Introduction

Many crypto companies struggle with the complexity and cost of U.S. regulatory compliance. Traditional money transmitter licensing in states like New York or California can take 12–18 months, require surety bonds exceeding $500,000, and cost tens of thousands in application fees alone. For early-stage exchanges, custodial wallet providers, and international teams, this creates a real barrier to U.S. market entry.

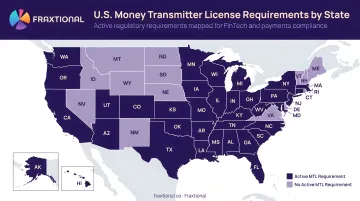

Montana offers a different path. It's the only U.S. state with no state-level Money Transmitter License (MTL) requirement, meaning crypto businesses register at the federal level with FinCEN instead. Research from the Congressional Research Service confirms that "all states except Montana have passed money transmitter laws."

This guide covers what you need to know if you're running a crypto exchange, custodial wallet, payment gateway, or remittance platform — especially if you're early-stage or entering the U.S. from abroad:

- What a Montana MSB actually is and how it differs from an MTL

- Why Montana appeals to crypto businesses

- How FinCEN registration works, step by step

- What federal obligations still apply

- Where this structure has real limits

Getting the structure right from day one matters for banking relationships, investor credibility, and federal compliance.

Key Takeaways

- Montana is the only U.S. state with no state-level MSB or money transmitter license—crypto businesses register federally with FinCEN instead

- Getting set up means forming a Montana LLC, filing FinCEN Form 107, and maintaining a BSA-compliant AML program

- "Montana crypto license" is informal shorthand—it's a federal MSB registration, not a state-issued license

- Federal BSA/AML obligations still apply in full—KYC, transaction monitoring, SAR filing, and OFAC screening

- Montana MSB does not authorize serving all 50 U.S. states—other states may still require their own licenses

What Is a Montana MSB for Crypto?

A Money Services Business (MSB) is any business that transmits funds, exchanges currency, or deals in convertible virtual currency (CVC). Under FinCEN's 2019 guidance, "Hosted wallet providers are account-based money transmitters that receive, store, and transmit CVCs on behalf of their accountholders."

The following business types fall within the MSB definition:

- Crypto exchanges (centralized and peer-to-peer)

- Custodial wallet providers

- Payment gateways processing crypto transactions

- CVC administrators issuing or redeeming virtual currency

In Montana, there's no state licensing layer. The Montana Division of Banking and Financial Institutions explicitly states: "The Montana Division of Banking and Financial Institutions (Division) does not regulate money transmitters." Unlike every other U.S. state, Montana has no state MTL framework, so the entire regulatory obligation sits at the federal level under the Bank Secrecy Act (BSA) and FinCEN.

The "Montana Crypto License" Label vs. Reality

What people call a "Montana crypto license" is technically a federal MSB registration filed with FinCEN by a Montana-incorporated entity, not a state-issued license. This distinction matters when setting expectations with banks and investors. The structure removes one regulatory layer, but full federal compliance under BSA and FinCEN still applies.

Why Crypto Companies Choose Montana

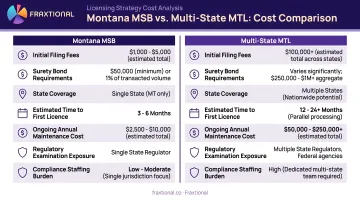

No State Licensing Regime

Montana's position here is straightforward: There's no surety bond at the state level, no state application fees, no state examination schedule specific to money transmission. Contrast this with:

- New York BitLicense: $5,000 application fee

- Texas MTL: $10,000 nonrefundable application fee plus $100,000 to $500,000 surety bond

- Washington MTL: $1,000 application fee plus $10,000 to $550,000 surety bond

Speed to Market

Because there's no state MTL process, a compliant Montana MSB structure can realistically be operational in four to eight weeks. The breakdown:

- LLC Formation: 1-3 business days with expedited processing

- EIN Acquisition: 1-5 business days for international applicants by phone, 4 business days by fax

- Compliance Framework: 2-4 weeks for policy drafting and risk assessment

- FinCEN Registration: Added to public MSB registry within approximately two weeks

This timeline assumes you have a qualified compliance team in place. Early-stage companies that can't yet justify a full-time BSA Officer often work with fractional compliance providers to meet examiner and banking partner standards from the start.

