Introduction

Private equity firms today answer to more regulators than ever before. The SEC, DOJ, EU supervisory authorities, and cybersecurity watchdogs are all paying attention simultaneously. The consequences of falling short on any front are severe. Compliance has moved from a back-office function to a frontline responsibility that directly affects fund performance, LP relationships, and the firm's ability to operate in key markets.

The cost of getting it wrong is real. SEC enforcement actions can result in substantial fines, operational restrictions, and reputational damage that takes years to repair. The SEC Division of Examinations has reported that private fund advisers managing approximately $18 trillion in assets remain a consistent enforcement priority.

This guide covers:

- Core regulatory frameworks PE firms must navigate

- The five compliance areas that generate the most regulatory risk

- How to build a proactive compliance program

- What portfolio company obligations actually look like

- How to resource the compliance function without overspending

Key Takeaways

- Regulatory pressure on PE firms is growing across the US (SEC, DOJ, BSA), EU (AIFMD II, SFDR, CSRD), and UK (FCA, UK GDPR).

- Five areas demand consistent attention: AML/KYC, fees and valuations, conflicts of interest, cybersecurity, and ESG reporting.

- The SEC evaluates compliance programs on education, engagement, and execution — documented policies only matter if they're actually followed.

- PE firms carry direct liability for compliance failures at portfolio companies — pre-investment due diligence is not optional.

- Fractional compliance leadership offers director-level expertise without the cost of a full-time hire.

The Evolving Private Equity Compliance Landscape

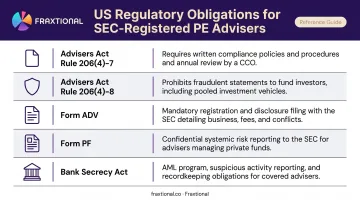

US Regulatory Requirements

SEC-registered PE advisers operate under a dense set of obligations. The foundational requirements include:

- Advisers Act Rule 206(4)-7 — requires written compliance policies and an annual review.

- Rule 206(4)-8 — prohibits misleading statements or omissions to fund investors.

- Form ADV — the public-facing disclosure document regulators use as a baseline during examinations.

- Form PF — required for advisers with at least $150 million in private fund AUM; large PE advisers with $2 billion or more file additional detail. Event reports (adviser-led secondaries, GP removal, fund termination) must be filed within 60 days after quarter-end.

- Bank Secrecy Act — FinCEN's 2024 rule extended BSA obligations to certain registered investment advisers, with an effective date of January 1, 2028.

That 2028 window is real, but firms that wait until 2027 to build controls will struggle. Start now.

The DOJ adds another dimension. Its M&A Safe Harbor Policy, announced in October 2023, incentivizes acquirers to voluntarily disclose misconduct discovered during acquisitions. For PE deal teams, that's a clear signal: compliance diligence now carries criminal law exposure, not just regulatory risk.

EU and UK Obligations

US obligations are only part of the picture. For PE firms marketing into or operating in Europe, a separate — and equally demanding — regulatory stack applies:

- AIFMD II (Directive 2024/927, adopted March 2024) — updated rules on authorization, delegation oversight, and loan-originating funds.

- SFDR — in effect since March 2021; Article 6, 8, and 9 fund classifications are product governance decisions, not marketing choices.

- CSRD — requires large and listed EU companies to publish sustainability reports. US sponsors must map which portfolio companies fall within scope before deals close.

- GDPR / UK GDPR — applies to any processing of EU or UK personal data, including LP contacts and deal-room information. Reportable breaches must be notified within 72 hours.

PE firms face a specific vulnerability here: inherited compliance failures from acquired companies. Regulators expect risk assessments during commercial due diligence, not as an afterthought post-signing.

5 Core Compliance Areas Every PE Firm Must Get Right

AML and KYC

FinCEN's 2024 rule formally brings certain registered investment advisers into the BSA framework. While the effective date is delayed until January 2028, PE firms that treat AML as optional in the meantime are taking a real risk.

A compliant AML program requires:

- Documented KYC procedures for limited partners and portfolio company counterparties

- Beneficial ownership verification and sanctions screening

- A designated BSA Officer responsible for ongoing monitoring

- Suspicious activity escalation procedures with documented SAR workflows

Fraxtional provides fractional BSA Officer support for PE clients, including named designation on regulatory filings and direct management of SAR/CTR workflows. Firms get defensible coverage without the cost or commitment of a permanent hire.

Fees, Expenses, and Valuations

This is where the SEC currently focuses most of its PE enforcement energy. The SEC charged TZP Management Associates in August 2025 with breaching fiduciary duty by overcharging management fees to private funds — a textbook example of what happens when fee-offset testing doesn't happen consistently.

