The companies caught in these actions weren't all reckless. Many simply let compliance drift — no structured review process, no documented gap analysis, no early warning system.

This article covers what a compliance review is, how it differs from a formal audit, why it matters for fintechs and financial institutions, what it should include, and how to run one effectively.

Key Takeaways

- A compliance review is an internal, proactive self-assessment — distinct from any regulator-initiated examination

- Unlike a compliance audit, a review carries no external authority, narrower scope, and no formal enforcement consequence

- Financial services reviews must cover AML/BSA, KYC, consumer protection, data privacy, and marketing compliance

- Jurisdiction shapes which regulators apply — FinCEN and CFPB in the US, FCA in the UK, FINTRAC in Canada, and national competent authorities across the EU

- Early-stage fintechs and money transmitters can use fractional compliance leadership in place of a full-time CCO

What Is a Compliance Review?

A compliance review is a structured, internally initiated assessment of an organization's operations, policies, and procedures against applicable laws, regulations, and internal standards. The company runs it — not a regulator. That makes it a risk management tool, not an enforcement mechanism. The firm controls the scope, timing, and findings, which means gaps can be addressed before a regulator ever sees them.

For fintechs, banks, money transmitters, and crypto firms, a compliance review isn't a generic checklist. It maps the specific regulatory obligations that apply to the business model. That typically includes:

- AML/BSA obligations — transaction monitoring, SAR filing processes, staff training

- KYC and customer due diligence — onboarding procedures, identity verification, beneficial ownership

- Consumer protection rules — UDAAP obligations, Reg E, complaint handling

- Data privacy — GDPR, CCPA, and sector-specific cybersecurity standards

- Marketing and communications — disclosure accuracy, fair representation of financial products

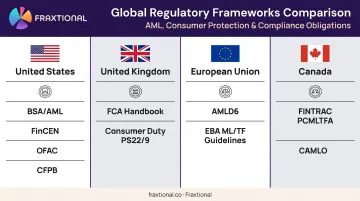

How Jurisdiction Shapes Scope

Regulatory frameworks vary enough across markets that the same review scope won't transfer cleanly from one jurisdiction to another. A US payments firm operates under BSA/AML and CFPB rules; a UK e-money institution answers to the FCA Handbook and Consumer Duty. The applicable frameworks determine what gets reviewed:

| Jurisdiction | Key Frameworks |

|---|---|

| United States | BSA/AML, FinCEN, OFAC sanctions, CFPB consumer rules |

| United Kingdom | FCA Handbook, Consumer Duty (PS22/9) |

| European Union | AMLD6, EBA ML/TF risk-factor guidelines |

| Canada | FINTRAC PCMLTFA, CAMLO requirements |

Companies operating across multiple markets need discrete review modules for each jurisdiction. In practice, that means separate workstreams, different document requests, and often different subject matter leads — particularly where MLRO obligations (UK) or CAMLO requirements (Canada) create distinct accountability structures.

Compliance Review vs. Compliance Audit: Key Differences

These terms get used interchangeably, but they describe fundamentally different activities with different consequences.

A compliance review is internal and self-directed. The company designs it, runs it, and acts on the findings. A compliance audit is external — conducted by regulators, independent third parties, or external auditors — and carries real enforcement weight. The FFIEC BSA/AML Examination Manual is explicit: independent testing assesses BSA compliance relative to the bank's risk profile and determines the adequacy of the compliance program. That is a fundamentally different posture than internal monitoring.

Three Dimensions of Difference

| Dimension | Compliance Review | Compliance Audit |

|---|---|---|

| Initiation | Self-initiated by the company | Scheduled by regulator or external body |

| Scope | Broad, ongoing, risk-based | Focused on specific controls or statements |

| Consequence | Identifies gaps to fix internally | Can result in fines, sanctions, or corrective orders |

The OCC draws a clear line here: monitoring and audit activities both measure material consumer compliance risk, but they operate at different levels of independence and assurance. That distinction determines what regulators can actually do with the findings.

Why This Distinction Has Practical Value

A well-documented compliance review reduces the likelihood of adverse findings during a formal examination. It also creates a paper trail showing that the company identifies gaps and closes them — not under pressure, but proactively.

Sponsor banks and institutional investors expect to see this evidence before entering or maintaining a partnership. A company that can produce a history of internal reviews, corrective actions, and documented follow-through moves through due diligence faster and with fewer conditions attached than one assembling this record for the first time during an exam.

