Introduction

Having a transaction monitoring system isn't enough if nobody has checked whether it actually works. Regulators have moved well past accepting "we have a model" as a compliance answer — they want documented evidence that the model was independently reviewed, is producing accurate outputs, and has been maintained as the institution's risk profile evolved.

The consequences of skipping that step are concrete. In 2022, USAA received a $140 million FinCEN penalty partly because 40% of its active monitoring scenarios hadn't been tuned in over two years and its customer risk score model was cited as critically flawed.

Transactions were passing through unchecked. The model had been broken for years without anyone catching it.

This article covers what qualifies as an AML model under federal guidance, why validation scrutiny has intensified, the four components regulators expect every validation to address, practical best practices, and how to set a defensible validation schedule.

Key Takeaways

- An AML model is any system using quantitative logic (scoring, segmentation, thresholds) to generate risk estimates — simple rule-based tools may not qualify

- Validation must be independent and triggered by go-live, material changes, and risk profile shifts — not just on a fixed schedule

- Four components: data integrity, scenario logic, output quality, and governance documentation

- USAA ($140M), U.S. Bank ($185M), and TD Bank ($1.3B) all received enforcement actions with model validation failures cited

- Tuning adjusts parameters; validation independently confirms the model works — and regulators expect both

What Is an AML Model — and When Does It Require Validation?

The Regulatory Definition

The Federal Reserve's SR 11-7 model risk guidance defines a model as "a quantitative method, system, or approach that applies statistical, economic, financial, or mathematical theories, techniques, and assumptions to process input data into quantitative estimates." Every model has three components: an information input component, a processing component, and a reporting component.

For AML purposes, this definition captures:

- Transaction monitoring systems with scenario-based rules and alert scoring

- Customer risk rating models that assign scores based on attributes

- Segmentation models that group customers for threshold calibration

Model vs. Tool: Why the Distinction Matters

Not every AML system is a model. Under the 2021 Interagency Statement on Model Risk Management for BSA/AML Systems, whether a system qualifies as a model is institution-specific. Systems typically not classified as models include CTR aggregation systems and stand-alone tools that flag transactions on a single factor.

The practical test: does the system apply quantitative logic — segmentation, weighted scoring, threshold optimization — to produce risk estimates? If yes, it's likely a model with validation obligations. If it's reorganizing or displaying data without generating estimates, it may be a tool.

Model classification is the threshold decision — it determines whether full independent validation is required or whether simpler periodic testing suffices.

When Validation Is Triggered

Validation isn't a one-time event at go-live. Once a system is classified as a model, SR 11-7 and the 2021 interagency BSA/AML statement require or warrant validation when:

- A model is first implemented

- A material change is made to the model or its parameters

- The institution's risk profile shifts — new products, new customer segments, new geographies

- A merger or acquisition occurs

- Regulatory findings cite model-related deficiencies

Why Regulators Are Scrutinizing AML Model Validation More Than Ever

The Regulatory Framework

SR 11-7 (Federal Reserve) established the foundational model risk management framework, later supplemented by the April 2021 interagency BSA/AML model risk statement that applies it specifically to transaction monitoring and customer risk rating systems.

As of April 2026, the Federal Reserve issued SR 26-2 and the OCC issued Bulletin 2026-13, revising and superseding the earlier guidance for their respective supervised institutions. The core validation expectations have only grown stricter.

What Enforcement Actions Actually Looked Like

Three cases make the stakes concrete:

| Institution | Penalty | Model Validation Issue |

|---|---|---|

| U.S. Bank (FinCEN, 2018) | $185M | Capped automated monitoring alerts; failed to have its transaction monitoring system validated by a suitably independent individual; customer risk-rating program failed to review relationships enterprise-wide |

| USAA Federal Savings Bank (FinCEN, 2022) | $140M | Lacked distinct policies for validation and adjustment of its monitoring system; 40% of active scenarios untuned for 2+ years; customer risk score model cited as critically flawed |

| TD Bank (OCC/FinCEN, 2024) | $1.3B + $450M | "Significant, long-standing, systemic breakdowns" in transaction monitoring; OCC consent order requires ongoing independent validation of models, rules, thresholds, and customer risk rating models |

Fintechs, BaaS Banks, and Crypto Firms Face Specific Exposure

These penalties hit traditional banks, but the same validation failures are now surfacing across fintechs, BaaS banks, and crypto firms — often with less infrastructure to absorb the fallout.

Institutions that scale quickly on third-party vendor models face a distinct risk. The 2021 interagency statement is explicit: banks remain ultimately responsible for BSA/AML compliance even when using third-party models. Deploying a vendor's transaction monitoring system without independent validation is treated as a compliance gap, not a vendor's problem.

