Introduction

Most fintechs don't learn the full cost of a sponsor bank relationship until they're already deep in negotiations. Setup fees, reserve requirements, basis points on transaction volume, and ongoing compliance obligations stack up in ways that early-stage teams rarely budget for.

The stakes are high. Switching sponsor banks mid-program is operationally painful and expensive, making it critical to understand both sides of the equation before signing anything.

This guide covers what you'll pay, what you get in return, what compliance obligations come with the territory, and how to negotiate more favorable terms from the start.

TLDR

- Sponsor bank fees fall into three buckets: pre-launch, recurring, and variable — each requires separate budgeting

- The real value isn't just compliance cover — it's access to payment rails and card networks that non-chartered entities simply cannot access

- Banks price for perceived risk, so compliance maturity directly affects the fees you'll be quoted

- Run a structured RFP with multiple banks to create competitive tension and compare terms side by side

- Reserve conditions, SLAs, and exclusivity clauses deserve as much attention as the headline fee rate

What Is a Sponsor Bank and Why Do Fintechs Need One?

A sponsor bank is a federally or state-chartered bank that partners with a fintech to legally provide financial services — account holding, card issuance, lending, and money movement. Without a bank charter of their own, fintechs have no legal path to operating in most payment and deposit categories without one.

The charter requirement runs deeper than most founders realize. Access to Federal Reserve payment rails — ACH, Fedwire, FedNow, and real-time payments through The Clearing House's RTP network — is restricted to depository institutions and eligible financial institutions.

The Federal Reserve confirms that financial institutions access Reserve Bank services through a master account or by routing through another institution that holds one. Non-chartered fintechs fall into the second category, which is exactly why the sponsor bank relationship exists.

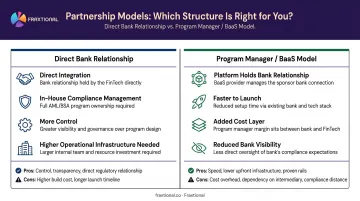

Two Partnership Models

Fintechs typically structure their sponsor bank relationship in one of two ways:

- Direct bank relationship — the fintech integrates directly with the bank and manages compliance in-house. Offers more control, but requires more operational infrastructure.

- Program manager / BaaS model — a Banking-as-a-Service platform or card issuer holds the bank relationship and manages integrations. Faster to launch, but adds a cost layer and reduces direct visibility into the bank relationship.

Neither model eliminates compliance responsibility. 2023 interagency guidance from the OCC and Federal Reserve states that a bank's use of third parties does not diminish its responsibility to operate safely and comply with applicable laws. That accountability flows directly back to how the bank manages its fintech partners.

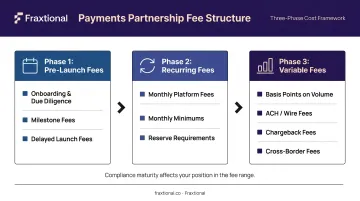

Types of Sponsor Bank Fees: A Complete Breakdown

Sponsor bank fees don't arrive in a single invoice. They accumulate across three distinct phases: pre-launch, ongoing, and variable. Understanding which bucket each fee falls into helps fintechs budget accurately and compare banks on a consistent basis.

Pre-Launch and Setup Fees

Before your program goes live, expect the bank to charge for the work of evaluating you. These typically include:

- Onboarding and due diligence fees — covering the bank's review of your compliance program, legal structure, and business model

- Milestone fees — triggered at specific points, commonly at term sheet signing and at program launch

- Delayed launch fees — charged if the fintech is slow to go live after the bank has completed its diligence work

Lithic's guide to landing a sponsor bank confirms these fee categories, noting that pre-product-launch milestone fees typically kick in at term sheet signing and at program launch. Precise dollar ranges vary by bank and program complexity — always request itemized fee schedules from banks directly rather than relying on published benchmarks.

Ongoing and Recurring Fees

Once the program is live, recurring fees typically include:

- Monthly platform or maintenance fees — covering the bank's ongoing oversight, compliance program maintenance, and administrative burden

- Monthly minimums — a floor charge that applies regardless of transaction volume, most relevant for early-stage programs with lower volumes

- Reserve requirements — many banks require fintechs to hold a cash buffer, often calculated as several days of transaction volume; this is working capital locked up for the life of the contract, not a direct expense, but a real drag on liquidity

Variable and Transaction-Based Fees

These fees scale with program activity. They're also where the real economic exposure accumulates at scale:

- Basis points on transaction volume — a percentage of total processed volume, structured as either a take rate on interchange or a straight volume fee

- ACH transfer fees — per-transaction charges on originations and returns

- Wire fees — per-transaction charges, typically higher than ACH

- Chargeback fees — charged per dispute, and these accumulate quickly in consumer-facing programs

- Cross-border transaction fees — applied to international transactions, relevant for remittance or cross-border payment programs

Note that rates differ materially between payments programs and lending programs — factor that in when modeling volume-based costs.

