A company that operated without licenses, then voluntarily stopped or pivoted, remains exposed to penalty calculations covering the entire period of unlicensed operation.

Two cases demonstrate how far back regulators will reach:

- In 2020, Vermont fined Bitstamp $15,500 for operating without a license from 2012 to 2020, prior to the company transitioning customers to a licensed subsidiary.

- In 2011, New Hampshire fined Cambridge Mercantile for unlicensed activity conducted between 2006 and 2011.

No regulatory contact during that period did not protect either company. Regulators calculated penalties from the first day of unlicensed activity, not from the date of discovery.

Personal Liability: When Founders and Executives Face Charges

18 U.S.C. §1960 explicitly reaches individuals—not just corporate entities—who "conduct, control, manage, supervise, direct, or own" any part of an unlicensed money transmitting business. Founders, CEOs, compliance officers, and key executives can face personal criminal charges independent of whether the company itself is prosecuted.

Dissolving the Company Does Not Eliminate Personal Exposure

Federal prosecutors and state regulators can pursue charges against individuals even after the business ceases to exist. This exposure persists regardless of whether the company is still operating. Conviction or regulatory findings can result in:

- Industry bars permanently preventing individuals from working in financial services roles

- Personal fines and disgorgement reaching individuals directly

- Restitution orders requiring personal repayment to victims or the government

How Enforcement Has Played Out

Recent cases show that regulators and federal prosecutors have targeted executives at both traditional money services businesses and crypto platforms. The outcomes below span compliance failures, Bitcoin exchanges, and decentralized mixing services — but the legal exposure in each case was personal.

Thomas Haider (MoneyGram): FinCEN assessed a $1 million personal penalty against MoneyGram's former Chief Compliance Officer in 2014 for failing to terminate fraudulent agents and file SARs. In a 2017 settlement, Haider paid $250,000 and accepted a three-year injunction barring him from any compliance function at any money transmitter.

Anthony Murgio (Coin.mx): Murgio was sentenced to 66 months in prison in 2017 after pleading guilty to conspiring to operate an unlicensed money transmitting business via the Coin.mx Bitcoin exchange.

Roman Storm (Tornado Cash): In August 2025, co-founder Roman Storm was convicted by a jury for knowingly transmitting over $1 billion in criminal proceeds through the Tornado Cash mixer — even though the platform operated on a non-custodial, decentralized model.

Samourai Wallet founders (2025): The CEO and CTO of Samourai Wallet were sentenced to five and four years in prison, respectively, for operating an unlicensed money transmitting business via their non-custodial mixing service that transmitted over $237 million in criminal proceeds.

The Hidden Business Costs of Non-Compliance

Banking Relationship Risk

Banks, payment processors, and correspondent institutions conduct due diligence on their clients' licensing status. Discovery of unlicensed money transmission—whether through regulatory action or routine review—typically triggers immediate account termination.

Losing banking access mid-operation can freeze customer funds and halt the entire business, apart from any formal penalty. Sponsor banks reviewing embedded finance or BaaS partnerships specifically scrutinize compliance track records—and prior unlicensed activity is often disqualifying.

Investor and Acquirer Due Diligence Risk

Sophisticated investors, private equity firms, and strategic acquirers ask directly about licensing history and prior regulatory actions. Unlicensed operation creates a paper trail that can:

- Kill fundraising rounds before term sheets are signed

- Delay acquisitions by 6-12 months while remediation occurs

- Drive down valuations by 30-50% to account for regulatory liability

- Result in deal termination entirely if exposure is deemed too high

For seed-to-Series B companies that depend on the next funding round to survive, this is an existential threat.

The "Licensing After the Fact" Problem

Money transmitter license applications in every state ask whether the applicant has previously conducted money transmission without authorization. Answering yes—which is legally required—triggers:

- Elevated regulator scrutiny and longer review timelines

- Potential denial of the application based on prior unlicensed activity

- Conditions that make the license difficult to use (restricted transaction volumes, enhanced reporting, bond requirements)

In practice, companies that operated without a license often spend 12-18 months in remediation before a clean application is even possible.