Foreign Founder Advantage

Montana places no restrictions on international founders. Key facts for foreign applicants:

- 100% foreign ownership of a Montana LLC is permitted

- Only a registered agent with a Montana address is required — no staffed office

- No residency requirements for owners or control persons

- EIN available by phone through the IRS, bypassing the longer mail process

Use-Case Fit

Not every crypto business needs a state MTL — but most custodial models do. Here's how common structures typically fall:

Best suited for:

- Centralized crypto exchanges

- OTC desks

- Custodial wallet providers

- Crypto payment gateways

- Cross-border remittance platforms using crypto rails

- Stablecoin issuers

May not need MSB treatment:

- Fully non-custodial software where the operator never controls keys or funds (FinCEN's 2019 guidance clarifies that unhosted wallet users conducting transactions "on the user's own behalf" are not money transmitters)

Cost Efficiency

Montana Entity Setup:

| Item | Cost |

|---|---|

| Montana LLC Articles of Organization | $35 standard, $55 (24-hour expedite), $135 (1-hour expedite) |

| Registered Agent | $100-$300/year |

| FinCEN Form 107 Registration | $0 |

Federal-Only Compliance vs. Multi-State Licensing:

A Montana MSB setup costs under $500 in formation and registration fees. Multi-state MTL applications can easily exceed $50,000 in fees and bonds before you serve a single customer.

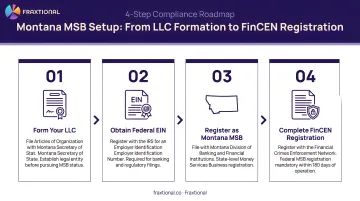

How Montana MSB Registration Works

The overall structure rests on three pillars:

- Montana entity formation

- FinCEN registration via Form 107

- Documented federal-grade AML compliance program

All three must be in place before commercial operations begin. The FinCEN Form 107 filing is a notification to the U.S. Treasury, not a discretionary approval process—but incomplete or inaccurate filings create serious compliance exposure.

Step 1: Map Your Business and MSB Categories

Determine which FinCEN MSB categories apply to your business:

- Money transmitter: Accepts currency, funds, or other value that substitutes for currency and transmits it

- Dealer in foreign exchange: Exchanges currency for customers exceeding $1,000 in any person on any day

- Provider of prepaid access: Sells or loads prepaid access

- Administrator/exchanger of CVC: Accepts and transmits virtual currency or buys/sells it

This mapping shapes your Form 107 filing, risk assessment, and AML program scope.

Step 2: Form the Montana LLC

Process:

- Reserve a business name with the Montana Secretary of State

- File Articles of Organization ($35 standard filing fee)

- Appoint a registered agent with a Montana address

- Obtain an Employer Identification Number (EIN) from the IRS

Timeline: A few business days with standard processing, 1-2 days with expedited filing.

Step 3: Build the AML/BSA Compliance Framework

Before filing with FinCEN, the business must have a documented, risk-based AML program in place. Under 31 CFR 1022.210, this includes:

- Written policies and procedures approved by senior management

- Designated Compliance Officer with authority and resources

- Risk-based KYC/CDD procedures tailored to your customer base

- SAR and CTR procedures with clear thresholds and filing steps

- OFAC sanctions screening tools integrated into onboarding and transactions

- Staff training plan with regular updates and testing

Building this framework typically takes longer than any other step — expect several weeks if starting from scratch. Banks will review your AML program in detail during onboarding, and a weak or template-based compliance framework is a common reason MSBs are turned away at the banking stage. Get it right before filing.

Step 4: File FinCEN Form 107

Filing steps:

- Enroll in the BSA E-Filing system

- Complete Form 107 with:

- Legal entity details

- Ownership structure

- MSB activity categories

- Geography of operations

- Compliance contact information

- Submit electronically

The filing itself is typically completed in one to two business days once your AML program and entity documents are finalized. Per the Form 107 instructions, initial registration must be filed "on or before the end of the 180-day period beginning on the day following the date the business is established." Renew registration every two years, on or before December 31.

Step 5: Secure Banking and Payment Partners

Once your MSB registration and compliance documentation are in place, you can approach MSB-friendly banks, EMIs, and payment providers. Banks will request:

- Your FinCEN registration confirmation

- Complete AML program documentation

- Risk assessment

- Sample transaction monitoring reports

- Evidence of OFAC screening implementation

- Compliance Officer résumé and qualifications

Banks face real regulatory pressure to avoid high-risk MSB relationships, and many decline before reviewing a single document. A compliance program with clear policies, an experienced officer, and documented controls gives you a realistic shot at getting across the line.

Federal Compliance Obligations That Still Apply

Montana removes the state regulatory layer, but federal BSA obligations apply in full. A Montana MSB is examined by IRS specialist examiners and must demonstrate a functioning compliance program — not just a filed form.

