Introduction

In January 2017, Western Union agreed to forfeit $586 million after admitting to criminal violations including willfully failing to maintain an effective anti-money laundering program. The penalty wasn't an isolated case—in 2023, Binance admitted it "willfully operated as an unregistered MSB" and paid a historic $3.4 billion to FinCEN. These enforcement actions underscore a fundamental reality: Money Service Businesses (MSBs) sit at a vulnerable intersection of high transaction volume, cross-border reach, and limited traditional banking oversight.

MSBs provide essential financial services to underserved and unbanked populations worldwide. Yet the same features that make them valuable to legitimate customers—speed, accessibility, and sometimes anonymity—make them attractive channels for money launderers moving illicit funds across borders.

This guide is for compliance officers, founders, and executives at fintech companies, money transmitters, crypto platforms, and embedded finance companies navigating MSB-related AML obligations. We'll cover what makes MSBs high-risk, how criminals exploit them, and what compliance obligations you must meet to avoid becoming the next enforcement headline.

TLDR:

- MSBs face heightened money laundering risk due to cash intensity, speed, and cross-border reach

- Enforcement penalties reach billions—Binance paid $3.4B; Western Union forfeited $586M

- Registration with FinCEN is mandatory; unregistered operation is a federal crime

- Every MSB must maintain a written AML program with four pillars: policies, officer, training, and audit

- Fractional BSA officers provide executive-level accountability without full-time hiring costs

What Is a Money Service Business?

A Money Service Business (MSB) is any non-bank financial entity engaged in transmitting, converting, or exchanging money. Under the Bank Secrecy Act (BSA), MSBs are classified as financial institutions and held to the same AML/KYC standards as traditional banks.

FinCEN's threshold is specific: a business conducting more than $1,000 in MSB activity with the same person on any given day qualifies — and money transmitters are subject to registration at any transaction amount.

That "any amount" threshold for money transmitters is a trap for startups—there's no minimum transaction size that exempts you from registration.

Subtypes of MSBs

FinCEN's MSB definition includes these primary categories:

- Currency dealers and exchangers (>$1,000/day threshold) including fiat-to-crypto exchanges

- Money transmitters (any amount)

- Check cashers (>$1,000/day)

- Traveler's check and money order issuers, sellers, and redeemers (>$1,000/day)

- Prepaid card and stored value providers (funds exceeding $10,000/day)

- U.S. Postal Service money services

Modern MSBs now include P2P platforms, digital wallets, remittance services, and crypto asset exchanges — all subject to the same core BSA obligations.

Not every financial entity falls under this framework. Excluded from MSB classification:

- Traditional banks and foreign banks (regulated separately under banking laws)

- Entities regulated by the CFTC or SEC

- Agents of a registered MSB who file under the principal MSB

- Natural persons engaging in MSB activities on an infrequent basis for no profit

- Government agencies

Understanding where your business falls determines your registration obligations — and, as the next sections cover, your exposure to money laundering risk.

Why MSBs Are Considered High Risk for Money Laundering

MSBs are structurally attractive to money launderers because of the combination of cash-intensive operations, high transaction velocity, and cross-border reach—all of which make individual transactions difficult to trace. FATF's updated guidance formally designates MSBs—specifically Money or Value Transfer Services—as high-risk, and makes clear that wholesale de-risking conflicts with risk-based AML standards.

Key vulnerability factors:

- Weak or absent identity verification on some services makes source-of-funds tracing nearly impossible

- Physical currency cannot be reliably traced once converted or transmitted

- Agent networks and third-party intermediaries fragment the transaction chain, creating accountability gaps

- In crypto and mobile money environments, transfer speed routinely outpaces transaction monitoring

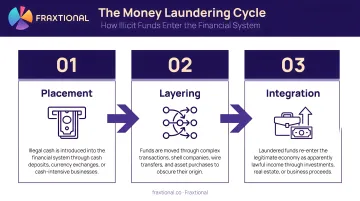

MSBs map perfectly to all three stages of the money laundering cycle:

- Placement — Depositing illicit cash via check cashing or currency exchange

- Layering — Sending funds cross-border through wire or remittance services to obscure origin

- Integration — Using converted funds or foreign currency notes to re-enter the legitimate economy

Those three stages play out differently depending on the MSB type involved—and some subtypes carry concentrated exposure.

Structural Risks in MSB Subtypes

2024 World Bank data show that grey-listed countries absorbed significant remittance volumes—Nepal received $11.3 billion, Kenya $5.0 billion, and DRC $2.0 billion. These flows create natural corridors for both legitimate transfers and illicit fund movement.

