Introduction

The stablecoin market reached $317 billion in market capitalization by April 2026, processing $28 trillion in real economic activity during 2025 alone. Yet this explosive growth has come with a sobering reality: stablecoins now account for 84% of all illicit virtual asset transaction volume, making compliance the single most urgent operational priority for fintechs, payment service providers (PSPs), and crypto firms in this space.

The core challenge is structural: stablecoins move on decentralized, permissionless blockchain rails but are subject to the same AML/CFT obligations as traditional payment systems.

Many companies enter the stablecoin ecosystem without a clear compliance program in place—no designated BSA Officer, no written AML policy tailored to virtual assets, and no monitoring architecture for on-chain activity. The result: sponsor banks decline partnerships, investors withhold funding, and regulatory deficiency findings pile up.

This article covers the current regulatory landscape shaped by the GENIUS Act and MiCA, KYC obligations adapted to pseudonymous wallets, Travel Rule mechanics for qualifying stablecoin transfers, on-chain transaction monitoring at both customer and ecosystem levels, and how to build a compliance program that scales with your stablecoin operations.

Key Takeaways

- Stablecoin issuers and PSPs face federal AML/CFT obligations: KYC, Travel Rule, and transaction monitoring

- The GENIUS Act (US, 2025) and MiCA (EU) established formal frameworks; FATF sets the global baseline

- KYC must be risk-based, continuous, and include wallet attribution to verified identities

- The Travel Rule requires originator and beneficiary data to accompany qualifying stablecoin transfers between VASPs

- Effective compliance demands dual-layer monitoring: direct customer tracking and ecosystem-level token surveillance

The Stablecoin Compliance Landscape: What's Changed

GENIUS Act Establishes Federal AML Framework

Passed in July 2025, the GENIUS Act classifies permitted payment stablecoin issuers (PPSIs) as financial institutions under the Bank Secrecy Act, subjecting them to the same federal AML/CFT, customer identification, and sanctions compliance obligations as traditional money transmitters.

The Act also mandates that issuers maintain identifiable reserves backing outstanding stablecoins on at least a 1:1 basis, comprising high-quality liquid assets like US currency, demand deposits, and short-term Treasury bills.

Practical impact: Compliance programs must now mirror traditional financial institution structures—written BSA/AML policies, designated compliance officers with clear authority, staff training programs, independent audits, and comprehensive risk assessments covering products, geographies, customer types, and delivery channels.

MiCA and FATF Define Global Standards

The EU's Markets in Crypto-Assets (MiCA) regulation imposes parallel requirements on issuers of asset-referenced tokens (ARTs) and e-money tokens (EMTs), including reserve backing, transaction volume limits, and full AML obligations. MiCA restricts widely-used stablecoins when daily transaction volume exceeds 1 million transactions or €200 million in value within a single currency area.

FATF Recommendation 16 now explicitly applies to virtual asset service providers (VASPs), requiring immediate and secure transmission of originator and beneficiary information for qualifying virtual asset transfers—the foundation of Travel Rule compliance.

Why Enforcement Has Escalated

Regulators escalated enforcement because illicit cryptocurrency addresses received at least $154 billion in 2025, with stablecoins dominating this activity. FATF guidance notes that the majority of illicit stablecoin activity occurs in the secondary market—peer-to-peer transfers that happen outside direct issuer control but still trigger compliance obligations for VASPs facilitating those transfers.

That volume has put every VASP in the spotlight. Sponsor banks and private equity investors now treat a complete, audit-ready compliance program as a prerequisite for partnership. For stablecoin issuers specifically, that means:

- Written AML/CFT policies documented before launch, not retrofitted after

- Independent audits that satisfy sponsor bank due diligence requirements

- Ongoing transaction monitoring covering secondary market P2P flows

- Sanctions screening integrated across all transfer channels

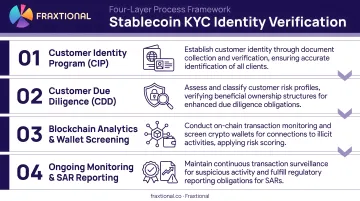

KYC Requirements for Stablecoin Issuers and PSPs

Layered Identity Verification Standards

Stablecoin KYC mirrors traditional Customer Identification Program (CIP) requirements under the BSA, adapted for digital-first onboarding:

- Government-issued ID verification - Passport, driver's license, or national ID with document validation

- Biometric checks - Facial recognition matching photo ID to live selfie

- Proof of address - Utility bills, bank statements, or government correspondence

- Entity verification - For business customers: articles of incorporation, beneficial ownership disclosure, and authorized representative validation

These controls must function in real-time digital workflows, not manual back-office processes, to match the speed of blockchain transactions.

