Regulatory risk assessment is the tool that prevents those outcomes — yet it is consistently referenced without being explained at the operational level compliance teams and founders actually need. This article changes that.

Key Takeaways

- Regulatory risk assessment identifies, scores, and manages the risks posed by existing and changing regulations before they cause financial penalties or business disruption.

- The process has three layers: inherent risk, risk controls, and residual risk — what's left after controls are applied.

- A practical assessment follows five steps — from identifying applicable regulations to continuous monitoring — covered in full below.

- Key risk drivers in fintech include product velocity, third-party relationships, jurisdictional complexity, and compliance staffing gaps.

- The most common failure: treating the assessment as a one-time document instead of an ongoing management process.

What Is Regulatory Risk Assessment — and Why It Matters

Regulatory risk assessment is a systematic process for identifying the likelihood and impact of regulatory non-compliance or regulatory change across a company's products, services, and operations — and then evaluating the controls in place to manage those risks.

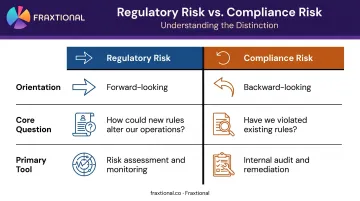

The distinction from compliance risk matters, because the two require different responses:

| Regulatory Risk | Compliance Risk | |

|---|---|---|

| Orientation | Forward-looking | Backward-looking |

| Core question | How could new or changing rules alter our operations? | Have we violated rules that already exist? |

| Primary tool | Risk assessment and monitoring | Internal audit and remediation |

Both matter. But conflating them creates gaps — companies focused only on past violations miss emerging exposures until a regulator finds them first.

For financial services companies, the stakes are higher than in most industries. Fintechs, crypto firms, BaaS providers, and embedded finance platforms operate across multiple agencies simultaneously — FinCEN, CFPB, OCC, FRB, FTC in the US; FCA in the UK; FINTRAC and OSFI in Canada; EBA and national competent authorities under MiCA in the EU.

A single product feature that creates no issue under BSA/AML may still implicate UDAAP, Reg E, state money transmission laws, and GDPR depending on where the customer is located. Mapping that multi-jurisdictional exposure — before it surfaces in an exam or enforcement action — is exactly what regulatory risk assessment is designed to do.

How Regulatory Risk Assessment Works: Inherent Risk, Controls, and Residual Risk

All sound regulatory risk assessments rest on a three-layer model. FINTRAC's risk assessment guidance explicitly defines this structure, and the FFIEC BSA/AML Examination Manual operationalizes it across US examination practice.

Inherent Risk

Inherent risk is the raw level of regulatory exposure before any controls are applied. Examiners and regulators assess it across three dimensions:

- Institutional factors — organizational complexity, product type, delivery channels, vendor relationships, and prior examination findings

- Environmental factors — market demographics, competitive landscape, and geographic diversity of the customer base

- Legal and regulatory factors — density of applicable rules, recent regulatory changes, and current enforcement trends

Products with high transaction volume, cross-border exposure, or novel business models carry higher inherent risk ratings. A crypto exchange serving customers in five jurisdictions will score materially higher than a single-state, single-product payment processor — and the assessment should reflect that difference explicitly.

Risk Controls

Controls are evaluated against four pillars:

- Board and senior management oversight — do directors understand the institution's risk profile, and do senior leaders have the expertise to manage it?

- Policies, procedures, and staff training — is guidance documented, current, and actively applied?

- Risk monitoring and management information systems — does compliance data reach decision-makers in a timely way?

- Internal controls and audit — does independent testing verify that preventative controls are actually working?

Weak controls in any one pillar can unravel an otherwise well-designed program. The FCA's 2024 enforcement action against CB Payments Limited illustrates the point: the regulator fined the firm £3,503,546 after finding failures in the design, testing, implementation, and monitoring of controls across multiple products, including Coinbase Pro and Simple Trade Service. Approximately 31% of affected high-risk customers made prohibited deposits later used for cryptoasset transactions totaling approximately $226 million.

Residual Risk

Residual risk is the outcome of balancing inherent risk ratings against control effectiveness for each material product, service, or business line. A high inherent risk rating combined with strong controls might produce a medium residual risk score — acceptable with continued monitoring. The same high inherent risk with weak controls produces a high residual risk score that demands immediate remediation.

Residual risk scores determine where management attention and resources go. Those scores should drive the compliance calendar — high residual risk areas get more frequent testing, closer board reporting, and faster escalation paths when red flags appear.