Common risk areas include:

- Management fee offsets not applied after commitment periods end

- Transaction fees allocated inconsistently with LPA terms

- Non-pro rata expense allocations across fund vehicles

- Performance reporting that doesn't reconcile to source documents

Recalculate fees and offsets directly from governing documents — not from legacy spreadsheets or inherited models.

Conflicts of Interest and Employee Conduct

Cross-fund conflicts — where multiple funds invest in the same portfolio company — require explicit disclosure protocols and documented pre-transaction conflict reviews. The SEC has found that advisers sometimes obtained LPAC consent only after conflicted transactions had already occurred.

Other areas requiring active monitoring:

- Employee personal trading and pre-clearance policies

- Gifts and entertainment thresholds

- Political contribution restrictions (pay-to-play rules)

- MNPI controls and information barrier procedures

Cybersecurity and Data Privacy

SEC Regulation S-P amendments adopted in May 2024 require covered investment advisers to maintain incident response programs and notify affected individuals within 30 days of becoming aware of unauthorized access. That's a hard deadline — firms without a documented incident response plan are already non-compliant.

The financial exposure is significant. IBM's 2024 data puts the average breach cost in the financial sector above $6 million. PE firms hold sensitive LP information, deal data, and financial records across multiple systems — many of which are connected to portfolio companies with weaker controls.

Minimum requirements:

- Written incident response plan with tested escalation procedures

- GDPR/UK GDPR breach notification capability (72-hour window)

- Device controls and phishing awareness protocols for all staff

ESG and Sustainability Reporting

For PE firms with EU-domiciled funds or LP bases, SFDR classification carries direct compliance obligations. CSRD extends to large and listed EU portfolio companies — meaning sponsors need to identify which assets fall within scope before acquisition.

On the US side, the SEC adopted climate disclosure rules in March 2024, then voted to end its defense of those rules in March 2025. US requirements remain most relevant for IPO-ready or publicly listed portfolio companies. EU obligations are the more immediate operational driver for most PE firms.

Minimum operational requirements:

- SFDR Article 8/9 classification documented for EU-domiciled funds

- CSRD scope mapping completed at acquisition for large EU portfolio companies

- LP disclosure templates updated to reflect current sustainability commitments

- US climate reporting tracked for portfolio companies approaching public markets

Building a Proactive Compliance Program

Assess First, Build Second

Before redesigning any compliance program, review the current state across three levels:

- Adviser level — Form ADV accuracy, compliance manual, code of ethics, prior exam deficiency letters

- Portfolio framework — how compliance standards are set and monitored across investments

- Individual portfolio companies — where gaps exist relative to applicable requirements

Any gap identified at this stage becomes an immediate remediation priority. Fraxtional conducts independent compliance audits for PE firms, producing board-ready findings with prioritized remediation recommendations designed to hold up to regulatory and investor scrutiny.

Apply a Risk-Based Approach

Not all compliance obligations carry equal enforcement risk. The practical approach is to concentrate resources where the probability of regulatory action or investor harm is highest.

Build a risk register that:

- Identifies specific risk categories (AML, MNPI, cybersecurity, ESG, fees)

- Scores each by likelihood and severity

- Sets quarterly audit priorities based on the resulting rankings

This is the compliance equivalent of the 80/20 principle: most enforcement exposure concentrates in a small number of high-frequency, high-impact risk areas.

That concentration of risk is also what regulators scrutinize most closely — which is why what CCOs know, and how they act on it, matters as much as the policies themselves.

Education, Engagement, and Execution

SEC Enforcement Director Gurbir Grewal's October 2023 remarks at the NYC Bar Association Compliance Institute made the SEC's expectations explicit. Regulators now evaluate CCOs on whether they have:

- Educated themselves on current enforcement trends and the firm's actual business activities

- Engaged meaningfully with all business lines — not just legal and finance

- Executed on written policies, with documentation to prove it

Policies without evidence of execution carry no weight with examiners. Training must be ongoing, scenario-based, and documented — with records showing completion across the full employee population.

Schedule Regular Audits

Quarterly compliance audits targeting specific high-risk areas are more effective than a single annual review. The SEC expects firms to produce audit records during examinations. Firms that identify issues between exams — and document their remediation — consistently fare better when regulators arrive.

Managing Compliance Obligations Across Portfolio Companies

PE firms carry direct exposure for regulatory and reputational risks arising from portfolio company conduct. Fines or sanctions at an operating company affect fund returns and the firm's credibility with LPs — not just the company itself.

Pre-Investment Due Diligence

At minimum, compliance due diligence before closing should assess:

- AML/KYC framework maturity — does the company have documented controls, a designated BSA Officer, and SAR workflows?

- ESG reporting status — particularly for EU-based targets subject to CSRD

- Cybersecurity posture — covers incident response capability, data classification, and third-party vendor controls

- International trade and sanctions exposure — OFAC screening, export controls for relevant sectors

The DOJ's M&A Safe Harbor Policy offers a meaningful incentive here. Acquirers who identify misconduct during diligence, disclose it voluntarily, and remediate post-close can qualify for declination or reduced penalties. The policy's practical benchmark is a six-month post-closing disclosure window — making speed of diligence-to-remediation handoff operationally important.

