This guide is written for fintech founders, compliance leads, and startup operators preparing to secure a sponsor bank partnership. The stakes are real: the bank's charter is on the line, and its review of fintech partners has become significantly more demanding in recent years. A failed or stalled due diligence process means no banking rails, no product launch, and no path forward.

What follows breaks down exactly what sponsor banks examine, how the process unfolds end-to-end, and what separates fintechs that pass from those that don't.

Key Takeaways

- Sponsor bank due diligence covers compliance programs, BSA/AML controls, leadership backgrounds, financial condition, and vendor relationships

- Expect five stages: document submission, bank review, clarifying requests, risk assessment, and a final decision

- Regulatory enforcement actions against BaaS banks in 2024 tightened onboarding requirements at most active sponsor banks

- The absence of a named compliance owner is the single most common reason fintechs fail or stall at this stage

- Fintechs that prepare before submission move faster and win better bank partners

What Is Sponsor Bank Due Diligence?

Sponsor bank due diligence is a multi-domain evaluation through which a bank determines whether a fintech is a safe, compliant, and financially viable partner — before extending access to its banking license, payment rails, and regulatory standing.

The bank's goal is straightforward: reasonable confidence that the fintech's operations, customers, and compliance posture will not expose the bank to regulatory, financial, or reputational harm. That's a high bar, and it shapes every document request and follow-up question.

Sponsor bank due diligence is the bank's review of the fintech as a business partner — distinct from customer due diligence (CDD), which is the fintech's obligation to verify and monitor its own end-users. The two are connected, though: banks now evaluate how fintechs conduct CDD on their customers as part of the broader assessment.

A fintech with a KYC vendor but no documented CDD framework will face questions.

Why the Due Diligence Bar Has Risen

The shift in scrutiny is directly tied to regulatory enforcement. Following a wave of BaaS-related consent orders and enforcement actions (concentrated heavily in 2024), regulators made clear that sponsor banks are fully accountable for the compliance failures of their fintech partners.

The scale of enforcement is hard to overstate. American Banker reported that in 2024, U.S. banking regulators issued more than 120 enforcement actions, fines, and lawsuits, with the OCC executing 36 formal enforcement actions — more than triple its 2023 total. BaaS violations were identified as a major enforcement theme throughout the year.

High-profile examples include:

- Evolve Bank & Trust — subject to a Federal Reserve cease and desist order in June 2024 for AML deficiencies and inadequate oversight of its fintech partner program

- Blue Ridge Bank — required by the OCC to obtain regulatory non-objection before onboarding any new fintech partners; subsequently began offboarding at least a dozen existing fintech relationships

- Thread Bank — subject to an FDIC consent order explicitly referencing its fintech partners and requiring stronger oversight

The June 2023 interagency guidance from the OCC, FDIC, and Federal Reserve codified what regulators now expect banks to demonstrate: documented oversight of fintech partners' BSA/AML programs, fraud controls, KYC procedures, and customer risk ratings. Banks can no longer rely on partner representations. That evidence must come directly from fintechs, gathered before the relationship begins.

For fintechs, the downstream effect is direct: banks that previously ran lighter diligence processes now request extensive documentation, background checks, compliance policy reviews, and proof of ongoing monitoring capability. What banks want to see upfront — and what many fintechs aren't ready to produce — is the focus of the rest of this guide.

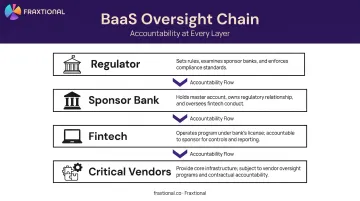

What Sponsor Banks Actually Evaluate

Due diligence spans five core domains. Banks assess all five before making a partnership decision.

Business and Corporate Structure

Banks start by verifying the fintech exists, is properly organized, and is owned by people without disqualifying backgrounds.

Key items requested include:

- Articles of incorporation, EIN, and certificate of good standing

- Organizational chart and board composition

- Ultimate Beneficial Owner (UBO) identification and documentation — grounded in FinCEN's CDD Final Rule

- Background checks on founders and key executives covering criminal history, adverse financial history, and regulatory sanctions

An adverse finding on a founder — prior enforcement action, fraud history, undisclosed litigation — can result in outright rejection regardless of how strong the compliance program looks on paper.