Beyond remittance corridors, two other MSB subtypes present distinct monitoring challenges:

- Cryptocurrency exchanges that obscure beneficial ownership or allow rapid asset conversion add layers of complexity that standard transaction monitoring systems struggle to track

- Prepaid card issuers with stored value that can be transferred or withdrawn below reporting thresholds provide a portable, pseudo-anonymous vehicle for moving funds

The De-Risking Problem

The U.S. Treasury's 2023 De-Risking Strategy documented that approximately 28% of money transmitter principals and 45% of MTO agents surveyed had lost access to banking services. As banks exit MSB relationships to avoid regulatory exposure, some MSBs are pushed to informal or less-regulated channels—ironically increasing systemic money laundering risk rather than reducing it.

Common MSB Money Laundering Typologies and Red Flags

MSB money laundering takes predictable forms. Recognizing these typologies — and the specific red flags tied to each — is the foundation of any effective AML program.

Structuring (Smurfing)

One of the most prevalent schemes: criminals break large cash transactions into multiple smaller ones to stay below reporting thresholds. Examples include purchasing multiple money orders just under $3,000, or wiring funds just under $10,000 across multiple days or locations. MSBs should treat repeated sub-threshold transactions from the same customer or coordinated groups as a primary red flag.

Customer Identity Red Flags

FinCEN guidance identifies these warning signs:

- Presenting false, altered, or inconsistent identification

- Changing names or addresses across transactions

- Reluctance to provide required documentation or verify information

- Abruptly abandoning a transaction when reporting is mentioned

- Inability to produce appropriate documentation (invoices, business records) to support a requested transaction

Transaction Pattern Red Flags

Monitor for activity inconsistent with the customer's stated occupation or business:

- Retail customer sending high-volume cross-border transfers

- Sudden spikes in transaction size or frequency without explanation

- Receiving multiple incoming transfers and immediately consolidating them for outbound wires

- Exchanging small bills for large denominations without clear business rationale

- Negotiable instruments in round denominations under $3,000 used to fund domestic accounts — a structuring variant that bypasses CTR triggers

Agent and Employee Risk

MSBs with agent networks face an additional layer of exposure: agents who are complicit in laundering, whether by accepting bribes to suppress CTR filings or by coordinating transactions across branch locations to stay below thresholds. Internal red flags include:

- Employees with unexplained lifestyle changes

- Reluctance to take leave or allow oversight of their transactions

- Pattern of transactions just below reporting thresholds at specific locations

- Agent locations with unusually high cash activity relative to customer base

Cross-Border Corridor Risk

Frequent transfers to jurisdictions listed on FATF's non-cooperative or high-risk country lists, or to countries where the customer has no apparent business or personal ties, should prompt additional due diligence and potential SAR filing. FATF's October 2025 update includes Kenya, Nepal, DRC, and other countries that also appear as top remittance recipients. That overlap means MSBs can't treat high-volume corridors as automatically low-risk.

AML Compliance Requirements Every MSB Must Meet

Registration: The Baseline Obligation

In the US, MSBs must register with FinCEN via Form 107 within 180 days of establishment and renew every two years. Operating as an unregistered MSB is a federal crime under 18 U.S.C. 1960, carrying fines and up to 5 years imprisonment. MSBs must also maintain an agent list updated annually and retain all supporting documentation for five years.

Civil penalties for non-registration reach $5,000 per day per violation, with each day counting as a separate violation.

Written AML Program: The Four Pillars

Under 31 CFR 1022.210, every MSB must have a documented AML compliance program that includes:

- Internal policies, procedures, and controls — specific to the MSB's products, channels, and customer risk profile

- A designated compliance officer accountable for day-to-day program execution and regulatory responsiveness

- Ongoing employee training covering red flags, reporting duties, and role-specific obligations

- Independent audit/review to test whether controls actually work — not just that they exist on paper

The program must be risk-commensurate—a high-volume urban money transmitter faces different obligations than a small rural check casher. Regulators look for programs calibrated to actual risk, not generic templates applied across the board.

KYC and Customer Due Diligence (CDD)

MSBs must verify customer identity across four core data points:

- Full legal name

- Physical address

- Date of birth

- Tax ID or SSN

CDD requires assessing money laundering risk, establishing expected transaction patterns, and flagging deviations. For higher-risk customers—such as those in high-risk jurisdictions or with complex ownership structures—Enhanced Due Diligence (EDD) applies. CDD applies to every transaction regardless of size.