Risk-Based Customer Categorization

Not all customers carry equal risk. Effective programs apply Enhanced Due Diligence (EDD) triggers based on:

High-risk customer segments:

- Users from FATF-designated high-risk jurisdictions (as of February 2026: North Korea, Iran, Myanmar)

- Institutional counterparties exceeding volume thresholds (typically $100,000 daily or $1 million monthly)

- Entities from jurisdictions on the FATF Grey List with strategic AML deficiencies

Behavioral red flags requiring EDD:

- Unusually large or rapid wallet creation patterns

- Transaction structuring designed to stay below reporting thresholds

- Frequent cross-border transfers to unrelated parties

- Activity inconsistent with stated business purpose

These triggers must be defined in written policies and applied systematically, not left to analyst discretion.

Ongoing KYC and Event-Triggered Reviews

Stablecoin compliance programs require continuous KYC obligations that extend well beyond initial onboarding:

- Annual or biennial re-verification of identity documents and beneficial ownership records

- Reviews triggered by risk profile changes — shifts in transaction patterns, jurisdictional exposure, or adverse media findings

- Dynamic risk scoring updated continuously based on on-chain activity

This ongoing obligation is especially important for stablecoins because pseudonymous wallet addresses can obscure beneficial ownership changes and transaction patterns that would be visible in traditional banking.

Wallet Attribution: The Unique Stablecoin Challenge

Wallet attribution — linking blockchain addresses to verified customer identities — is where stablecoin KYC diverges most sharply from traditional payment compliance.

When a customer transfers stablecoins to an external wallet, compliance teams must:

- Maintain mapping of customer-controlled wallet addresses

- Screen destination wallets against sanctions lists and known illicit addresses

- Apply enhanced scrutiny to transfers involving unhosted (self-custodied) wallets

- Use blockchain intelligence tools integrated into KYC workflows to trace fund flows

FATF guidance acknowledges there is no technically proven means to identify wallet owners from blockchain addresses alone. VASPs must implement mitigation measures in response — including holding transactions until screening completes.

The Travel Rule and Stablecoins: What VASPs Must Do

Travel Rule Basics for Stablecoin Transfers

Under FATF Recommendation 16, any qualifying transfer of virtual assets—including stablecoins—between two regulated VASPs must include:

- Originator name

- Originator account or wallet address

- Originator location (jurisdiction)

- Beneficiary name

- Beneficiary account or wallet address

The current US threshold is $3,000 under 31 CFR 1010.410(f), though FinCEN proposed lowering this to $250 for international transfers.

Who Must Comply

The Travel Rule applies to:

- Stablecoin issuers acting as VASPs

- PSPs processing stablecoin settlements

- Crypto exchanges facilitating stablecoin trades

- Money transmitters using stablecoin rails

No exemption exists based on asset type — if your firm touches a qualifying transfer, compliance is mandatory. The technical challenge, however, lies in how that data gets transmitted.

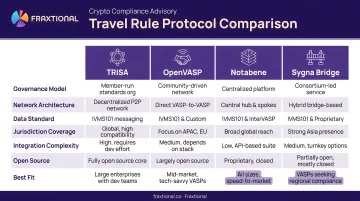

The Interoperability Problem

Travel Rule compliance isn't just about capturing data — it requires secure, real-time transmission to the receiving VASP. No universal messaging standard exists, which means firms must actively choose a protocol network.

| Protocol | Implementation Model |

|---|---|

| TRISA | Open-source, peer-to-peer using trusted Certificate Authority |

| OpenVASP (TRP) | Decentralized standard using "Travel Address" system |

| Notabene | End-to-end solution with Transaction Authorization Protocol (TAP) |

| Sygna Bridge | API-based messaging with TRISA interoperability |

Firms must participate in one or more of these networks to exchange data with counterparties, and they are working toward interoperability across protocols.