Step-by-Step: How to Conduct a Regulatory Risk Assessment

One prerequisite before the steps: the assessment must be documented in a risk register or assessment matrix, reviewed and approved at the board or senior management level, and updated whenever material changes occur — not just at year-end.

Step 1: Identify Applicable Regulations and Regulators

Map every product, service, geography, and third-party relationship against the regulatory bodies and specific rules that govern them.

For companies operating across the US, UK, EU, and Canada, this includes:

- US: BSA/AML, UDAAP, Reg E, Reg Z, state money transmission laws, GLBA/Safeguards, FinCEN MSB registration

- UK: FCA registration, Consumer Duty, AML/CTF requirements for cryptoasset businesses

- EU: MiCA, GDPR, DORA, national competent authority requirements

- Canada: PCMLTFA, FINTRAC registration, OSFI B-10 for third-party risk

The output is a live regulatory register organized by business line. It should never be a static spreadsheet filed in a shared drive.

Step 2: Score Likelihood and Impact

For each identified exposure, assign two ratings:

- Likelihood — how probable is non-compliance or a regulatory change that materially affects this area?

- Impact — what are the financial, operational, and reputational consequences if it materializes?

A 1–5 scale for each dimension produces a risk heat map that makes prioritization transparent and defensible to examiners, investors, and board members.

Step 3: Select Mitigation Strategies and Assign Owners

For each high or medium-rated risk, choose a response:

- Avoid — exit the product, feature, or market

- Mitigate — add controls, procedures, or monitoring

- Transfer — through insurance or contractual terms with vendors

- Accept — with documented rationale and a monitoring plan

Assign an owner and a remediation deadline. For early-stage fintechs and crypto firms, mitigation often means building compliance infrastructure from scratch. That is a fundamentally different kind of project than strengthening controls that already exist.

Step 4: Implement Controls and Document Evidence

Convert mitigation decisions into three types of controls:

- Preventive controls — policies, training, product design guardrails

- Detective controls — transaction monitoring, audit triggers, complaint tracking

- Corrective controls — escalation procedures, incident response plans

Store policies, training logs, monitoring reports, and regulator correspondence in a central evidence repository. When an examiner or investor conducts due diligence, the documentation either exists or it does not. Controls without evidence will not hold up — treat documentation as part of the control itself.

Step 5: Monitor, Update, and Escalate

Embed ongoing monitoring into the compliance management program with a tiered cadence:

- High-risk areas: reviewed monthly

- Medium-risk areas: reviewed quarterly

- Low-risk areas: reviewed semi-annually

FINTRAC requires a documented periodic review of the risk-based approach at least every two years, with a formal effectiveness review on the same cadence. The FFIEC expects BSA/AML risk assessments to reflect actual changes in products, services, customers, and geographies as they occur.

Scheduled reviews set the baseline. Certain events, however, require an immediate reassessment regardless of cycle:

- New product launches or market expansions

- Regulatory guidance updates or new enforcement actions in the sector

- Changes in sponsor bank requirements

- Key personnel departures from the compliance function

- Material changes to the business model or customer base

Key Factors That Shape Regulatory Risk in Fintech and Financial Services

Product Velocity and Third-Party Relationships

Fintechs and crypto firms launch products faster than compliance infrastructure typically scales. Each new product introduces regulatory touchpoints that must be assessed before go-live , not after launch. A new payment product may simultaneously implicate Reg E, UDAAP, state money transmission laws, and BSA/AML. Missing any one of those creates exposure.

Third-party and sponsor bank relationships add another layer of exposure. The OCC's interagency third-party guidance is direct: engaging a third party does not diminish a bank's responsibility to operate safely and comply with applicable law. The Federal Reserve's 2024 enforcement actions against Evolve Bank & Trust and Green Dot both required review and remediation of fintech partner programs , confirming that vendor-level compliance failures flow directly back to the primary institution.

The risk assessment must extend to every material vendor and sponsor bank relationship, with documented due diligence, contractual standards, and ongoing monitoring for each one.

Jurisdictional Complexity

Cross-border operations multiply regulatory exposure in ways that regulators often catch before the company does. Binance's enforcement history illustrates the point: the DOJ found that Binance processed over $898 million in trades between US users and users in Iran between January 2018 and May 2022 without adequate controls, while FINTRAC separately imposed a $6,002,000 penalty on Binance Holdings Limited in May 2024 for PCMLTFA violations as a foreign MSB , including failure to register and failure to report certain virtual-currency transactions.