Core AML Program Requirements

Under federal law, your program must include:

- Written policies approved by senior management and updated regularly

- Designated Compliance Officer with real authority and resources

- Risk-based customer due diligence (CDD) and KYC tailored to your business model

- Recordkeeping for a minimum of five years

- Independent testing of the program on a regular basis

Examiners may request training records, SAR examples, and monitoring evidence during audits.

Transaction Monitoring and Reporting Duties

Suspicious Activity Reports (SARs):

Under 31 CFR 1022.320, MSBs must file a SAR for transactions conducted or attempted involving or aggregating funds of at least $2,000 if the MSB knows or suspects the transaction involves illegal activity or lacks a lawful purpose. SARs must be filed no later than 30 calendar days after initial detection.

Currency Transaction Reports (CTRs):

MSBs must file a CTR for transactions involving currency of more than $10,000.

Sanctions Screening

OFAC compliance applies to every U.S.-registered entity without exception. Crypto businesses face particular exposure due to wallet address screening requirements. OFAC FAQs state that "Blocked virtual currency must be reported to OFAC within 10 business days."

The Compliance Officer role carries real weight with examiners — they want to see someone with actual authority, not just a title. For early-stage crypto companies that can't yet justify a full-time hire, Fraxtional's fractional BSA Officer service places a director-level compliance lead into your program, providing the examiner-ready documentation and banking partner credibility you need without the full-time overhead.

Key Limitations and Misconceptions

Montana MSB ≠ Nationwide License

The most common misconception: a Montana MSB registration does not authorize a business to serve customers across all 50 U.S. states. Each state retains the right to enforce its own money transmission laws.

The Conference of State Bank Supervisors (CSBS) notes that "State authority extends over the entirety of the licensed entity. Accordingly, the multistate and any multinational activities of a licensee are fully within the scope of coordinated annual state examinations."

Examples of state enforcement:

- Washington: Persons buying or selling virtual currency as a business generally fall under money transmission rules and must hold a state MTL when serving Washington residents

- Texas: The state treats cryptocurrency-to-fiat exchanges through third-party exchangers as money transmission under state law

Operating in a state without the required local MTL creates real regulatory and legal exposure. Montana gives you a federal compliance foundation — state-by-state licensing is still your responsibility from there.

What "No State License Required" Actually Means

This phrase means no Montana state MTL is required — not that your business is deregulated. You still face:

- Federal BSA examination by the IRS

- Full AML program compliance

- FinCEN reporting obligations

- State licensing requirements in customer jurisdictions

Beyond regulators, banks and payment partners will independently evaluate your compliance program quality — regardless of where you're incorporated.

When Montana MSB May Not Be the Right Fit

Consider alternatives if:

- Your platform is fully non-custodial and you never control keys or funds (may not fall under MSB rules at all)

- You're targeting a single foreign market without U.S. customer intent (a U.S. MSB may be more structure than needed)

- You're planning immediate nationwide U.S. retail operations (you'll need a broader state licensing strategy from the outset)

Frequently Asked Questions

Does Montana require a money transmitter license?

No—Montana is the only U.S. state with no state-level money transmitter license requirement. However, businesses conducting money transmission or crypto-related financial services must still register with FinCEN as an MSB and comply with all federal BSA/AML obligations.

What is the difference between a money transmitter and a payment processor?

A money transmitter moves funds on behalf of customers and is classified as an MSB under FinCEN rules, requiring registration and AML compliance. A payment processor facilitates transactions between merchants and card networks without taking custody of funds. That custody distinction determines whether MSB registration applies.

Can a Montana MSB legally serve customers in all 50 U.S. states?

No—Montana's lack of a state MTL only removes the Montana state licensing layer. Other states may require their own money transmitter licenses, and operating in those states without the appropriate license creates regulatory exposure.

How long does it take to register as an MSB with FinCEN?

The FinCEN Form 107 filing can typically be completed in one to two business days. The full process (Montana LLC formation, EIN, and compliance framework) realistically takes four to eight weeks end-to-end.

Does a Montana MSB still need a formal AML compliance program?

Yes—a written, risk-based AML program is a federal requirement under the BSA. This includes KYC procedures, a designated Compliance Officer, transaction monitoring, SAR/CTR filing, OFAC screening, and regular independent testing.

Can foreign nationals or non-U.S. companies own a Montana MSB?

Yes—Montana allows 100% foreign ownership of an LLC, with no residency requirement for owners or control persons. Founders must appoint a registered agent in Montana and obtain a U.S. EIN, but a staffed physical office in Montana is not required.