How to Avoid These Penalties: Building a Compliant Foundation

Conduct a Licensing Footprint Assessment

Before operating, companies must map their customer locations, transaction flows, and business model against state-by-state money transmission statutes. Identify which states require an MTL based on where customers are located—not just where the business is incorporated.

Many companies end up needing licenses in 40+ jurisdictions. Licensing in one MTMA-adopting state does not automatically satisfy requirements in others.

Establish Required Compliance Infrastructure

A written AML program, designated BSA Officer, SAR filing capabilities, KYC/CIP controls, and ongoing transaction monitoring are prerequisites for obtaining and maintaining any money transmitter license. These are not optional enhancements. Their absence is itself an independent violation of BSA obligations.

Core components include:

- Board-approved AML policies tailored to your business model

- Risk-based compliance framework aligned with FFIEC, FinCEN, and FATF requirements

- KYC/CIP and OFAC/PEP screening controls

- Transaction monitoring systems customized to your risk profile

- SAR filing workflows with clear escalation paths

- Staff training and implementation support

Consider Proactive Remediation If Already Operating

If your company is already operating without licenses, voluntary disclosure, structured remediation, and proactive engagement with regulators consistently produce in better outcomes than waiting for an enforcement action. Consult qualified legal counsel before taking any remediation steps, as the approach varies significantly based on the duration, volume, and nature of unlicensed activity.

Access Fractional Compliance Leadership

Building the compliance infrastructure required for licensing does not require the cost of a full-time compliance executive. Fractional compliance leadership — including fractional CCOs, BSA Officers, and CAMLOs — gives growing fintech and money transmitter companies access to director-level expertise at a fraction of the cost, with the credibility that regulators and sponsor banks require.

Fraxtional uses this model to help companies from seed stage through Series B get compliance-ready before enforcement becomes a crisis. Fractional officers provide immediate ownership of daily AML/BSA obligations, respond to regulator or sponsor bank inquiries with confidence, and establish the governance framework that regulators expect from a mature compliance program.

Frequently Asked Questions

What is an unlicensed money transmitter?

An unlicensed money transmitter is any business that accepts money or monetary value from one party and transmits it to another—domestically or internationally—without obtaining the required FinCEN MSB registration and state money transmitter licenses. Many businesses unknowingly qualify, including crypto platforms, P2P apps, and embedded finance providers.

What are the penalties for non-compliance with FinCEN?

Civil penalties of up to $10,556 per violation per day for failure to register as an MSB, plus federal criminal liability under 18 U.S.C. §1960 with prison terms of up to five years. FinCEN can also pursue injunctive relief halting operations entirely.

Can founders be personally liable for operating without a money transmitter license?

Yes. 18 U.S.C. §1960 explicitly applies to individuals who control, manage, or direct an unlicensed money transmitting business. Founders and executives have been convicted and sentenced to prison—personal criminal exposure survives even if the company is dissolved.

Do crypto and fintech startups need a money transmitter license?

Most crypto exchanges, wallets, stablecoin operators, and fintech platforms that move funds on behalf of customers qualify as money transmitters. Courts have rejected every argument that digital assets or technological innovation creates an exemption from money transmission laws.

Does FinCEN MSB registration replace state money transmitter licenses?

No. FinCEN registration and state MTLs are separate and both required. Federal registration brings a company into the BSA/AML framework but does not authorize money transmission—each state where customers are located requires its own license.

What should I do if my company is already operating without a money transmitter license?

Immediately consult qualified legal counsel, pause unlicensed activity where feasible, and develop a remediation plan. Proactive outreach to regulators consistently produces better outcomes than waiting for enforcement to arrive. Fractional compliance advisors can help you assess exposure and manage the licensing process without the cost of a full-time hire.