The Unhosted Wallet Challenge

When one side of a transfer involves an unhosted wallet (self-custodied, not controlled by a VASP), regulators take varying positions:

- UK approach: Under Part 7A of the MLRs, cryptoasset businesses must request information from customers for unhosted wallet transfers exceeding €1,000

- EU approach: The Transfer of Funds Regulation applies a €0 threshold—all transfers require data collection, even to self-hosted addresses

- US approach: FinCEN has not issued a final rule on unhosted wallets; conservative firms apply enhanced scrutiny to all such transfers regardless of value

Compliance teams must maintain written policies defining their approach, including when to apply enhanced due diligence, delay transactions pending verification, or decline transfers to unhosted wallets entirely. Threshold divergence across jurisdictions adds another layer to this challenge.

Jurisdictional Threshold Fragmentation

Different regulators impose different monetary thresholds and data requirements:

| Jurisdiction | Threshold | Key Requirement |

|---|---|---|

| United States | $3,000 (proposed $250) | Full originator/beneficiary data |

| European Union | €0 (no exemption) | All transfers treated as cross-border |

| United Kingdom | €1,000 (unhosted wallets) | Risk-based information requests |

| Canada | CAD $1,000 equivalent | Full Travel Rule data exchange |

For firms operating across these jurisdictions, a single static policy won't hold. Your compliance architecture needs to apply the correct rule set based on transaction context — originator location, beneficiary location, and the jurisdictions of both VASPs involved. Building that logic into your workflows before you scale is far easier than retrofitting it later.

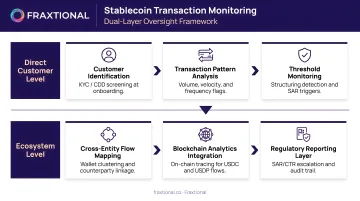

On-Chain Transaction Monitoring: Direct and Ecosystem-Level

The Two-Tier Monitoring Obligation

Regulators including FATF and the Hong Kong Monetary Authority now expect stablecoin issuers and VASPs to implement dual-layer monitoring:

- Direct customer monitoring - Track your own customers' on-chain activity for suspicious patterns

- Ecosystem monitoring - Understand how your token is used across the broader blockchain network, beyond direct counterparties

This distinction is unique to stablecoins and does not exist in traditional finance, where banks don't monitor how cash moves after withdrawal.

Core Direct Monitoring Controls

Velocity checks:

- Unusual transaction frequency (100+ transactions daily vs. historical baseline of 5)

- Rapid volume spikes (10x normal monthly volume compressed into 48 hours)

Behavioral baselining:

- Establish normal patterns per customer segment

- Flag deviations: retail user suddenly transacting institutional volumes, dormant wallet reactivating with large transfers

Counterparty risk scoring:

- Assess wallets your customers transact with

- Real-time sanctions screening against OFAC SDN List, UN consolidated list, and EU sanctions

- Flag transfers to mixers, darknet markets, or wallets linked to ransomware

Geographic risk analysis:

- Track blockchain activity patterns by jurisdiction

- Flag transfers routing through high-risk jurisdictions even if customer is located elsewhere

Chain-Hopping and Cross-Chain Tracing

FinCEN and Treasury risk assessments highlight chain-hopping as a primary stablecoin laundering typology—converting one virtual asset into another before moving funds. This often involves:

- Bridging stablecoins from Ethereum to Binance Smart Chain or Polygon

- Layering through decentralized exchanges (DEXs)

- Using DeFi protocols to obscure fund origins

- Mixing services that aggregate and redistribute tokens

Compliance tools must trace funds across chains, not just within a single blockchain. Most programs monitor activity on their native chain adequately—the gap appears when funds bridge to another network and disappear from view.