Cross-border assessments must account for:

- Overlapping and potentially conflicting privacy requirements (GDPR vs. US state privacy laws)

- Different licensing standards across jurisdictions (FCA registration vs. OCC national bank charter vs. FINTRAC MSB registration)

- FATF Travel Rule obligations, which 99 jurisdictions have now passed or are actively legislating, with uneven implementation across markets

Compliance Staffing and the Fractional Model

Managing multi-jurisdictional exposure requires more than policy documents — it requires staffing depth proportional to the risk. The depth of the compliance function directly affects the quality of both the assessment and the controls it surfaces. Growing fintechs and crypto firms often find that their regulatory exposure outpaces their internal team's capacity, typically discovered at the worst possible time: a bank partnership review or investor due diligence.

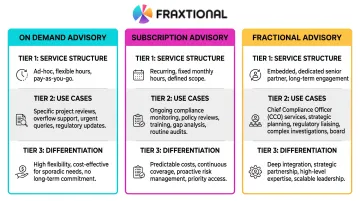

This is where fractional compliance leadership provides a practical path. Fraxtional provides director-level CCO, CRO, and BSA Officer expertise through three engagement models:

| Model | Structure | Best For |

|---|---|---|

| On Demand Advisory | Flat one-time fee | Discrete risk assessments, audits, procedure development |

| Subscription Advisory | Weekly or monthly retainer | Ongoing support and staff augmentation |

| Fractional Advisory | Monthly retainer with named title use | Companies needing a dedicated CCO, CRO, or BSA Officer |

Under the Fractional Advisory model, directors take direct ownership of the risk assessment process: embedding with internal teams, conducting full risk mapping across operations, identifying exposure areas tied to vendors, engineering, and operations, and producing documentation ready for board reviews and bank evaluations.

The cost difference is significant. A fractional CRO through this model runs 50–70% less than a full-time equivalent, whose fully loaded cost typically exceeds $25,000 per month.

Common Issues and Misconceptions

Three patterns show up repeatedly across FinTech and crypto assessments — and each one undermines the credibility of an otherwise solid program.

Treating the assessment as a one-time document. Many teams complete a regulatory risk assessment in response to an exam or investor request, then file it away. The result is a static snapshot that becomes inaccurate within months as products evolve and regulations shift. A credible assessment is a continuous management process, not an annual deliverable.

Conflating low residual risk with no risk. A low residual risk score means strong controls are in place — not that the underlying regulatory exposure has disappeared. Teams that interpret a favorable rating as permission to deprioritize monitoring are caught off guard when controls erode or requirements shift. Schedule periodic re-evaluations; residual scores reflect today's controls, not tomorrow's reality.

Scoping the assessment too narrowly. FinTech and crypto companies frequently assess risk only for their primary product or primary jurisdiction. Regulators assess the institution as a whole. The risk assessment must match that scope, covering:

- All material business lines and delivery channels

- Third-party and vendor arrangements

- Embedded activities and secondary markets

Frequently Asked Questions

What is the regulatory risk assessment process?

It is a structured process of identifying applicable regulations, scoring the likelihood and impact of non-compliance or regulatory change, evaluating existing controls, and calculating residual risk. The goal is to inform management decisions and prioritize compliance resources based on actual exposure — not assumptions.

What is an example of regulatory risk?

A crypto firm that expands into a new jurisdiction without assessing local AML licensing requirements faces simultaneous registration, reporting, and sanctions exposure. FINTRAC's $6 million penalty against Binance as a foreign MSB in Canada illustrates this: failure to register and failure to report virtual-currency transactions in a jurisdiction where the firm was operating.

What is the difference between regulatory risk and compliance risk?

Regulatory risk is forward-looking — it asks how new or changing regulations could affect the business. Compliance risk focuses on whether the company has already violated rules that exist today. They require different responses: regulatory risk calls for monitoring and horizon scanning; compliance risk calls for audit and remediation.

How often should a regulatory risk assessment be updated?

At minimum, annually — FINTRAC formally requires a documented review every two years. Certain events should trigger an immediate reassessment: new product launches, regulatory guidance updates, enforcement actions in the sector, material business model changes, or loss of key compliance personnel.

Who is responsible for regulatory risk assessment in a fintech or financial services company?

Responsibility is shared: the board approves and oversees the program, the CCO or CRO leads it, business line managers implement controls, and internal audit validates effectiveness. Early-stage companies without a full-time CCO often fulfill this function through a fractional compliance officer — such as Fraxtional's Fractional Advisory model, which provides a named CCO or CRO title without a full-time hire.

What are the three main components of a regulatory risk assessment?

The three-layer model covers: inherent risk — raw regulatory exposure before any controls are applied; risk controls — the policies, oversight structures, monitoring systems, and audit mechanisms in place; and residual risk, which is what remains after controls are accounted for and directly drives prioritization decisions.