Why Regular Compliance Reviews Matter for Fintech and Financial Services

Regulatory Change Creates Constant Gaps

Financial regulations across all major jurisdictions evolve continuously. The FCA's Consumer Duty introduced new outcome-based requirements in 2023. CFPB supervisory priorities shift with administration changes. FinCEN's AML program rules continue to expand.

Without a regular review cycle, those changes create invisible gaps: obligations the company hasn't updated its procedures to meet. By the time an examiner finds them, the window for quiet remediation has closed.

Risk Surfaces Before It Escalates

Compliance reviews create a structured opportunity to catch vulnerabilities early: miscalibrated transaction monitoring thresholds, KYC procedures that haven't kept pace with product changes, third-party vendors the team never re-assessed after scope expansions. The CFPB's 2024 action against Chime Financial — for illegally delaying consumer refunds on closed accounts — illustrates exactly this pattern. The underlying issue wasn't deliberate misconduct; it was a process gap that accumulated undetected.

Sponsor Banks and Investors Expect Evidence

For fintechs seeking or maintaining sponsor bank relationships, a documented compliance review history is tangible proof of program maturity. Banks want to see that compliance is managed proactively, not reactively. They expect to review:

- Current policies and procedures mapped to applicable regulations

- Evidence of periodic gap assessments

- Corrective action logs showing issues were identified and resolved

- Named compliance leadership who can field their questions

A company showing up to sponsor bank due diligence without this documentation faces delays, enhanced monitoring, or outright rejection.

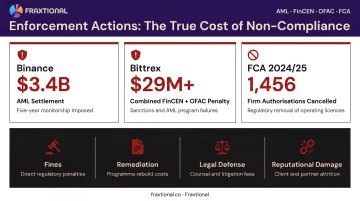

Non-Compliance Costs Far More Than a Review Program

Recent enforcement actions show exactly what's at stake:

- Binance: $3.4 billion AML settlement, plus a five-year monitorship

- Bittrex: Parallel FinCEN and OFAC actions totaling over $29 million

- FCA (2024/25): 1,456 firm authorizations cancelled — not fines, but the legal right to operate

These outcomes compound. Fines, remediation costs, legal defense, operational disruption, and reputational damage stack on top of each other. A structured internal review program costs a fraction of any one of these outcomes.

Key Areas Covered in a Financial Services Compliance Review

BSA/AML and Sanctions

For any covered financial services firm, AML controls sit at the center of a compliance review. The Bank Secrecy Act authorizes Treasury to impose reporting requirements on financial institutions to detect and prevent money laundering. Reviewers should assess:

- Whether transaction monitoring systems are properly calibrated to the firm's risk profile

- SAR filing processes: timeliness, completeness, and escalation workflows

- OFAC sanctions screening against current SDN and non-SDN lists

- Staff training currency and documentation

The five-pillar BSA/AML structure (internal controls, independent testing, designated compliance officer, training, and CDD) provides a useful checklist framework for this section.

KYC and Customer Due Diligence

FinCEN's CDD Rule requires covered financial institutions to maintain written procedures for identifying and verifying beneficial owners of legal entity customers, with a 25% ownership threshold and one control-person requirement. KYC gaps are a consistent finding in regulatory examinations of growth-stage financial businesses.

The FCA's review of challenger banks found weaknesses in governance, customer risk assessment, enhanced due diligence procedures, and transaction monitoring across multiple firms — a pattern that applies to US and UK fintechs alike.

A review of KYC procedures should cover:

- Identity verification processes for individual and entity customers

- Beneficial ownership collection and verification

- Enhanced due diligence procedures for high-risk customers

- Periodic refresh processes for existing customer records

Consumer Protection and Fair Practices

US fintechs must assess adherence to UDAAP requirements (covering unfair, deceptive, or abusive acts or practices) along with Reg E obligations for electronic fund transfers. The CFPB's 2024 circular on remittance providers noted that deceptive marketing about transfer speed or cost can itself constitute a violation.

UK firms face parallel obligations under FCA Consumer Duty, which sets requirements across four outcomes: products and services, price and value, consumer understanding, and consumer support.

Reviewers typically examine disclosures, complaint handling procedures, product suitability processes, and account closure controls.