SAR/STR Filing Obligations

Under 31 CFR 1022.320, US money services businesses must file a Suspicious Activity Report (SAR) for transactions involving or aggregating at least $2,000 when the MSB knows or suspects funds were derived from illegal activity, designed to evade BSA requirements, or serve no apparent lawful purpose.

Stablecoins add several triggers on top of those baseline requirements:

- Transfers to/from OFAC-sanctioned wallets

- Rapid cross-chain transfers structured to obscure fund origin

- Use of mixers or privacy-enhancing protocols

- Structuring to stay below Travel Rule thresholds

- Patterns matching typologies in FATF's targeted guidance on stablecoins

Ecosystem-Level Monitoring for Issuers

Stablecoin issuers carry a monitoring obligation that extends beyond their direct customer base: tracking all on-chain movement of issued tokens across every wallet that holds them.

In practice, this means:

- Monitoring all wallet addresses holding your stablecoin across the blockchain

- Identifying when your token appears on sanctioned entity wallets, darknet markets, or illicit platforms

- Blacklisting wallet addresses when legally authorized under your protocol

- Reporting patterns to law enforcement when required

Unlike traditional payment processors, issuers retain visibility into how their token moves ecosystem-wide—and regulators increasingly expect them to act on it.

Navigating Multi-Jurisdictional Compliance

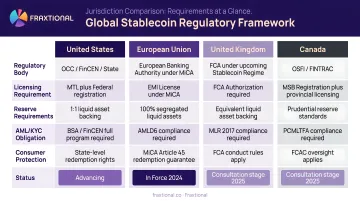

Key Regulatory Regimes for Stablecoin Operations

| Jurisdiction | Primary Framework | Registration Requirement | Key Obligations |

|---|---|---|---|

| United States | GENIUS Act + FinCEN MSB rules | FinCEN MSB registration within 180 days + state MTLs | Federal AML program, 1:1 reserves, Travel Rule, SAR filings |

| European Union | MiCA | CASP authorization via national competent authority | AML obligations, reserve requirements, volume limits, €0 Travel Rule threshold |

| United Kingdom | FCA crypto asset registration under MLRs | FCA registration before trading | Full AML compliance, Travel Rule, unhosted wallet EDD |

| Canada | FINTRAC MSB registration | Registration at business start | AML program, large transaction reporting, Travel Rule |

A single stablecoin product may trigger obligations in multiple jurisdictions at once. A US issuer serving EU customers, for example, must comply with both GENIUS Act reserve requirements and MiCA transaction volume limits.

Practical Compliance Architecture Challenges

Each jurisdiction imposes different requirements:

Data field variations:

- US Travel Rule: Originator/beneficiary name, address, account number

- EU TFR: Additional fields for intermediary CASPs, €0 threshold application

- UK MLRs: Risk-based approach for unhosted wallets, €1,000 threshold

SAR filing format differences:

- US: FinCEN SAR-MSB form, $2,000 threshold

- UK: Suspicious Activity Report to National Crime Agency

- EU: Member state-specific STR formats and thresholds

- Canada: FINTRAC suspicious transaction reporting

Licensing obligations:

- US: Federal FinCEN registration + state-by-state money transmitter licenses (up to 50 jurisdictions)

- EU: Single CASP authorization valid across member states under MiCA passporting

- UK: FCA registration with ongoing supervision

- Canada: Federal FINTRAC registration + provincial MSB licenses where required

Avoiding Regulatory Arbitrage Gaps

Firms that structure operations to avoid one jurisdiction's rules often trigger another's. A stablecoin issuer incorporated in the Cayman Islands but serving US customers cannot avoid FinCEN MSB registration simply by locating offshore.

When jurisdictions conflict, apply the stricter standard across the board. If the EU imposes a €0 Travel Rule threshold and the US applies $3,000, use €0 for all transactions.

Banking partners and investors now expect this posture during pre-deal compliance reviews. A conservative, risk-based approach is one of the clearest signals of operational maturity a stablecoin issuer can send.