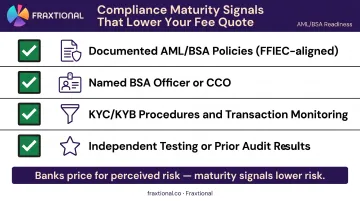

Your compliance maturity directly affects where in the fee range you land. Banks price for perceived risk. A fintech that shows up with documented AML policies, experienced compliance leadership, and a clean operating history looks like a lower-risk partner — and gets quoted accordingly.

The Benefits Fintechs Gain From Sponsor Bank Partnerships

Fees represent cost. But what a sponsor bank unlocks is simply unavailable to any non-chartered entity through any other path.

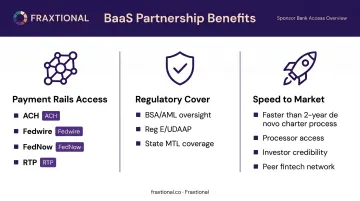

Access to Payment Rails and Card Networks

The most fundamental benefit is access to payment infrastructure that is legally restricted to chartered institutions:

- ACH — sponsor bank acts as the Originating Depository Financial Institution (ODFI), enabling the fintech to originate and receive ACH transactions

- Fedwire — wire transfer access flows through the bank's Federal Reserve account

- FedNow — available only to depository institutions eligible to hold Reserve Bank accounts; non-bank providers access it through those institutions

- RTP — The Clearing House's real-time payments network requires insured depository institution participation

Card issuance works the same way. Visa confirms that a BIN sponsor is the issuing bank that owns the BIN necessary to access the Visa network. Mastercard's rules similarly define BIN Sponsor roles and now require approval for sponsored program manager activity. Without a bank sponsoring your BIN, card issuance simply isn't possible.

Regulatory Cover and Compliance Infrastructure

Operating under a sponsor bank's regulatory umbrella provides coverage that would take years and significant resources to build independently:

- BSA/AML program oversight

- Consumer protection compliance (Reg E, UDAAP)

- State money transmitter licensing coverage in many cases

The BSA requires each bank to establish a BSA/AML compliance program — and that program extends to the fintech programs they sponsor. For early-stage fintechs, operating inside that infrastructure is considerably cheaper and faster than building equivalent frameworks independently — often saving a year or more of regulatory groundwork.

Speed to Market and Network Effects

Pursuing a de novo bank charter is the alternative to a sponsor bank partnership. The OCC's licensing manual notes the de novo phase can extend beyond two years — and that's before factoring in the capital requirements and operational complexity of running a chartered institution.

An experienced sponsor bank compresses that timeline dramatically. Beyond speed, well-connected banks open doors to:

- Processors and technology partners already familiar with fintech programs

- Investors who treat bank endorsement as a credibility signal

- Other fintechs in the sponsor's portfolio — a built-in peer network

Compliance Obligations Sponsor Banks Require From Fintechs

Sponsor banks are accountable to regulators for every program they support. That accountability flows directly back to their fintech partners in the form of documented compliance requirements.

Pre-Launch Due Diligence

Before onboarding, expect detailed reviews of:

- AML/BSA program documentation

- KYC and KYB procedures

- Transaction monitoring framework

- Fraud controls and customer identification procedures

Fraxtional has worked through this process with fintechs across prepaid, lending, deposit, and crypto verticals. Most bank conversations stall during due diligence because compliance documentation isn't ready — not because the product is flawed. Arriving with an audit-ready compliance stack, defensible policies, and named compliance leadership already in place changes the dynamic entirely.

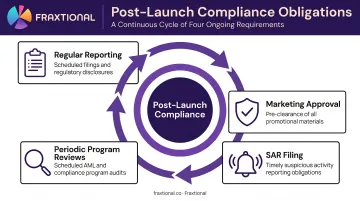

Ongoing Post-Launch Obligations

After launch, the compliance relationship continues through:

- Regular reporting to the bank on program activity and risk metrics

- Marketing material approval — banks require pre-approval of customer-facing materials, often with defined SLA turnaround times that should be negotiated in the contract

- SAR filing responsibilities — shared or delegated obligations for Suspicious Activity Reports

- Periodic program reviews — the bank will conduct ongoing assessments of your compliance program's effectiveness

Fintechs operating in high-risk verticals (crypto, cross-border remittance, and similar categories) face heightened scrutiny on all of the above. Some banks will decline these programs regardless of compliance quality, which makes early alignment on the bank's risk appetite a critical part of the selection process.