Compliance and BSA/AML Program

This is the most scrutinized domain, and the one where most fintechs fail.

Banks want to see:

- A written BSA/AML compliance program with a named compliance owner (BSA Officer or CCO)

- Documented KYC/CDD procedures and customer risk rating methodology

- Transaction monitoring processes and alert disposition workflows

- SAR and CTR filing framework with clear escalation paths

The named compliance owner requirement is non-negotiable. Banks need a human accountable for compliance decisions — someone they can contact directly, who signs off on filings and can speak to the program during bank oversight reviews. Fintechs without that person named frequently stall or fail at this stage.

Fractional arrangements work here. Fraxtional places fractional BSA Officers and CCOs who can be named in a fintech's program documentation, with AML frameworks that banks have accepted across lending, payments, and crypto programs.

Financial Condition and Business Plan

Banks are evaluating two things financially: stability and coherence.

They review:

- Current funding status, runway, and capitalization table

- Financial projections covering user acquisition and revenue

- Existing bank statements

The central question is whether the fintech is financially stable enough to sustain its program and whether projected transaction volumes align with its stated compliance capacity. A fintech projecting 50,000 monthly active users but lacking the compliance infrastructure to support that volume is flagged as a mismatch.

Technology, Security, and Vendor Risk

Banks assess the fintech's technology stack, data security posture (SOC 2 or equivalent certifications), and disaster recovery capabilities. They also require visibility into the fintech's own vendor relationships.

This matters because regulators now expect banks to understand not just the fintech they sponsor, but also the fintech's critical vendors. A payment infrastructure provider or identity verification vendor failure creates direct risk for the bank. Fintechs that can't produce a third-party risk management (TPRM) inventory — including documented vendor assessments — get flagged during review.

Legal, Regulatory, and Product Disclosures

Banks review which licenses the fintech holds or relies on, which states or jurisdictions it operates in, and whether product disclosures are accurate. One area banks scrutinize closely: FDIC insurance representations.

The FDIC's advisory on deposit insurance representations makes clear that banks must monitor third-party statements that could create consumer confusion about FDIC coverage. The FDIC and CFPB have issued multiple enforcement actions and cease-and-desist letters to fintechs and crypto companies that misrepresented deposit insurance status. Banks review fintech marketing materials and disclosures as part of due diligence — and a fintech implying FDIC protection where it doesn't apply is a significant red flag.

How the Process Works, Step by Step

Due diligence is iterative, not a one-time submission event. The timeline varies from a few weeks for well-prepared fintechs with straightforward models to several months for those with complex products or documentation gaps.

Step 1 — Internal Readiness Assessment

Before approaching any bank, conduct an honest internal review. Map your compliance program against what banks will request, then identify gaps: missing BSA/AML policy, no formal TPRM inventory, no named compliance owner. Resolve those gaps before submitting anything.

This is where most failures are seeded. Fintechs that skip this step face extended timelines or outright rejection.

Fraxtional's risk assessment service is specifically scoped to this preparation phase, producing prioritized findings, compliance-ready documentation, and a leadership-ready summary before the bank ever sees your file.

Step 2 — Initial Submission

The initial submission typically includes:

- Company profile (business description, website, business plan, tax ID)

- Team information (management bios, org chart, board composition)

- Financial documents (funding details, projections, bank statements)

- Legal and compliance questionnaire

Completeness matters. Incomplete or inconsistent submissions signal organizational immaturity. Some banks use structured intake platforms; others work via email or shared folders. Either way, a polished submission that requires minimal follow-up creates a materially better first impression.

Step 3 — Bank Review and Background Checks

The bank's compliance team reviews submitted materials, runs background checks on founders and key personnel, and screens against OFAC and sanctions lists.

This phase typically generates a round of follow-up questions: requests for additional policy documentation, clarification on the business model, or evidence of how the fintech handles specific compliance scenarios.