Post-Acquisition Compliance Transformation

After closing, the goal is standardizing minimum compliance requirements across portfolio companies without over-resourcing each individual entity. Fraxtional's post-acquisition program buildouts for PE firms typically cover:

- Compliance gap analyses against regulatory and investor benchmarks

- AML/KYC framework implementation with documented controls

- Board-ready documentation and LP reporting packages

The result is oversight-level visibility for the PE firm — without staffing a full compliance function at every portfolio company.

The Resourcing Question: Building Your PE Compliance Function

The Cost Reality

Maintaining a full compliance function — dedicated CCO, compliance team, regulatory filing support, outside counsel for complex matters, and a technology stack — represents a significant ongoing investment. For PE firms managing multiple funds, cross-border LP bases, and a portfolio of operating companies, that cost compounds quickly.

Key cost drivers include:

- Personnel (CCO, compliance analyst, legal support)

- Form ADV and Form PF filing management

- Cybersecurity and incident response infrastructure

- EU/UK regulatory reporting and outside counsel

- Portfolio company risk assessment and monitoring

The Fractional Alternative

Those cost pressures have pushed many PE firms toward fractional compliance leadership — director-level expertise without the overhead of a permanent hire.

Fraxtional provides CCO, BSA Officer, MLRO, CAMLO, and CRO functions on a fractional basis, with named title use, direct Director-level access, and engagement flexibility scaled to the firm's needs.

The three engagement models map to different PE situations:

| Model | Structure | Best for |

|---|---|---|

| On Demand Advisory | Flat one-time fee | Discrete projects: risk assessments, pre-deal diligence, policy buildouts |

| Subscription Advisory | Monthly/weekly retainer | Active deal periods, portfolio monitoring, staff augmentation |

| Fractional Advisory | Monthly retainer with named title | Ongoing CCO, BSA Officer, MLRO, or CAMLO designation |

For PE firms operating across the US, Canada, UK, and EU, Fraxtional's cross-border regulatory coverage — spanning BSA/AML, UDAAP, UK FCA requirements, FINTRAC, and international AML mandates — makes it possible to manage multi-jurisdictional obligations under a single engagement structure.

Technology Stack Considerations

Compliance technology won't replace judgment, but it can automate routine tasks. PE firms should evaluate tools for:

- Employee trade monitoring and pre-clearance

- Communications archiving

- Code of ethics enforcement and attestation tracking

- Risk assessment documentation and audit trails

- Entity management across fund structures

With the administrative burden handled by purpose-built tools, the compliance function can focus on the higher-risk, judgment-intensive work that actually protects the firm.

Frequently Asked Questions

What is the 80/20 rule in private equity compliance?

The 80/20 rule means concentrating roughly 80% of compliance resources on the 20% of activities that carry the highest regulatory risk. For PE firms, that means prioritizing fee and expense testing, conflict disclosures, MNPI controls, and AML — where SEC enforcement and fiduciary duty exposure are most concentrated.

What regulations must private equity firms comply with?

In the US: the Investment Advisers Act (Rules 206(4)-7 and 206(4)-8), Bank Secrecy Act, and SEC reporting requirements including Form ADV and Form PF. In the EU and UK: AIFMD II, SFDR, CSRD, MiFID II, and GDPR. DOJ M&A enforcement standards apply to acquisition activity.

How often should private equity firms conduct compliance audits?

Best practice is quarterly audits targeting high-risk areas — fees, conflicts, MNPI controls, cybersecurity — plus a comprehensive annual review. The SEC expects firms to produce audit records during examinations, and a quarterly cadence lets you remediate issues before they escalate.

What is the difference between a fractional CCO and a full-time CCO?

A fractional CCO provides director-level compliance oversight on a flexible engagement model, with full named title use on regulatory filings and investor documentation. Firms get experienced leadership at a lower cost than a full-time hire — especially useful for PE firms managing obligations across multiple jurisdictions or portfolio companies.

What are the consequences of compliance failures for PE firms?

Consequences include SEC fines, civil litigation from investors, operational restrictions, and reputational damage with LPs. Inherited compliance failures from portfolio companies — particularly in AML, cybersecurity, or financial crime — can also trigger direct adviser-level liability and affect fund returns.

What compliance obligations apply to PE portfolio companies?

PE firms must ensure portfolio companies meet applicable AML/KYC, ESG, data privacy, and financial crime standards. Assess these obligations during pre-investment due diligence and build them into a post-acquisition compliance program. EU-based portfolio companies may also carry independent CSRD and GDPR obligations that flow back to the sponsor.