Blue Ridge Bank is the clearest BaaS example. The OCC required independent model validation of its automated suspicious activity monitoring system following issues tied to fintech partner activity, then restricted new fintech relationships pending OCC approval.

Regulators consistently cite the same recurring deficiencies across institutions:

- Incomplete or outdated model documentation

- Incorrect transaction code mapping

- Inconsistent scenario testing and monitoring

- Failure to maintain a qualified BSA Officer with model governance oversight

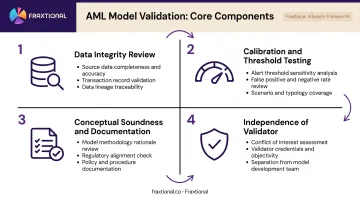

The Four Core Components of an Effective AML Model Validation

SR 11-7 requires every model validation to cover three core model components plus governance controls. That translates to four distinct areas in practice:

1. Data Integrity Review

Before evaluating whether the model logic works, validators confirm that the right data is actually flowing in. A data integrity review verifies:

- All relevant accounts, customers, and transaction types are populating the system

- Transaction codes are mapped correctly — wire, ACH, card, and for crypto-focused firms, on-chain transactions

- Source system feeds are complete and accurate (no silent gaps from system migrations)

- No customer or product segments are excluded unintentionally

Data integrity reviews are often warranted more frequently than full model validations — particularly after system conversions, M&A activity, or when new product lines are added.

2. Calibration and Threshold Testing

This is the above-the-line / below-the-line analysis. The core question: are thresholds catching suspicious activity without generating an unmanageable alert volume? Validators use statistical sampling of scenarios — ideally in a test environment — to:

- Verify that scenario logic is functioning as designed

- Recompute parameter calculations independently to verify model output accuracy

- Assess whether thresholds are set too permissively (missing activity) or too sensitively (alert fatigue)

For classification-based models, statistical measures like K-S statistic, ROC curve, Gini coefficient, and confusion matrix are appropriate tools for evaluating the model's ability to separate risk, as outlined in ACAMS guidance on AML model risk management.

3. Conceptual Soundness and Documentation Review

This component asks whether the model's underlying methodology is defensible. Validators review:

- The rationale behind segmentation decisions and scoring weights

- How threshold choices were made and whether that logic is documented

- Whether the model's purpose and limitations are clearly stated

- Whether expert judgment inputs are recorded and traceable

Missing or outdated documentation is one of the most common findings in regulatory exams. A model that works correctly but cannot demonstrate why it was built the way it was still fails a conceptual soundness review.

4. Independence of the Validator

Regulators require validation to be performed by a party independent from those who developed or manage the model. This means no conflict of interest — the validator cannot also be responsible for the model's performance.

Qualified validators include:

- External auditors or third-party consultants

- Internal teams with no involvement in model development or management

- Fractional compliance leaders or BSA Officers engaged specifically for the validation role

For institutions without an internal independent reviewer, external advisory firms can fill this gap. Fraxtional's independent audit practice, for example, delivers board-ready findings with prioritized remediation guidance — a practical option for firms preparing for regulatory examinations or sponsor bank due diligence reviews.

AML Model Validation Best Practices

Tie Validation Criteria to Model Purpose

A clustering-based segmentation model and a classification-based alert scoring model require different validation criteria. Before testing begins, validators should document the model's intended use and select statistical measures aligned to that purpose — not generic benchmarks that don't fit the model type.

Document Everything, Continuously

Regulators cite documentation gaps more than almost any other finding. A defensible model documentation structure includes:

- Model purpose and intended use

- Input/output decisions and data lineage

- Development rationale and expert judgment records

- Threshold and parameter change history

- Validation findings and remediation actions

- Ongoing monitoring standards and model ownership

This documentation shouldn't live in scattered email threads. Maintain it in a central model record and update it whenever changes occur.

Establish Model Governance Oversight

Model risk oversight requires a dedicated cross-functional body — whether a formal committee or a designated senior function. That body should handle:

- Setting and tracking validation schedules

- Reviewing validation findings and approving remediation

- Approving threshold changes before implementation

- Monitoring model performance between validations

SR 11-7 requires board and senior management oversight of model risk. The FFIEC goes further, specifying that independent testing results must be reported directly to the board or a designated board committee.

Watch for Model Deterioration Between Validations

Four warning signs that a model may be failing before the next scheduled review:

- Alert backlogs — unreviewed alerts accumulating faster than they're being worked

- Policy inconsistency — high-risk customers not generating alerts as expected

- Recurring false positives — the same scenarios firing on the same low-risk activity repeatedly

- Unexplained volume swings — sudden spikes or drops in alert counts without a clear business reason

Any of these signals warrants pulling the model forward for an out-of-cycle review. Logging the issue and waiting for the next scheduled validation is how programs accumulate exam findings.