SAR and CTR Reporting Obligations

MSBs must file a Suspicious Activity Report within 30 days of detecting a suspicious transaction of $2,000 or more (60 days if no suspect is identified). SAR confidentiality is legally required—tipping off a subject is a criminal offense.

Currency Transaction Reports are required for cash-in or cash-out transactions exceeding $10,000 in a single day, including aggregated transactions.

Additional thresholds:

- $3,000 Monetary Instrument Log — required for cash purchases of bank checks, money orders, and traveler's checks between $3,000 and $10,000

- $3,000 Funds Transfer Recordkeeping — MSBs must maintain records for transmittals of funds of $3,000 or more

Fractional Compliance Leadership for Early-Stage MSBs

Meeting these obligations requires more than written policies — it requires accountable leadership who understands how regulators think. For fintech companies and money transmitters building programs from the ground up, that expertise is often the hardest thing to source.

Many early-stage MSBs are addressing this through fractional compliance models. Fraxtional's BSA Officer and CCO services give growing companies access to director-level AML expertise without the cost and commitment of a full-time hire. These fractional leaders can be officially named in regulatory filings and provide the executive accountability that regulators and sponsor banks expect.

How MSBs Are Regulated Around the World

FinCEN's guidance on convertible virtual currency and FATF's Travel Rule for virtual assets now require digital-asset MSBs to collect and transmit originator and beneficiary data on transfers above applicable thresholds.

In August 2025, FinCEN issued Notice FIN-2025-NTC1 highlighting the use of Convertible Virtual Currency (CVC) kiosks for scam payments and illicit activity—requiring financial institutions to flag related SARs with the key term "FIN-2025-CVCKIOSK."

Consequences of MSB AML Non-Compliance

Regulatory Penalties

Enforcement actions span a wide spectrum:

- Civil monetary penalties — up to $5,000 per day for registration failures

- Criminal prosecution — individuals (including compliance officers) face fines up to $500,000 and 10 years imprisonment

- Mandatory remediation plans — often including multi-year monitorships

- License revocation — ending your ability to operate

Recent enforcement demonstrates these aren't theoretical. Paxful paid FinCEN $3.5M in December 2025 for unregistered MSB operation, AML failures, and SAR violations. Binance's 2023 settlement included a five-year monitorship and required complete exit from the United States.

Reputational and Operational Consequences

The financial hit is only part of the picture. Non-compliant MSBs also face:

- Loss of banking relationships — the "de-risking" phenomenon where banks terminate MSB accounts to avoid regulatory exposure

- Investor confidence erosion — AML scrutiny of major payment platforms has triggered share price drops

- Customer attrition — fraud concerns and service interruptions drive customers to competitors

- Executive personal liability — if your MSB becomes a vehicle for money laundering, executives face personal criminal exposure

Western Union's 2017 settlement shows how far operational remediation can reach. Required measures included:

- Agent training and ongoing monitoring for fraud-induced transfers

- Enhanced due diligence on all new and renewing agents

- Suspension or termination of noncompliant agents

- A comprehensive anti-fraud program maintained for years post-settlement

Frequently Asked Questions

Is a money service business considered high risk for AML?

Yes. MSBs are formally designated as high-risk by FATF and most national regulators due to their cash-intensive, high-volume, and often cross-border nature, making them attractive for placement, layering, and integration of illicit funds.

Do mobile financial services have a high risk of money laundering?

Mobile financial services—including digital wallets, mobile money transfer apps, and P2P platforms—carry elevated AML risk because they enable fast, sometimes pseudonymous transactions at scale. They are classified as MSBs and subject to the same AML obligations as traditional money transmitters.

Which types of businesses are at the highest risk for money laundering?

Among MSBs, money transmitters, currency exchanges, remittance providers, and crypto asset platforms carry the highest inherent ML risk due to cross-border reach, transaction anonymity, and high volumes. Cash-intensive businesses such as check cashers follow closely.

What does an MSB AML compliance program need to include?

In the US, FinCEN requires four core pillars: written internal policies and controls, a designated compliance officer, ongoing employee training, and an independent audit function. Each element must be tailored to the MSB's specific risk profile, size, and transaction volumes. UK and EU firms face equivalent obligations under their respective frameworks.

What are the penalties for MSB non-compliance with AML regulations?

Penalties range from civil fines ($5,000 per day for registration failures in the US) to criminal prosecution carrying up to $500,000 in fines and 10 years imprisonment. Non-compliant MSBs also risk license revocation and loss of banking access through de-risking.