Building Your Stablecoin Compliance Program

FinCEN's Five-Pillar BSA/AML Program

Under 31 CFR 1022.210, every MSB—including stablecoin issuers and PSPs—must maintain an AML program incorporating:

- Written policies and procedures documented specifically for your stablecoin business model

- Risk assessment covering products, geographies, customer types, and delivery channels

- Designated compliance officer with clear authority and direct board reporting

- Ongoing employee training covering AML obligations, red flags, and escalation procedures

- Independent audit to test program effectiveness and surface gaps

These five pillars are non-negotiable. FinCEN consistently cites their absence in enforcement actions and deficiency findings.

The Compliance Leadership Gap

Many fintech and crypto startups launching stablecoin products lack a dedicated Chief Compliance Officer, BSA Officer, or CAMLO (Chief Anti-Money Laundering Officer). This is the most frequent reason sponsor banks decline partnerships and regulators issue findings.

Hiring a full-time compliance executive with stablecoin expertise can cost $250,000–$400,000 annually — unworkable for seed-stage companies. Fractional compliance services, covering CCO, BSA Officer, and MLRO roles, provide director-level expertise at a fraction of that cost, giving startups the named accountability banks and regulators require.

Firms like Fraxtional offer fractional leadership specifically for fintech, crypto, and stablecoin issuers — placing experienced officers who can be named in regulatory filings and manage sponsor bank relationships directly.

The Biggest Compliance Design Mistake

That leadership gap connects to a deeper architectural problem. Building compliance as a post-launch remediation effort rather than embedding it from day one is the most common — and most costly — design mistake stablecoin teams make.

Why this fails:

- Retrofitting KYC gating into live transaction flows disrupts user experience

- Adding Travel Rule data capture after launch requires re-engineering wallet infrastructure

- Implementing monitoring hooks post-deployment creates compliance gaps during the interim period

- Sponsor banks and investors increasingly expect to see compliance built into product design during pre-launch reviews

Correct approach: Embed compliance controls at the infrastructure level:

- KYC gating before wallet activation or first transaction

- Travel Rule data capture integrated into transaction submission flows

- Monitoring hooks in smart contracts or API layers to stream transaction data to compliance tools

- Wallet attribution maintained in customer databases from onboarding

Remediating compliance after launch typically costs 3–5× more and delays banking partnerships. Getting the architecture right before launch is what positions a product for faster regulatory approval.

Frequently Asked Questions

What is the regulatory framework for stablecoins?

The US GENIUS Act (2025) establishes a federal licensing and AML framework for permitted payment stablecoin issuers. The EU's MiCA regulation imposes reserve requirements, transaction limits, and AML obligations on asset-referenced and e-money tokens. Globally, FATF's virtual asset guidance applies AML/CFT obligations including the Travel Rule, while FinCEN classifies stablecoin issuers as money transmitters subject to BSA requirements.

What is the FDIC stablecoin rule?

In December 2025, the FDIC approved application procedures for FDIC-supervised institutions seeking to issue payment stablecoins under the GENIUS Act. By April 2026, the FDIC clarified that stablecoin reserves may qualify for pass-through deposit insurance, with tokenized deposits treated the same as traditional deposits under the Federal Deposit Insurance Act.

What are the most regulated stablecoins?

Fiat-backed stablecoins pegged to major currencies face the strictest regulatory scrutiny because they most closely resemble regulated payment instruments. USDT (Tether) and USDC (Circle) account for 93% of total stablecoin market capitalization and face licensing, reserve backing, and AML obligations under both MiCA and the GENIUS Act.

What are the 4 types of stablecoin?

The four types are fiat-backed (pegged to a currency, backed by cash or equivalents), commodity-backed (backed by assets like gold), crypto-backed (overcollateralized with crypto), and algorithmic (peg maintained through supply mechanics without full reserves). Compliance obligations differ by type — the GENIUS Act explicitly excludes algorithmic stablecoins because they cannot maintain the required 1:1 reserve backing.

What are the best platforms for integrating stablecoin payments into core banking systems?

The technical platform is only part of the answer — embedding KYC, Travel Rule, and transaction monitoring controls into the integration is just as important. Work with a compliance specialist familiar with both banking regulations and crypto asset frameworks before selecting a solution, particularly if you operate across multiple jurisdictions.