Data Privacy and Cybersecurity

Data privacy has become a core component of financial compliance reviews, sitting alongside consumer protection in most examinations. A review should address:

- GDPR/UK GDPR — for EU and UK operations, covering accountability, security, and breach notification

- CCPA — for California consumer data, including rights to access, delete, and opt out

- NYDFS 23 NYCRR 500 — cybersecurity program requirements for New York-licensed entities, including annual certification

The CFPB's 2024 rule extending federal oversight to large nonbank digital payment apps adds another layer for fintech consumer data handling.

Marketing Materials and External Communications

Consumer-facing content (ads, emails, website copy, social media) carries direct regulatory exposure. UDAAP applies to marketing representations, and the CFPB has signaled active scrutiny of how financial products are described to consumers.

For many financial services companies, marketing review is the highest-frequency compliance task — often requiring near-daily oversight rather than a periodic cycle.

Best Practices for Conducting an Effective Compliance Review

Establish a Structured Review Framework

Build a compliance checklist mapped to every applicable regulation for each jurisdiction the company operates in. Assign clear ownership for each domain — AML/BSA, KYC, consumer protection, data privacy, cybersecurity, marketing — and document who is responsible for what. Without ownership assignment, reviews generate findings with no one accountable for resolution.

Document Findings and Corrective Actions Rigorously

The paper trail matters as much as the review itself. A documentation process should capture:

- What was reviewed — specific policies, controls, or processes examined

- What issues were found — specific gaps, with supporting evidence

- What corrective action was taken — specific remediation steps, not generic intentions

- Timeline for resolution — target dates and actual completion dates

This record demonstrates a proactive compliance posture to regulators, auditors, and sponsor banks. A finding that was identified, documented, and resolved reflects well on the organization — far better than a finding discovered for the first time during an external examination.

Schedule Reviews Consistently and Involve the Right Stakeholders

Regulatory bodies set minimum cadences, but those are floors — not targets. Key benchmarks include:

- FINTRAC: Minimum two-year effectiveness review for Canadian reporting entities

- FCA: Annual Consumer Duty board reporting expected

- FFIEC: BSA/AML independent testing frequency tied to the firm's risk profile

For most regulated financial businesses, the working standard is a comprehensive annual review, with high-risk areas — AML controls, marketing materials, transaction monitoring — reviewed more frequently.

Cross-functional involvement is equally important. Legal, finance, operations, IT, and compliance leadership each see different risk surfaces. A review run solely within the compliance function misses operational and technical gaps that other teams are best positioned to catch.

That coordination burden is where many fintechs and early-stage money transmitters struggle — particularly those without a full-time CCO or BSA Officer. Fraxtional's fractional compliance leaders integrate directly into client teams across the US, UK, Canada, and EU, taking ownership of review scheduling, cross-functional coordination, and documentation. That's a different role than outside advisor — it's embedded compliance leadership without a permanent executive hire.

Frequently Asked Questions

What should be part of a compliance review?

A financial services compliance review should cover:

- AML/BSA controls and KYC/customer due diligence procedures

- Consumer protection obligations (UDAAP, Reg E, or Consumer Duty depending on jurisdiction)

- Data privacy requirements, cybersecurity standards, and marketing material accuracy

All findings should be documented with corrective actions tracked to resolution.

What is the difference between audit review and compliance review?

A compliance review is an internal, self-initiated assessment that identifies and fixes gaps before they attract regulator attention. A compliance audit is external (conducted by regulators or independent third parties) with formal assurance requirements and potential enforcement consequences. Both assess regulatory alignment, but from fundamentally different positions of authority.

What is the HMRC compliance review?

An HMRC compliance review is a check by HM Revenue & Customs verifying that a business meets its UK tax obligations. This is distinct from a financial regulatory compliance review conducted under FCA supervision — though UK-based fintechs may be subject to both, depending on their licensing and activity.

How often should a fintech company conduct a compliance review?

Annual reviews are the baseline minimum. High-risk areas like AML controls and transaction monitoring warrant quarterly attention — that cadence is now standard for most regulated fintechs. FINTRAC requires effectiveness reviews at least every two years for Canadian entities; the FCA expects annual Consumer Duty board reports.

Who is responsible for conducting a compliance review in a financial institution?

Compliance reviews are typically led by the Chief Compliance Officer (CCO) or BSA Officer, with input from legal, operations, and IT. Smaller fintechs without a full-time CCO often engage fractional compliance officers (like Fraxtional's fractional CCO and BSA Officer services) to own the review process without a permanent hire.