Model Validation vs. Model Tuning: Key Differences

These two processes are frequently confused — and that confusion has shown up in enforcement actions.

Model tuning is an internal process. The institution or its vendor adjusts parameters and thresholds to improve performance — but no independent review occurs, and tuning never substitutes for validation. ACAMS guidance puts the tuning cycle at every 12 to 18 months.

Validation is a different animal entirely. It's an independent, structured review assessing data integrity, conceptual soundness, and output accuracy — conducted by a party with no conflict of interest in the outcome. Parameter adjustment doesn't come into it.

The USAA enforcement action illustrates what happens when the two get conflated. FinCEN cited USAA for lacking distinct procedures governing both validation and adjustment, including testing, updating, and tuning. Having one without the other leaves a documentable gap — and examiners will find it.

Tuning alone is insufficient when:

- The model hasn't had an independent review in more than two years

- A material change has occurred in the institution's business model or product mix

- A regulatory exam has cited model-related deficiencies

- The model was originally deployed from a third-party vendor without prior independent validation

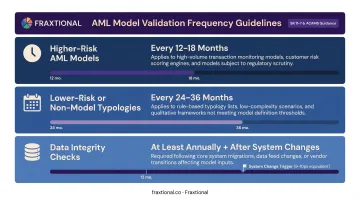

How Often Should You Validate Your AML Model?

General Frequency Guidance

SR 11-7 calls for at least an annual review of each model to assess whether it is working as intended. For BSA/AML-specific systems, the 2021 interagency statement frames frequency as risk-based and tied to changes in the institution's risk profile.

As an industry practice (per ACAMS guidance):

- Higher-risk AML models: independent validation every 12 to 18 months

- Lower-risk or non-model typologies: review every 24 to 36 months

- Data integrity checks: at least annually, and after any system change or integration

Event-Based Triggers

Scheduled cycles set the baseline — but model performance can shift faster than a calendar allows. These events require an out-of-cycle validation regardless of where you are in the schedule:

- Significant changes to model parameters or logic

- New product lines or customer segments added to the risk profile

- Core system conversions or integrations

- Mergers or acquisitions

- Regulatory examination findings citing model deficiencies

The Challenge for Smaller Institutions and Fintechs

Early-stage fintechs and community banks often lack the internal resources to run a recurring validation program. The mistake many make is treating validation as something to address when a regulator asks — by then, the gap is already a finding.

Establishing a validation schedule as part of the initial BSA/AML program governance framework — not as a reaction to exam pressure — is the cleaner path. Firms under sponsor bank relationships face added scrutiny, since sponsor banks now routinely require evidence of independent validation before approving new fintech partners or product expansions.

Fraxtional's fractional BSA Officer and CAMLO engagements address this directly. Senior compliance leadership covering model validation oversight, sponsor bank alignment, and ongoing monitoring — without the overhead of a full-time hire. Engagements typically run three to nine months, structured around the firm's risk profile and regulatory timeline.

Frequently Asked Questions

What is model validation in AML?

AML model validation is an independent review that confirms a financial institution's AML model (transaction monitoring, customer risk rating, and similar systems) is functioning as intended and meeting regulatory expectations. It covers data integrity, scenario logic, output accuracy, and governance documentation.

How often should AML models be validated?

Higher-risk models should be validated every 12 to 18 months; lower-risk typologies every 24 to 36 months. Data integrity checks should occur at least annually.

What is the difference between AML model validation and model tuning?

Model tuning is an internal process that adjusts thresholds and parameters to improve performance. Model validation is an independent, structured assessment of whether the model works as intended — covering data integrity, conceptual soundness, and output accuracy. Regulators expect both; neither substitutes for the other.

Who can perform an independent AML model validation?

Validation must be performed by a party independent from those who developed or manage the model. Qualified validators include external auditors, third-party consultants, or internal reviewers with no involvement in model development. The validator must have no conflict of interest with the model being reviewed.

What are common findings in an AML model validation?

Frequent findings include incomplete or outdated model documentation, incorrect transaction code mapping, thresholds that are either too permissive or too sensitive, insufficient testing of all relevant data sources, and lack of consistent monitoring between validation cycles.

What triggers an AML model validation outside of a regular schedule?

Out-of-cycle validations are required following significant model changes, new product lines or customer segments, core system conversions, mergers or acquisitions, or regulatory examination findings that identify model-related deficiencies.