One example from Fraxtional's experience: a prepaid wallet startup that had approached multiple banks independently with no traction was onboarded in under 60 days after a single targeted introduction. The difference was fit — the fintech's profile matched the bank's actual risk appetite.

How to Negotiate Sponsor Bank Fees More Effectively

Run a Structured RFP

Sending a structured Request for Proposal to multiple banks simultaneously creates competitive tension and puts you in a position to compare pricing models, capabilities, and contract terms on equal footing. Without competitive pressure, banks have little incentive to move off standard terms.

The RFP should cover more than headline fees. Use it to surface differences in:

- Reserve size requirements and release conditions

- SLA commitments for marketing and document approvals

- Exclusivity clauses that would prevent you from adding a backup banking relationship

- Termination rights and notice periods

- Whether setup and diligence fees are one-time or repeatable for program expansions

Banks often defer these details to the definitive agreement stage. Raising them in the RFP forces earlier transparency and prevents surprises.

Negotiate Specific Financial Terms

Beyond the RFP structure, push back on these specific items:

- Negotiate basis point take rates against projected volume tiers and seek step-downs as the program scales

- Challenge reserve size formulas and the conditions under which reserves can be released

- Confirm whether setup and diligence fees are one-time or apply again for product expansions

- Secure grace periods on monthly minimums tied to actual program ramp timelines

Use Compliance Maturity as Leverage

Banks price for perceived risk. The most effective lever in fee negotiations is demonstrating that your compliance program is already mature before you sit down at the table.

This means arriving with:

- Documented AML/BSA policies aligned to FFIEC standards

- A named BSA Officer or CCO — whether full-time or fractional

- Clear KYC/KYB procedures and transaction monitoring frameworks

- Evidence of independent testing or prior audit results

This is where engaging fractional compliance leadership before approaching sponsor banks pays for itself. A fintech that arrives with a named fractional CCO or BSA Officer and audit-ready documentation signals institutional maturity — banks associate that with lower-risk programs and price accordingly.

Fraxtional's fractional BSA Officer and CCO Directors are regularly listed as named officers in bank submissions and regulatory filings, giving clients the compliance standing that influences how sponsor banks evaluate and quote their programs.

Frequently Asked Questions

What is a sponsor bank in payments?

A sponsor bank is a federally or state-chartered bank that partners with a fintech or payment company to provide access to banking services, card networks, and payment rails. Non-chartered entities cannot legally hold deposits, issue cards, or access ACH and wire systems independently — the sponsor bank provides that access through its own charter and network memberships.

What are typical sponsor bank fees?

Fee structures vary by program type and risk profile. Common categories include setup and due diligence fees, monthly platform fees, reserve requirements, and ongoing transaction-based fees expressed as basis points on volume. Fees are negotiated individually, so request itemized quotes directly from multiple banks before committing to any structure.

What compliance requirements do sponsor banks impose on fintechs?

Core requirements include a documented BSA/AML program, KYC and KYB procedures, transaction monitoring controls, SAR filing protocols, and a marketing review process. Fintechs in higher-risk verticals — crypto, cross-border remittance — face additional scrutiny and stronger internal control expectations to satisfy a bank's risk appetite.

How do fintechs negotiate better sponsor bank fee terms?

Run a structured RFP with multiple banks to create competitive tension, negotiate reserve conditions and SLA terms early rather than at the definitive agreement stage, and demonstrate compliance maturity before entering negotiations. Banks price for perceived risk — a fintech with documented programs and named compliance leadership is consistently positioned to receive more favorable pricing.

Can a fintech work with multiple sponsor banks simultaneously?

Yes, but many contracts include exclusivity clauses that block adding a backup bank. Negotiate that term upfront — securing the right to add a second banking relationship from day one improves operational redundancy and reduces concentration risk without requiring a later renegotiation.

How long does it take to secure a sponsor bank partnership?

Timelines vary considerably. Banks with thorough diligence processes can take several months from initial outreach to program launch. Fintechs that arrive with complete compliance documentation, named leadership, and credible volume projections move through the process faster. For reference, the OCC notes that obtaining a de novo bank charter can take beyond two years. Even a multi-month sponsor bank process is a faster path to market by comparison.