Step 4 — Risk Assessment and Program Scoping

If the initial review is favorable, the bank conducts a program-level risk assessment. This covers projected transaction volumes, customer risk profile, and the bank's own capacity to provide oversight.

The outcome of this stage determines whether the program fits the bank's risk appetite and what ongoing monitoring obligations it will impose.

Step 5 — Decision, Agreement, and Monitoring Setup

The bank issues one of three outcomes:

- Approval — proceed to contract negotiation

- Conditional approval — remediation required before moving forward

- Rejection — program does not fit the bank's current risk appetite

If approved, the parties negotiate and execute a sponsor bank agreement covering compliance obligations, liability, permitted products, and termination rights. Approval also triggers setup of ongoing monitoring: regular document refresh cycles and recurring compliance reviews throughout the partnership.

What Determines Whether a Fintech Passes

Four factors carry the most weight in a bank's evaluation:

- Compliance program ownership — The single most influential factor. Banks are skeptical of fintechs that have written policies but no named owner. A dedicated BSA Officer or CCO, even in a fractional capacity, signals the accountability structure banks need. Without it, approval is unlikely.

- Business model clarity — Banks assess whether the target customer segment, revenue model, and transaction types are clearly articulated and whether the risk profile is one they're equipped to manage. A mismatch between the stated model and the actual product is an immediate red flag.

- Financial runway — Limited runway creates operational risk. If the fintech fails mid-program, the bank inherits compliance and customer liability. Banks favor applicants that can demonstrate sufficient capitalization relative to projected scale.

- Leadership background — Prior enforcement actions, regulatory sanctions, fraud history, or undisclosed litigation involving founders or key executives can result in rejection regardless of how strong the compliance program is.

Common Mistakes Fintechs Make

Submitting generic compliance policies. Banks view boilerplate or clearly templated compliance documentation as evidence that the fintech hasn't meaningfully implemented what it's describing. Policies need to reflect the actual business model — the customer types, transaction flows, and specific risk scenarios the fintech will encounter.

Conflating a KYC vendor with a compliance program. Having an identity verification tool is not the same as having a compliance program. Banks evaluate the entire framework: who owns it, how it is governed, how it adapts to new risk. Technology is one input; the program around it is what's being assessed.

Missing vendor risk documentation. Fintechs frequently arrive without documented third-party vendor relationships or vendor risk assessments. Regulators now expect banks to understand not just the fintech, but its critical vendors too. Showing up without a TPRM inventory gives reviewers an easy reason to stall or deprioritize the application.

Frequently Asked Questions

How does a sponsor bank work?

A sponsor bank is a chartered bank that gives fintechs access to banking rails, regulatory licensing, and payment network membership (such as Visa or Mastercard). Because the bank retains ultimate compliance responsibility under its charter, its due diligence process is rigorous.

What is a sponsor bank agreement?

A sponsor bank agreement is the formal contract governing the bank-fintech partnership. It covers compliance obligations, liability allocation, permitted products, reserve requirements, exclusivity, and termination rights — and is negotiated after the bank approves the fintech's application.

What are the three components of customer due diligence (CDD)?

The three standard components are: customer identification and verification (KYC), understanding the nature and purpose of the customer relationship, and ongoing monitoring of transactions for suspicious activity. Sponsor banks evaluate whether fintechs have robust CDD programs in place for their own end-users.

How long does sponsor bank due diligence take?

Timelines range from a few weeks for well-prepared fintechs with straightforward models to several months for those with complex products or documentation gaps. How prepared you are before submission drives the timeline more than any other factor.

What documents do fintechs typically need?

Core document categories include:

- Corporate formation documents and UBO identification

- BSA/AML compliance program and KYC/CDD policies

- Financial statements and projections

- Technology security documentation

- Background check authorizations for key personnel

- TPRM inventory of critical vendors

What are the most common reasons fintechs fail due diligence?

The top failure drivers: no named compliance owner, incomplete or generic compliance policies, adverse findings on leadership background checks, a business model outside the bank's risk appetite, and insufficient financial runway relative to projected scale.